Affordable housing continues to be a strong and stable commercial real estate asset. National-level consistency in both rent-growth and vacancy rates has been a hallmark of this sector for many years, including during the COVID-19 pandemic.

In no way, however, is the sector excluded from more granular-level variations or nuances. Regional- and metropolitan-level performance metrics (and corresponding development patterns) differ in important ways, and a careful study of the data exposes both risk and opportunity for commercial real estate stakeholders.

With a 2.4% vacancy rate at the end of third- quarter 2021, the market for affordable housing — defined here as properties served by the federal Low Income Housing Tax Credit (LIHTC) program — has fully recovered from the minimal stress it endured during the peak of the pandemic-induced economic downturn. This likely comes as little surprise given the relative stability in this market over the past few years.

In fact, since 2015, when Moody’s Analytics Reis began tracking the LIHTC market at the national level, the vacancy rate has remained within a tight 2% to 2.6% boundary. During this same time period, vacancy rates for all other U.S. multifamily properties ranged between 4.1% to 5.4%.

Further, many of the vacancies in affordable housing are due to frictional reasons rather than a lack of demand. In fact, waiting lists are prevalent in this sector and it’s typical for space to be preleased by the time one of the approximately 35,000 new units per year are completed.

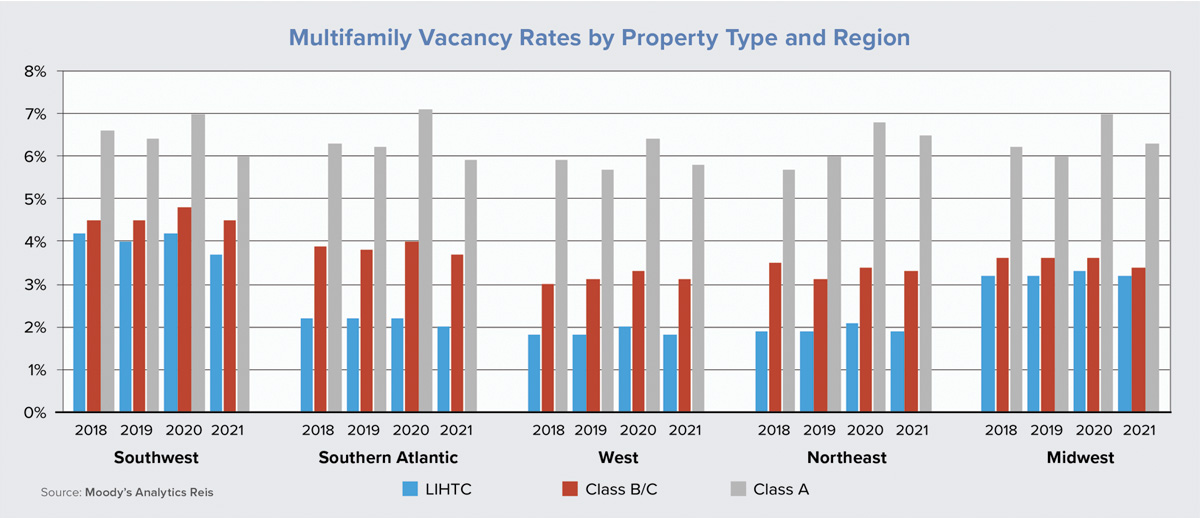

Looking at the chart on this page, the range of affordable-housing vacancy rates from 2018 through 2021 is minimal for each region and is similar to national averages. Instead, variation in vacancies across regions — as well as these levels’ relationships to their market-rate housing metrics — are most interesting.

The data shows that these differences tend to not be related to demand pressures, while the smaller gaps between LIHTC and market-rate properties tend to be in places where new supply has been most abundant and/or where market-rate housing costs tend to be lowest. For example, the Southwest region (which consists of Texas, Oklahoma, Arkansas and Louisiana) has had significant growth in LIHTC housing over the past few years while costs of living, especially for Class B/C properties, tend to be lower here than for its regional counterparts.

Delving into more granular levels of data exposes even further nuance and intrigue. Six of the nation’s 10 lowest LIHTC vacancy rates at the metro level are found in the state of Florida. Across the state’s 12 tracked metros, the average rate is a paltry 1.3% while the major markets of Orlando, Miami and Fort Lauderdale each have sub-1% rates.

Adding to this is a combination of annual asking-rent growth that averages about 3.5% statewide, fairly low construction activity and increasing rates of lower-income residents. Consequently, the case for further research and potential investment becomes quite interesting.

Given the recent and significant surges in the cost of living — including spikes in market-level rents — regulatory pressures for increasing the level of affordable-housing options are stronger than ever. At the national level, the Build Back Better Act proposed by President Joe Biden has set a priority to enable the construction, rehabilitation and improvement of more than 1 million affordable homes.

At a more local level, the Los Angeles City Council recently voted to explore a variety of ways to increase the city’s supply of affordable housing, as well as to find ways to place new developments in higher-amenity areas. These and a variety of upcoming measures have the capacity to alleviate housing-supply concerns at the low end of the pricing spectrum. Done incorrectly, they also have the potential to crowd out current programs and private investments. ●