All good things must come to an end — at least temporarily. That includes the recent major expansion of the industrial sector.

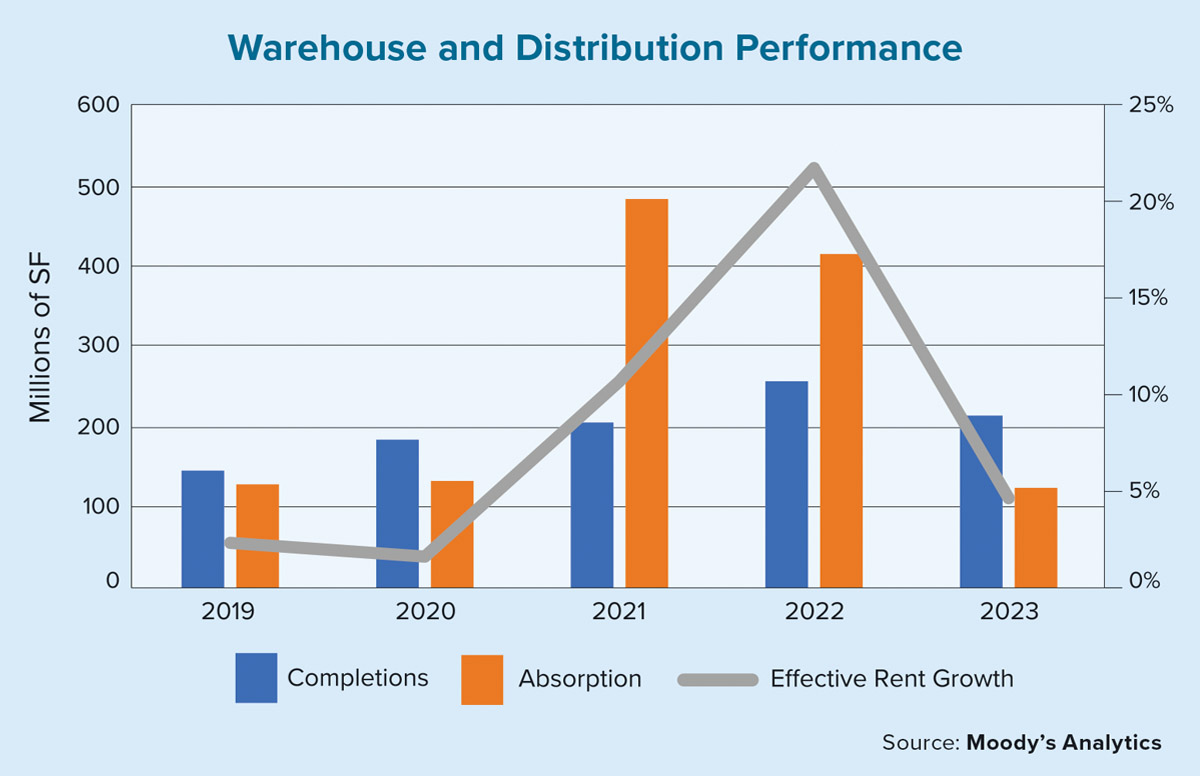

One of the darlings of commercial real estate in recent years, industrial is facing a bumpy path forward in the near term. Vast amounts of speculative construction fed by early pandemic tailwinds are currently meeting more muted demand than expected. Through 2023, the pace of industrial rent growth was more than halved, beginning the year with a solid average of 1.5% through the first two quarters, before dropping to a historically weak 0.6% to close out the year.

The absorption rate, or the change in occupied stock, and demand for space did remain positive throughout the year. The pace of leasing activity, however, slowed considerably in the fourth quarter, causing the full-year quarterly average to be a relatively weak 30 million square feet.

Considering that new construction added more than 50 million square feet of space each quarter, the fact that the market produced rent gains at all is a testament to the importance of a market’s current occupancy rate in relation to its long-term, and “natural” rate.

Even with the current supply and demand balance accounted for, the national vacancy rate sits at a tight 5.4%, with some markets substantially lower. This is in stark contrast to the 10% average national vacancy rate for industrial during the previous decade.

Of 47 metros being tracked by Moody’s Analytics, 22 experienced positive net absorption, with four metros having net absorption in excess of 1 million square feet. Dallas led the way on the demand side of the equation in the fourth quarter, with a net absorption of 3.4 million square feet. It was followed by Houston and San Bernardino/Riverside with a net absorption of 2.5 million and 1.7 million square feet, respectively.

At the other end, Los Angeles experienced the greatest drop in demand, shedding 1.6 million square feet of occupied space in the fourth quarter. Los Angeles was the only metro area whose negative net absorption exceeded 1 million square feet. Central New Jersey was next up, posting a decline of 734,000 square feet.

Fluctuating supply and demand metrics at the metro level led to a wide distribution of occupancy and rent changes, so while nearly every metro experienced positive effective rent growth, it is no surprise that the metros with negative net absorption also were among the metros that saw occupancy rates fall. Fort Lauderdale, Fort Worth, Nashville, Palm Beach and Richmond each ranked in the top 10 for both vacancy declines and effective rent growth. On the opposite end of the spectrum, Austin, Jacksonville, Los Angeles, Orlando and Phoenix each ranked in the bottom 10 for performance in these same metrics.

What is next for the sector? Higher interest rates and softening demand have reduced construction activity, causing expected new inventory growth to moderate greatly in 2025. Unfortunately for 2024, the train has left the station for many projects. Moody’s verification and monitoring process for planned, proposed and under-construction projects puts 2024 completion totals at a well-above-average 200 million square feet. Subsequently, rent growth will experience moderate to below-average performance during the next 12 to 18 months. Again, given the still-historic tightness in the market, we are reluctant to forecast a “cratering,” but downside risk is currently greater now than at any time in the past few years. ●