As of this past June, the U.S. economy had officially entered a recession, the national unemployment rate stood at 13.3% and the Federal Reserve had taken a conservative stance regarding the pace of recovery. At that time, about 30 million jobs had been lost since the outbreak of COVID-19 in early March.

In contrast to the financial crisis of 2008-2009, however, job losses were not yet concentrated in industries that occupy the bulk of commercial office space, leading some analysts to be cautiously optimistic about this sector. But data from Moody’s Analytics Reis indicates early-stage market stress, so continued weakness will persist for the next couple of years. Additionally, the pandemic is likely to cause structural change to the long-term geographic and space requirements needed by office-property owners.

As a result of this unprecedented event, adjustments to labor usage and company locations are expected to occur. And if the scale of these changes is large enough, there will be significant impacts on office space and capital markets.

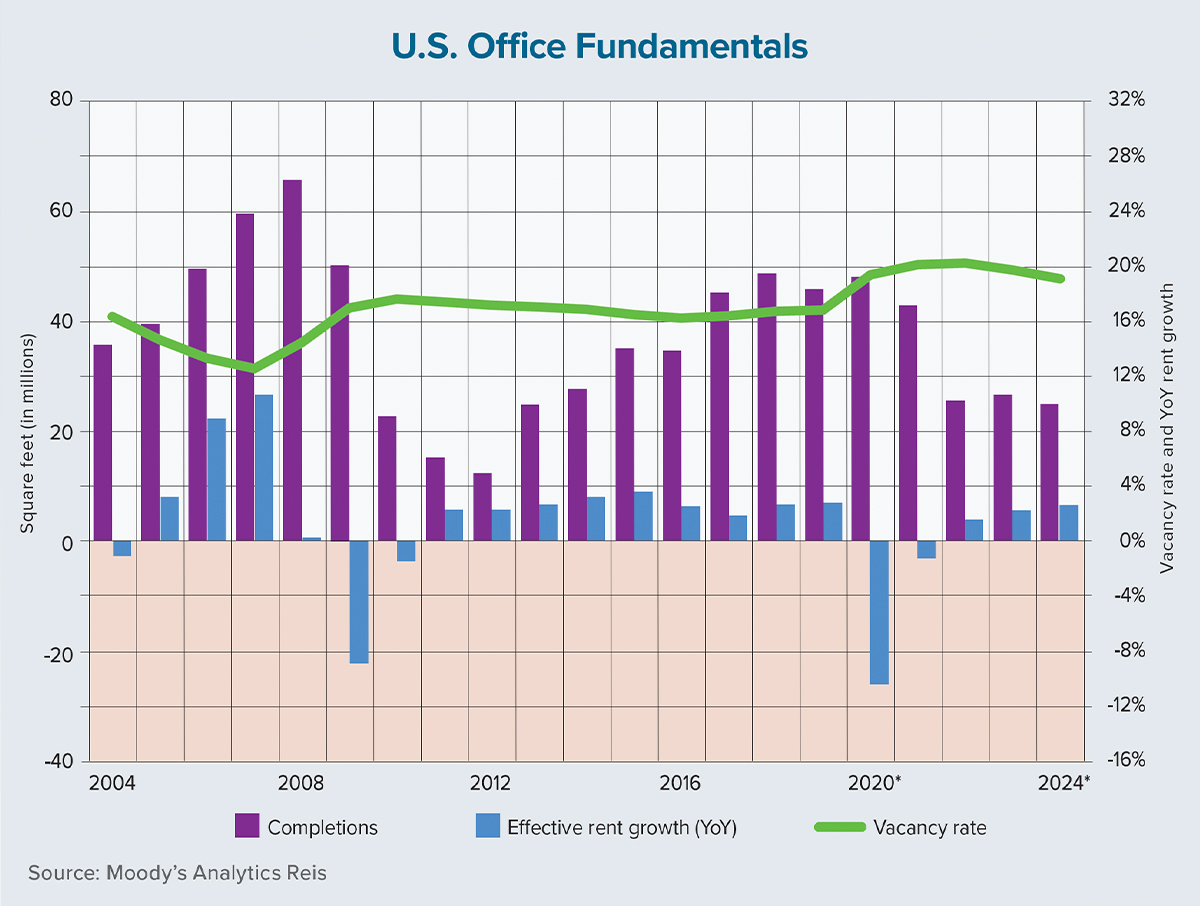

Shelter-in-place mandates and limited consumer demand severely slowed economic activity by the end of this past March. First-quarter 2020 inventory growth was minimal, but absorption was even more sluggish, causing the national vacancy rate to increase to 16.83%, its highest level since 2014. Effective rents in the first three months of this year rose year over year by a modest 0.4%, but this indicated a calm before the storm. Our models indicate the U.S. vacancy rate will end this year at 19.37%, with a 10.54% annual decline in effective rents.

Although many of the midrange calculations will be dictated by the creation of a COVID-19 vaccine, as well as the potential for a second wave of infections, vacancies are not expected to peak until 2022. Even though absorption will return to positive status in 2021, the pipeline of more than 100 million new square feet of office space due to come online by the end of 2022 will exert great pressure on occupancy rates and rents.

Offices are a microcosm of urban environments as workers are gathered into a central location to spur collaboration and productivity. But with communications infrastructure now proven to accommodate large-scale work-from-home arrangements, as well as persistent concerns about COVID-19 and future pandemics, companies may finally be pushed into thinking seriously about two important factors that will affect future demand for office space.

The first factor is geographic reallocation. It is no coincidence that COVID-19 outbreaks have clustered around major cities like New York, Seattle and Los Angeles. The same attributes that make these cities desirable places to live and work — the spatial clustering of businesses, cultural centers, households and service establishments — are predisposing them to the spread of the virus. Large-scale movements away from their current metropolitan base may prove too costly for many companies, but to minimize the risk of future pandemics, suburbs may be an attractive alternative.

The second factor, which is a bigger long-term risk, is a drop in space-usage intensity. Executives are already making bold statements regarding the future of workplaces. In fact, a March 2020 Gartner survey of 317 executives noted that 74% intend to permanently shift some employees to remote work. If this comes to pass, the office sector may struggle with a permanent shock to demand. The magnitude of distress may be comparable to that of the retail sector and its response to shifts in consumer spending toward online sales.

The evolutionary processes prompting change in the office sector — demographic shifts, economic development and technological advances — will be kicked into high gear because of the COVID-19 pandemic. Suburban offices may return to favor at the expense of central business districts, while the decline in the intensity of office-space usage may accelerate significantly. ●