The single-family rental (SFR) housing market was once a relatively niche sector of commercial real estate that was typically reserved for small-scale investors. Today, however, it is increasingly emerging as a power player in the landscape for institutional owners of residential properties.

While single-family homes historically were the exclusive purview of owner-occupants with the goal of homeownership, SFRs are becoming an increasingly popular housing option on the demand side due to a plethora of affordability issues. These barriers include house price appreciation that vastly exceeds wage growth and mortgage rates that make renting less expensive than owning. These obstacles plague the millennial generation in particular, many of whom have reached 40 years of age without the ability to climb even the first rung of the property ladder by purchasing a starter home.

Single-family rentals have been around for many years, but their broad commercialization has led to product differentiation. The two main products now available are those in build-to-rent (BTR) communities and those drawn from the existing housing stock that are located in primarily owner-occupied neighborhoods. The former typically involves new (or relatively new) construction with a plethora of amenities that mirror traditional multifamily homes. The latter is usually an older product than a BTR home, and it tends to be better managed and maintained when owned by an institutional investor rather than a small mom-and-pop operation.

Even institutional owners, however, are constantly reevaluating their holdings within the existing housing stock. They frequently dispose of older properties at higher capitalization rates and buy newer properties at lower cap rates, which garner savings by being less costly to maintain in the long run. Properties with lower cap rates are generally newer and in better condition.

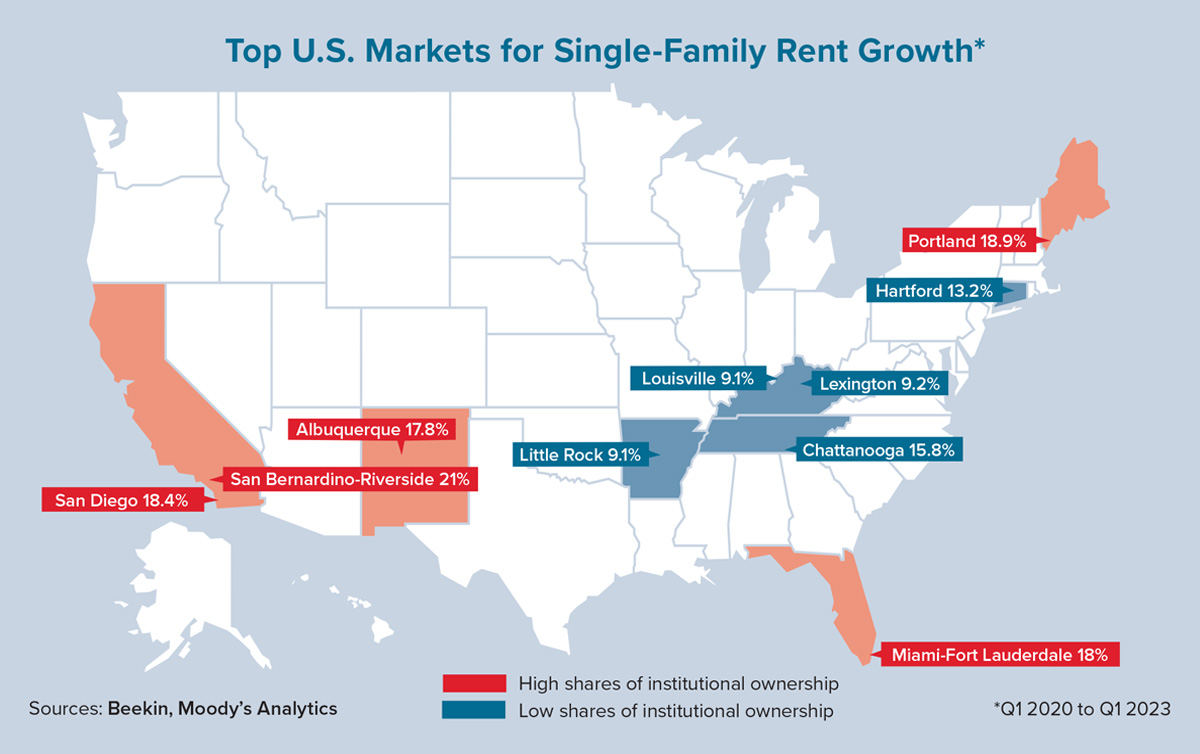

Rents are a significant portion of the cap rate calculation, which is derived from the net operating income and the market value of the property. So, how do single-family rents vary by metro area based on a significant presence of institutional investors in the area’s SFR sector? Using quarterly indices from real estate data analytics firm Beekin, we calculated single-family rent growth from first-quarter 2020 through first-quarter 2023.

For context, SFR holdings by real estate investment trusts (REITs) increased by 5.6% from Q4 2019 through Q4 2022. The top-five metros for highest rent growth and a strong presence of institutional ownership (as categorized by the metros in which publicly traded single-family rental REITs operate) posted firm double-digit growth during the three-year period ending in Q1 2023. The Southern California hub of San Bernardino-Riverside led the way with rent growth of 21% for single-family properties.

Meanwhile, metros where institutional owners do not have a strong presence also experienced healthy rent growth, although not as robust. Only Chattanooga, Tennessee, and Hartford, Connecticut, posted double-digit rent increases during these three years. While it may seem that institutional investors are primed to move into these metros due to strong rent performance metrics, they must be able to achieve economies of scale to realize the profit margins they seek. This often entails owning a vast portfolio of at least 1,000 properties in a concentrated area, which is not easy to build up in a short period of time from the existing stock of homes without a strong market shock (e.g., a deep recession). In these metros, it is more likely that investors will look to develop or acquire BTR assets to achieve scale quickly.

Due to the aforementioned reasons related to the quality differential between institutionally owned homes and those owned by small investors, metros that have a strong presence of institutional ownership will likely command higher rents. Additionally, institutional operators are more willing than smaller ones to accept a temporary dip in occupancy to secure a higher rent. This is because the impact on their overall net operating income due to a short-term vacancy is much smaller. ●