Many major retailers have announced significant store closures over the past two years. Throughout this period, observers have anticipated reports of soaring vacancy rates and plummeting rent prices. Yet the data has shown otherwise, defying the anecdotal reports of a retail apocalypse.

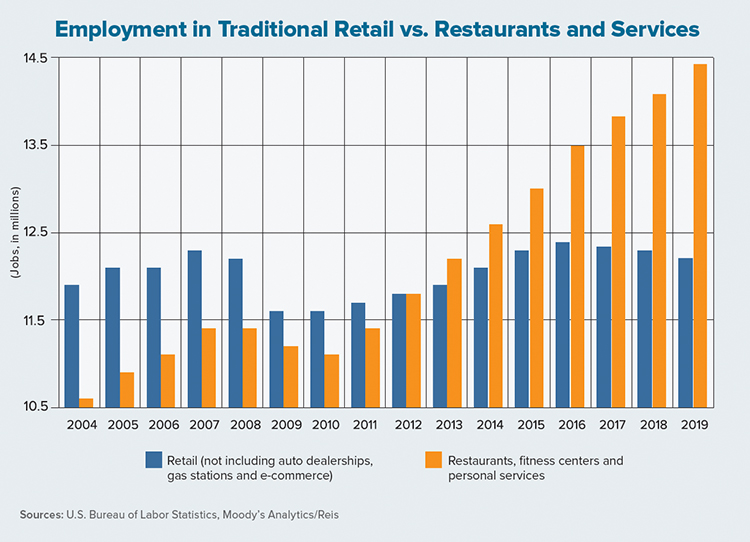

This is largely due to new tenants — including trampoline parks, fitness companies and new grocery stores, among others — occupying the vacant space. The chart on this page substantiates the anecdotal evidence that businesses in the entertainment, leisure and fitness sectors are growing as other retailers contract.

The collective restaurants, fitness and personal-services category (highlighted by the orange bars on the chart) added about 300,000 jobs per year, on average, from 2016 through 2019 for a cumulative growth rate of 6.9%. Meanwhile, retailers in traditional mall and shopping-center spaces — not including auto dealerships, gas stations and e-commerce companies — cumulatively shed 180,000 jobs over the past three years for a net decline of 1.5%. In short, a small segment of service-oriented industries grew and filled enough space to support the retail real estate market during this period.

The year-end 2019 data from Reis Inc., however, indicates that the balance between store closures and tenants leasing new space started to tip toward increased vacancies, since the retail vacancy rate increased 0.1% and the mall vacancy rate increased 0.3% in the fourth quarter of last year. At the same time, quarterly rent growth for retail was 0.1% — the lowest figure since 2012 — and the average mall rent was unchanged. Given these numbers, one cannot help but wonder if this was the start of a retail downturn or if it was simply a weak quarter.

Looking at other commercial real estate sectors, we see that the apartment and office markets also slowed a bit in fourth-quarter 2019. Indeed, given the U.S. Treasury bond yield-curve inversion this past August and the protracted trade war, many retailers were likely hesitant to make major leasing decisions late last year. Job growth picked up significantly this past November while the U.S. and China agreed to a “phase one” trade agreement shortly after the start of 2020. The federal funds rate was lowered three times in the second half of last year and interest rates settled down.

Will the healthier macro-level statistics near the end of last year reverse the fortunes of the retail sector? Or will retail continue to suffer at the hands of online shopping and store closures? Like many real estate questions of this type, the answer depends on the metro area or region in question.

Some metros are simply “over-retailed,” meaning they have an oversupply of these properties. A measure we have analyzed in the past (retail jobs per 1,000 residents) provides an objective metric of whether a metro is over-retailed relative to its peers.

Three metros that saw rent declines in the past quarter or year have a high ratio of retail jobs per capita. Lexington, Kentucky for example, had 58 retail jobs per 1,000 people in 2018, while suburban Virginia’s ratio was 54 and Pittsburgh’s was 52. These three metros were in the top 25 rankings of retail jobs per capita (the nonweighted U.S. metro average was 49). Many metros at the low end of this scale, however, did not see rent declines.

In short, the retail sector continues to be in transition. Although restaurant, fitness and entertainment companies are filling retail spaces vacated by big-box stores, the momentum may have shifted in fourth-quarter 2019 as vacancy rates started to rise. One quarter does not equate to a trend, however, and the end of last year was affected by a heightened trade war and other macroeconomic uncertainties that could reverse course in 2020. Indeed, many metros are seeing growth but, as the cliché goes, location is still paramount in retail.