The effects of the COVID-19 pandemic on U.S. commercial real estate have been wide-ranging. The industrial- property sector has grown and multifamily housing experienced early declines before steadying itself, while office and retail have only recently started to show evidence of their anticipated stress.

The fortunes of niche property sectors have followed suit. Outcomes for the senior-, student- and affordable-housing segments have exhibited variation in the form of steadiness or slight declines. Self-storage properties, however, have been a bit of a bright spot. Fallout from the pandemic has pushed the sector from a laggard to a leader.

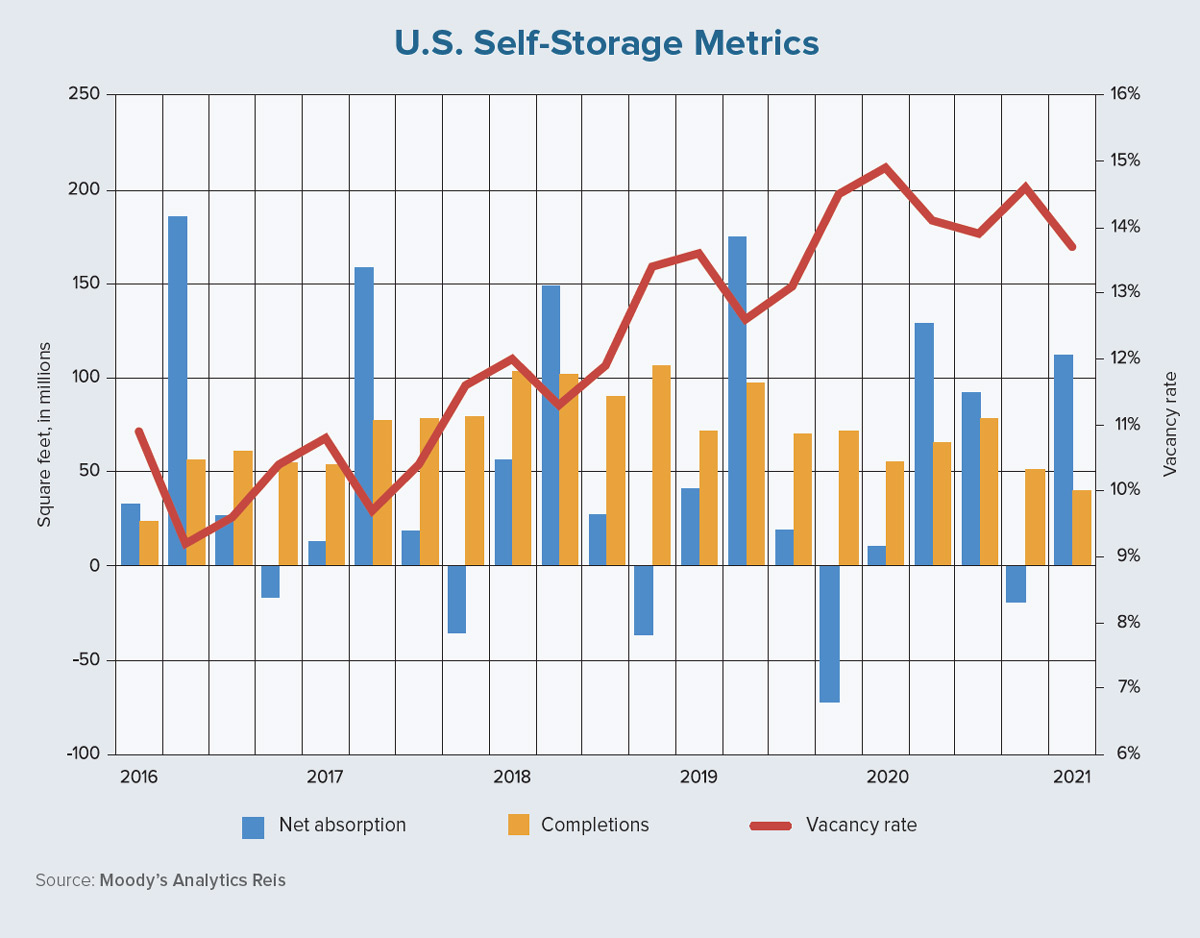

Prior to the health crisis, self storage was floundering. A glut of development, which started during the tail end of the Great Recession and accelerated throughout the ensuing expansionary period, placed downward pressures on rent prices and occupancy rates starting in about 2016. Net absorption remained solid throughout the latter portion of the expansion, averaging 196,000 units per year from 2016 through 2019, but this wasn’t enough to balance the inventory gains that averaged 311,000 units per year during the same period, according to Moody’s Analytics Reis data.

Consequently, over this four-year period, rent levels pulled back slightly and the vacancy rate increased from 10.4% to 14.5%. A lack of migration, which tends to slow demand, combined with the relative ease and low cost associated with constructing these facilities, brought the market out of balance — a somewhat typical state for this sector. More than any other asset class, self-storage facilities tend to fluctuate through higher peaks and lower valleys due to the low barriers of entry for investors, as well as fickle tenant demand paired with the typical monthly lease structure. At the end of 2019, the market was in one of these valleys.

The COVID-19 crisis turned out to be the shot in the arm needed to jolt the sector out of its malaise. During the early stages of the pandemic, the self-storage market gained stability that it maintained throughout the course of 2020. As construction slowed to only 40,000 units completed nationwide in first-quarter 2021 and net absorption grew to more than 100,000 units during these three months, the vacancy plummeted by 90 basis points to finish the first quarter at 13.7%. Simultaneously, annualized rent growth accelerated to a healthy 2.9%.

Why did this growth occur and will it continue? Although it’s not acyclical, the self-storage sector tends to thrive on economic and societal changes. These shifts may be based on negative economic pressures — for example, downsizing from single-family homes to apartments during the Great Recession. Changes also can be based on shifting demographics or even shifting lifestyles.

The pandemic has undoubtedly accelerated the acceptance of a remote-work lifestyle. This phenomenon has prompted migration, a well-cited and rational factor for self-storage use. Further, remote work has required the creation of many home offices, often in places they were never intended. These redesigns or renovations drove the need for space to store furniture and other household items that were “in the way.” Finally, many college students and recent graduates have had their educational or employment plans delayed, forcing the storage of their dormitory or apartment furnishings.

Moving forward, self storage will continue to reap the benefits of migration and catch the tailwinds associated with a strong economic recovery. As people adjust to post-pandemic life, many will find new locations to better fit their new lifestyles.

Additionally, gross domestic product growth is expected to approach 7% this year and 5% in 2022, with much of the growth based on the spending down of excess household savings built up during this past year. While much of this cash will be spent on travel, sizable portions will be used to buy durable goods and other household items. Some of these goods, or the goods they are replacing, will find their way into self-storage facilities. ●