The U.S. apartment market has outperformed its peer property-type groups, both in terms of occupancy and rent growth, with annual rent growth averaging 4.9% from 2014 to 2019 and annual occupancy growth averaging 2.1% over the same period. This is no surprise to anyone who is active in the multifamily-housing market. What is a surprise is how well the multifamily sector has done this year despite concerns that the economy has slowed — and may continue to slow — over the next few years.

First, the U.S. economy only slowed moderately through the first three quarters of this year. Employment growth for the first nine months of 2019 decelerated to an annual rate of 1.6%, down from average growth of 1.9% over the past five years. Meanwhile, gross domestic product growth for the first three quarters of this year decreased to 2% annually, down from its five-year average of 2.6%.

Growth rates may not be robust, but they are healthy. And they are reflected by the numbers in the apartment market, where occupancy growth slowed slightly to 1.8% and asking rents dipped to 4% year-over-year growth for the first three quarters of this year.

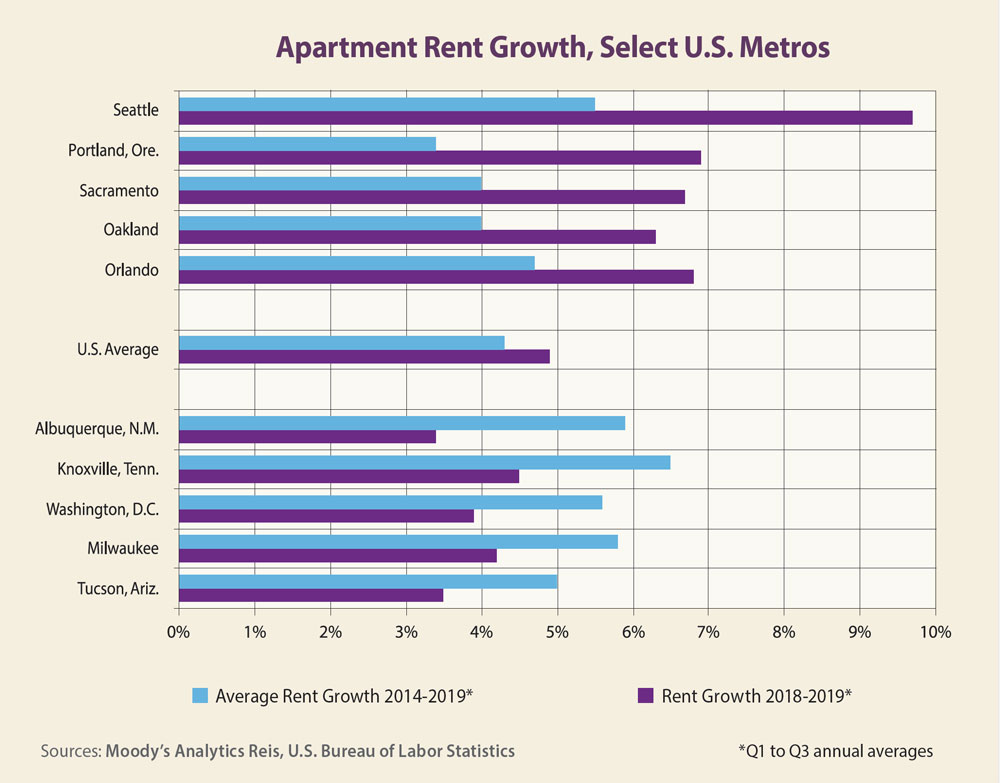

Still, a deeper look shows that a number of metro areas that were seeing strong rent growth have moderated a bit, while other metros with weaker rent growth over the past few years had much stronger growth in 2019. As many as 23 metros saw their annual rent-growth figures for the first three quarters of 2019 exceed their five-year averages. These include some surprises, such as Albuquerque, New Mexico; Knoxville, Tennessee; Washington, D.C.; Chicago; and even New York City — which is defying the intended efforts of the city’s updated rent-control law.

At the same time, market leaders from the past five years posted rent growth in 2019 that was merely average. These metros include Seattle, Orlando, Oakland, Sacramento and Portland, Oregon. The chart on this page highlights the differences in rent growth over the two periods.

The simple conclusion one can draw from this data is that the gap between the healthier markets and the weaker ones has narrowed over the past year. This is a positive development and worth mentioning. It also is worth noting that no metro area had a year-over-year rent decline during the first three quarters of this year.

These findings contrast the U.S. office- and retail-property markets, which show a widening gap between the healthier metros and the weaker ones. In addition, a handful of cities had year-over-year rent declines in these property sectors for the first nine months of this year. Average rent growth in the office market has kept pace with inflation, while average rent growth in the retail market has trailed inflation.

A key metric for the apartment market is job growth, and only one metro area had a year-over-year employment decline for the first nine months of this year (suburban Maryland, which was down 0.1%). As many as 18 metros, however, showed higher employment growth in 2019 than their five-year averages. This group was led by Houston; Syracuse, New York; New Orleans; Wichita, Kansas; and Tucson, Arizona.

Metros with the sharpest deceleration in employment growth this year compared to their five-year averages were San Bernardino, California; Austin; Jacksonville; Raleigh-Durham, North Carolina; and Minneapolis. This is not to say that these metros have weak job growth; their 2019 rates were simply lower than in recent years.

Thus, the apartment market remains the strongest property type for investors. It could even benefit from fears that the U.S. economy is close to a downturn, as some who would otherwise elect to buy a home will choose to rent for another year until the uncertainty dissipates.

Of course, uncertainty is a constant, so those who choose to wait for less uncertainty to buy a home are likely to rent forever. That said, the demand for apartments is not likely to wane over the next few years as long as job growth remains positive.