With trade-war threats continuing to dominate the news over the past year, the media has increasingly focused on the industrial real estate sector and how a trade war could significantly harm warehouse demand.

At the same time, retailers continue to close stores or announce future closings. These include prominent retailers of the past, such as Bed Bath & Beyond, J. Crew, Party City and GameStop. The news looks even more dire than it did a year ago because these retailers join Macy’s, Kmart, JCPenney and Sears among the companies that continue to close stores this year.

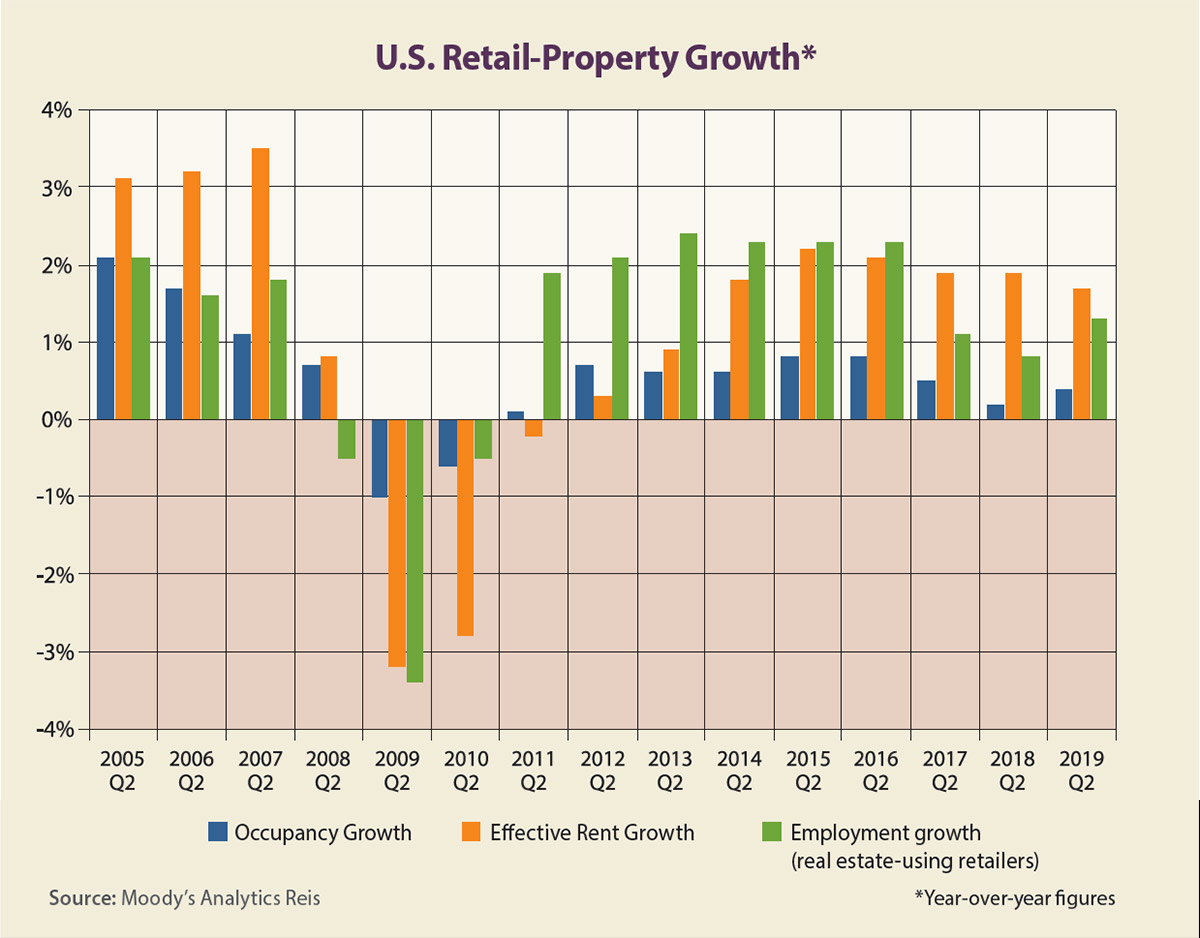

As bleak as these reports have been, the numbers on the retail real estate sector continue to tell a different story. Yes, growth has decelerated sharply, but occupancy and rent growth remain positive. The chart on this page shows that, as of second-quarter 2019, retail occupancy grew 0.4% year over year, after growing 0.2% in second-quarter 2018. Likewise, effective rent growth went up 1.7% year over year, well below the inflation rate, but rents have grown at or below 2.2% every year of this expansion.

So, how does one reconcile the positive numbers shown here with the steady store-closure announcements? Consider the retailers that are expanding — namely, grocery stores, many of which are based abroad. According to the National Retail Federation, the fastest-growing retailers include Lidl (based in Germany), El Super (based in Mexico) and Times Supermarkets (based in Japan). Other companies in the top 10 include Rue Gilt, Boxed, Wayfair, Primark, At Home, AT&T and Five Below.

Other smaller retailers are expanding. Consider that restaurants have added 134,000 jobs through the first eight months of 2019, offsetting 74,000 lost retail jobs. Other types of retailers, such as personal services (which includes dry cleaners and hair salons) have added 10,000 jobs, while fitness and recreation retailers have added 11,000 jobs.

These service providers continue to expand in traditional retail spaces. To get a better sense of how these businesses stack up, we aggregated all of the retail-industry categories (excluding gas stations, automobile dealers and e-commerce or “nonstore” retailers), then added personal-services and fitness providers to show how the “real estate-using” retail category has grown. The chart on this page includes this category. The annual employment gains for these businesses are consistent with retail occupancy and rent gains.

Finally, consider that the national numbers here are based on the Moody’s Analytics Reis average of 80 metro areas. Many closed stores are in tertiary metros or rural areas outside of our coverage area. Our 110 tertiary metros show slight occupancy declines in 2017 and 2018, but there was growth of 0.3% in second quarter 2019. The average retail rent in these tertiary markets grew 1.3% year over year as of the past second quarter, in line with the average of primary markets.

Still, these averages represent a blend of healthy markets and weaker ones. Metros with significant tourism industries have seen the highest retail-rent gains, including Nashville, Orlando and Jacksonville. Those that have seen the steepest rent declines are mostly in the Northeast or Midwest regions, including Hartford and Fairfield County, Connecticut; Cleveland; and Lexington, Kentucky.

In short, the retail sector continues to see considerable restructuring as older retailers shrink their footprints, while others expand. Store closures continue to make headlines, but it is important to look at the numbers to get a true sense of the retail landscape.