In many U.S. metro areas, development of new self-storage facilities has gotten a bit out of control. The top 50 self-storage markets in the nation have seen supply growth of 15.5% over the past five years, well ahead of the 13.3% occupancy-growth figure during the same period. As a result, the U.S. market is oversaturated and rents are declining across the board.

The self-storage industry, which has long been a favored asset of seasoned commercial real estate investors, saw tremendous growth in the first few years of the current U.S. economic expansion as more people moved into urban-area apartments with limited storage space. By 2015, developers who sensed growth potential ramped up new construction or began converting former industrial space into storage facilities.

Building these facilities is less costly than many other property types and thus the entry barriers are lower. New self-storage properties seemingly pop up overnight in some markets, particularly in older, converted warehouse buildings.

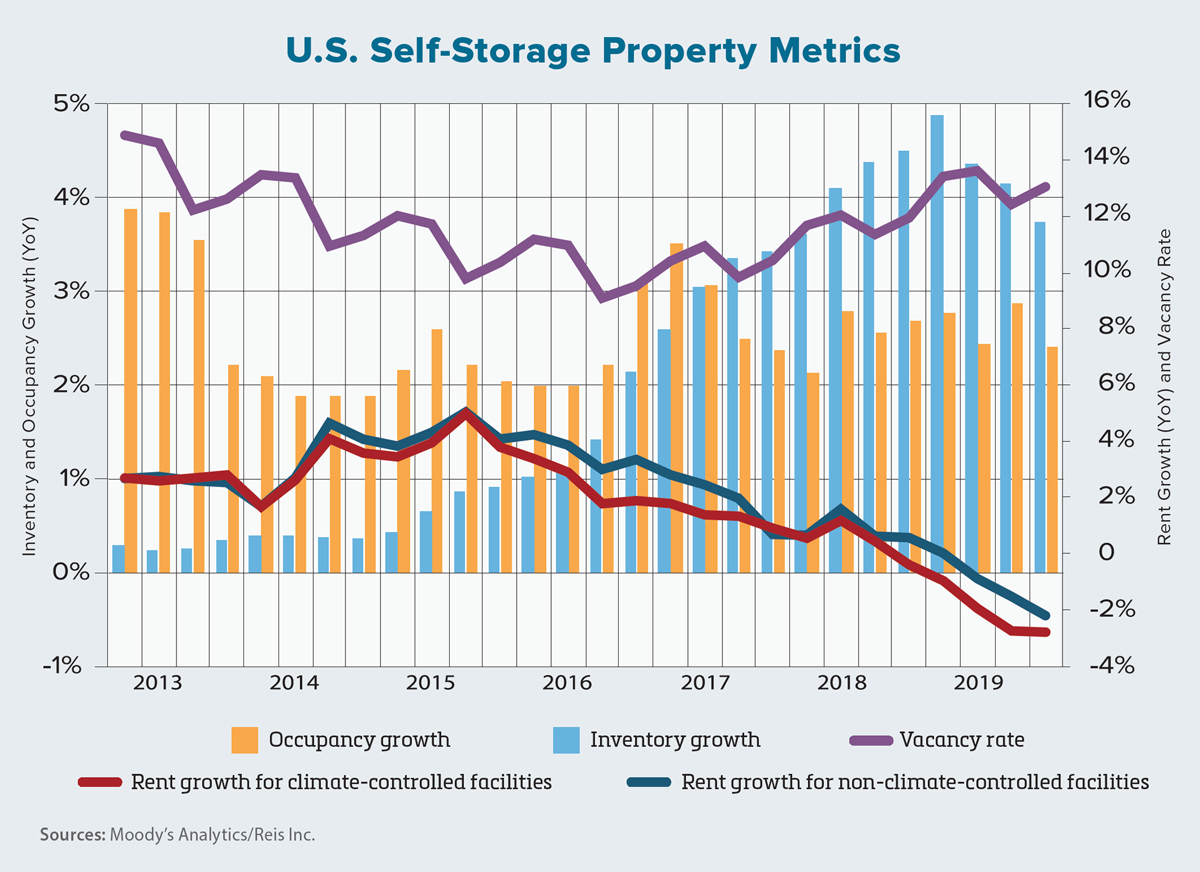

The chart on this page shows how the self-storage sector has evolved since 2013. Indeed, more than any other property type, the self-storage market is acutely cyclical. Demand rises in the second quarter of the year before steadily slowing in the following three quarters. This is apparent when viewing the bumpy vacancy-rate trend on the chart.

Note the strong demand growth from 2013 through 2015. The rate of supply growth, however, slowly began to catch up to demand by 2016. After the market achieved balance for about a year, supply growth then accelerated while demand growth stayed relatively flat. As a result, the vacancy rate started to rise in late 2017 and continued to do so through third-quarter 2019.

Rent growth has clearly followed the rule of supply and demand. That is, the excess supply growth starting in 2017 not only began to ease pressure on rent growth, but rents subsequently declined over the past year. Annualized rent growth in the third quarter of last year was negative 2.9% for climate-controlled 10-by-10-foot units and negative 2.3% for non-climate-controlled 10-by-10-foot units.

Some U.S. metros and regions are more out of balance than others. From 2016 through third-quarter 2019, the Southwest and South Atlantic regions had the largest supply-growth imbalances. Consequently, they also saw the sharpest drops in annualized rent growth during the first three quarters of last year.

The rent declines for the two categories of self-storage facilities, however, are deeper in the Southwest than in the South Atlantic. This is likely due to the relatively higher 2019 vacancy rate of 14.7% in the Southwest states, compared to 13.9% in the South Atlantic states. In contrast, the West region had the smallest imbalance in supply growth over these three-plus years, as well as the lowest vacancy rate and the smallest annual rent declines in 2019.

Lastly, the supply imbalances in the Midwest and Northeast regions are less severe than what is occurring in the Southwest and South Atlantic states, but they are larger than that of the West. As a result, their respective rent declines are comparatively moderate.

The self-storage industry has plateaued and future supply growth is expected to slow considerably. Vacancy rates and rents should remain flat in most metros. That said, it is important to consider differences across regions and metros, since doing so can yield opportunities that buck national and regional trends.

Just as important, however, are changes in local economies and demographics. Areas with large numbers of college students or baby boomers may continue to see higher demand. Still, it pays to know the self-storage market and where these properties are overbuilt. Supply growth has clearly had a deeper impact than demand on self-storage trends over the past few years.