This year marks the fifth edition of Scotsman Guide’s Top Women Originators, the benchmark ranking that highlights the exceptional performance of women in the mortgage industry. Since 2019, the company has expanded its print ranking from 200 women to 300 women — and sales volumes have soared.

Our rankings in the past two years reflected the sky-high origination volumes of 2020 and 2021, which were tied to historically low interest rates and a refinance boom. While these rankings were our largest ever, this year’s list shows significant growth from the 2020 rankings, which reflect the last “normal” year of the housing market in 2019.

In 2019, the first year that Scotsman Guide published an extended online rankings list for Top Women Originators, 635 women made the cut for an aggregate loan volume of $43.8 billion. This year, 762 women qualified with total originations of $52.3 billion.

The volume for the winning individual has also grown significantly in this time, from about $240 million to more than $400 million. And even though volumes fell compared to last year, the Top Women Originators are still doing more business than they were prior to the COVID-19 pandemic.

The 300 women on this year’s list also represented a larger share of our Top Originators, an annual ranking that was published last month. Women increased their representation on the Top Dollar Volume list from 26% in 2022 to 29% in 2023. Back in 2020, women accounted for 24% of the Top Dollar Volume list.

This year’s top spot went to Kelly Malatesta of Cadence Bank, who originated $416.2 million in loans during the 2022 production year. Malatesta is no stranger to the rankings, working her way to the top after taking seventh place in 2021 and fourth place in 2022. Malatesta is also this month’s Featured Top Originator. You can read about her niche and the strategies that brought her success on Page 18.

Second place went to Parker Borofsky of Movement Mortgage, who increased her volume in difficult market conditions by nearly $20 million to finish with $323.1 million in 2022. Her remarkable increase rocketed Borofsky up from 27th place last year.

You’ll find the 300 highest producers on the next few pages alongside summaries of new and relevant data about women in the workplace. For the full list of 762 Top Women Originators, visit scotsmanguide.com.

Next month, we’ll take a break from ranking individual originators to publish the Top Mortgage Lenders rankings. This is a list of the nation’s largest lenders by sales volumes and includes many of the employers of our Top Originators. In July, we’ll return with the Top Veteran Originators rankings.

Have a wonderful May and enjoy the spring blossoms. As always, thank you for reading.

— Hannah Darden, industry rankings editor

Verification: Hannah Darden, Brian Warr

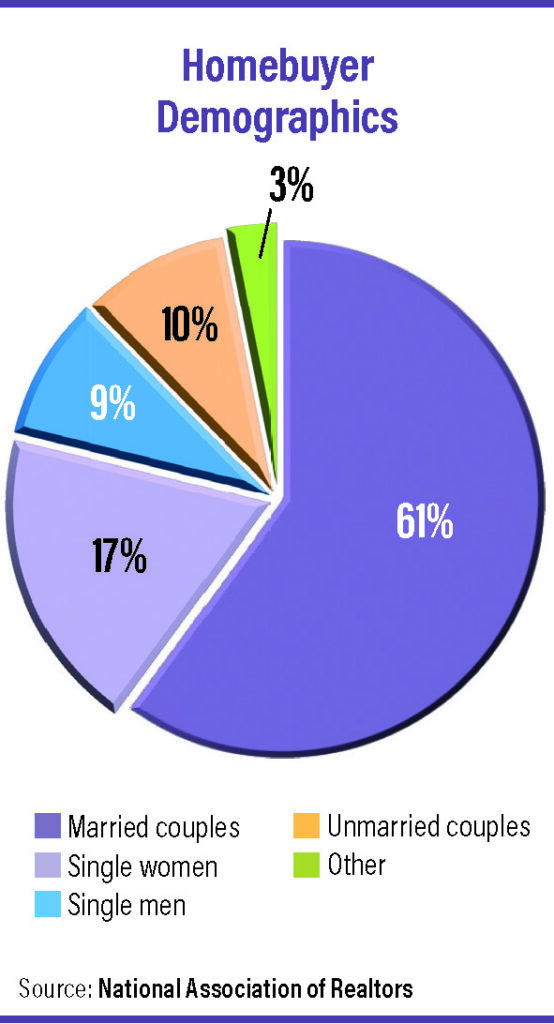

Single women remain second-largest homebuyer demographic

Single women made up 17% of all homebuyers last year, according to the 2023 Home Buyers and Sellers Generational Trends report from the National Association of Realtors (NAR). Single women came in second to married couples, who made up the lion’s share of buyers at 61%. Unmarried couples made up 10% of homebuyers with single men at 9%. Last year, the share of first-time homebuyers fell from 34% to 26%.

Single women have consistently been the second-largest buyer demographic. And Generation Z (ages 19 to 23) has the highest representation, with single women comprising 31% of Gen Z homebuyers. Married couples come in a close second among Gen Z at 30% while single men also have a large share at 25%. Unmarried couples account for 13% of Gen Z buyers, making the spread across Gen Z much more even than other age groups. Gen Z also doubled its representation from last year, growing from 2% to 4% of all U.S. buyers.

Millennials, who have been the largest generational homebuyer group since 2014, were dethroned by baby boomers in the newest report. Millennials made up 43% of buyers in last year’s report, but only 28% this year. Boomers, meanwhile, grew their share from 29% to 39% during the same period. Boomers also made up the largest share of sellers at 52%.

Women are switching companies more often than ever before

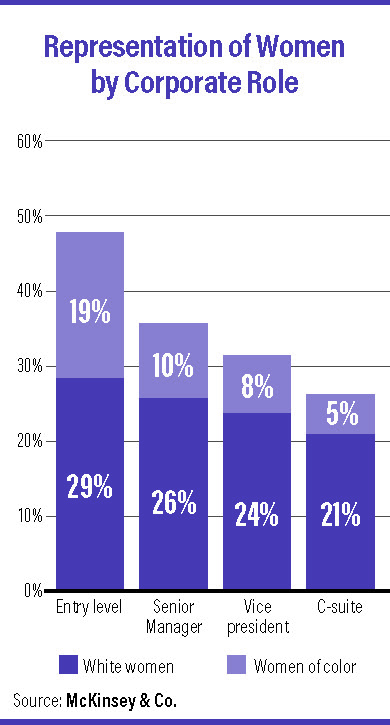

Companies must do better to retain women in leadership positions and to attract the next generation of women leaders. This was the main takeaway of McKinsey & Co.’s 2022 Women in the Workplace report, the largest study of women in corporate America.

Women are starting to ask for more at work and are willing to go somewhere else to get what they want, the study found. Women want opportunities for advancement, recognition for their work, better flexibility, and company commitment to diversity, equity and inclusion. All women (but especially women of color, disabled women and LGBTQ+ women) reported microaggressions that make it difficult for them to advance at work.

Women leaders are switching companies at the highest rate ever recorded in the study. And the factors causing women in leadership to leave their companies are also deeply important to young women in the workforce, who are more likely to be women of color and LGBTQ+. To maintain inclusive, diverse teams, companies must retain and attract women.

How do they do this? McKinsey suggests finding and fixing their promotional gaps — in which men are more likely to be promoted — and by implementing high-quality, equitable programs and training courses.

Men and women disagree on workplace equity

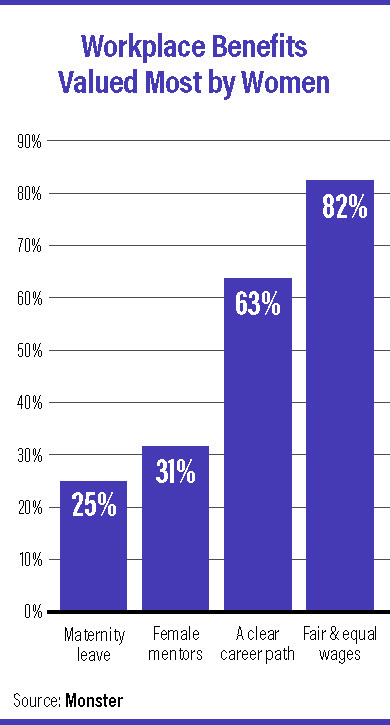

In conjunction with this year’s International Women’s Day (March 8), job search website Monster released the results of a poll it conducted among more than 6,800 workers. The results showed that men’s and women’s opinions on equality in the workplace differed greatly.

Men tended to view workplaces as more equitable than women did. Three-quarters of men believed that men and women are paid the same at their place of work, but only one-quarter of women said the same. Sixty-three percent of men felt that both genders were treated equally and fairly, but only 31% of women agreed. And while 66% of men thought all employees at their company received the same quantity and quality of opportunities, only 23% of women agreed.

When it comes to who gets opportunities at work, the differences were especially stark. More than 70% of women believed that men get a seat at the table more often than women. Only 9% of men agreed. Conversely, 74% of men believed that women received preferential treatment while only 4% of women concurred.

Women were also more likely to turn down a job offer if a company didn’t offer opportunities for women and/or flexibility and time off for parents. While 37% of women said they would turn down a job offer that didn’t have adequate flexibility for working parents, only 21% of men said the same. And while 30% of women insisted on adequate parental leave or childcare benefits, only 18% of men did.

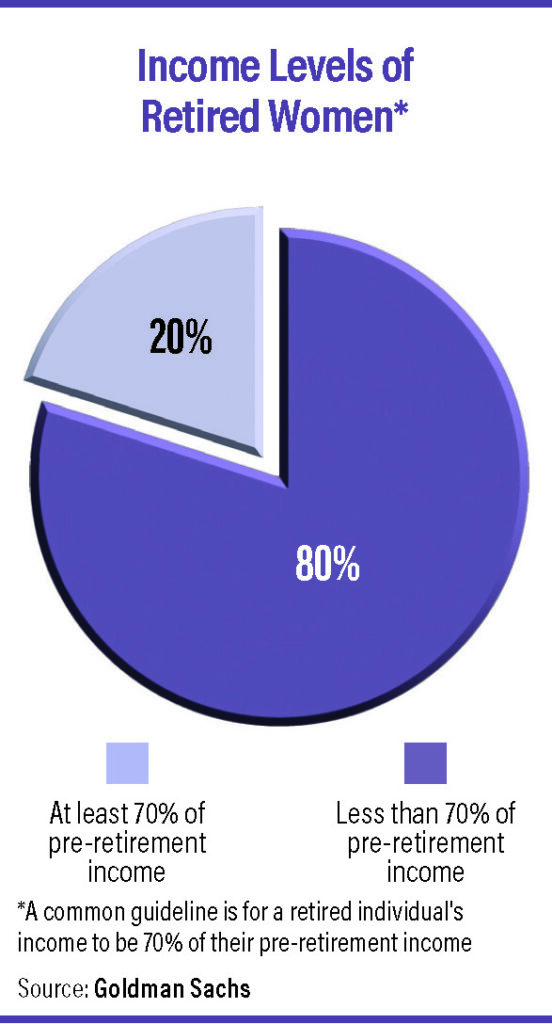

Women face unique challenges when saving for retirement

Women must stretch smaller retirement funds over longer life expectancies than men, a recent report from Goldman Sachs found. The report evaluated responses from both working and retired individuals across genders and generations. According to the report, women comprise 47% of the U.S. workforce but control only one-third of all household financial assets. Women also earn 21% less income than men during their lives.

Due to lower earnings, the average woman makes 30% fewer contributions to retirement funds than a man. At the same time, women live longer and must plan for additional time to stretch savings. The report found that across the “financial vortex” — a mix of competing financial priorities and life events — a woman’s ability to save for retirement was impacted more than a man’s even as they share the same financial responsibilities.

Six in 10 retired women in the survey said they retired earlier than they planned while 66% said they retired for reasons out of their control, due to external factors such as personal health or taking care of a family member. Additionally, while 36% of retired women reported taking time away from the workforce to care for children or other family members, only 21% of retired men did so. On average, women have nine fewer years of earned income, which also affects their Social Security benefits.