The rollout of multiple effective COVID-19 vaccines has put a full return to the office within sight. Many large U.S. companies now have credible timelines of a summer or autumn 2021 revival. But what does this “full return” actually entail?

Will all workers come back five days a week and will the office even vaguely resemble what it was prior to the pandemic? As time passes, the path forward becomes a bit clearer, and this specific path will determine quite a bit for commercial real estate stakeholders.

We expect the share of employees who work from home at least one day per week to rise considerably in a post-pandemic world. Evidence of this is provided in 2020 surveys from the Atlanta Federal Reserve and the U.S. Bureau of Labor Statistics in which more than 40% of traditional office-sector employees were reportedly working from home at least part time.

On the surface, this seems to present major issues to office-property owners and investors, but deeper analysis suggests that this may not be the case. This past June, the Atlanta Fed followed up on its original survey and asked employers about their office-space needs. Not only did the majority of respondents not expect large reductions, but many reported the need for slight increases in space.

Why the seeming contradiction? The simple answer is that many employers are still requiring employees to be present in the office at least part time. This requires space, and even if the sharing of desks becomes the norm, these desks are likely to be socially distanced. Additionally, it is probable that more collaborative space will be needed as office-using employers lean toward bringing in teams on the same days in the hopes of sparking creativity and innovation that may not be replicated on a virtual platform.

Furthermore, many of these employers expect growth. The U.S. economy is centered on knowledge creation and business services, industries that are disproportional users of office space. Moody’s Analytics Reis anticipates employment growth of nearly 20% for professional and business services over the next decade, which will make office space increasingly valuable even if many workers only use it on a part-time basis.

Assuming many workers return to the office in some capacity, where will these spaces be located? Some schools of thought predict the death of the central business district (CBD), or a mass migration of companies to less expensive and emerging warm-weather cities. There is some evidence that suburban markets are presently holding up better than CBDs, but the data is not yet conclusive.

At the metro level, cities such as Austin, Denver and Raleigh gained a fair share of attention even prior to the pandemic, and momentum seems to be continuing there. Anecdotal evidence — such as Oracle moving its headquarters to Austin — combined with recent rent and vacancy data, confirms the strength of these cities.

Phoenix and Raleigh, for example, ended 2020 with year-over-year reductions of least 60 basis points in their office-vacancy rates, according to Moody’s Analytics Reis. Although we are certainly not pronouncing the death of density or the end of large, “old guard” business centers, we do anticipate a divide between the emerging and old-guard cities to continue over the next couple of years before both sets of markets recover later this decade.

Our 2021 annualized average effective-rent forecast for the “old guard” office markets (such as Chicago, New York City, Los Angeles and San Francisco) is negative 8.3%. But the yearly rent decline for emerging office markets such as Atlanta, Charlotte, Dallas and Nashville is expected to be only 5.5%.

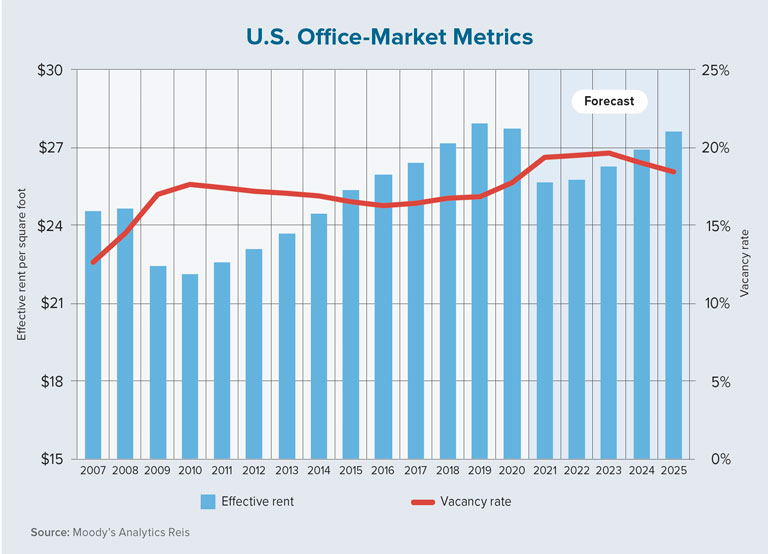

Lastly, from a national perspective, 2021 will be a difficult period for the office sector. A seismic shift in the demand for square footage is unlikely, but as the chart on this page shows, there will be a transition period for the sector. A typical lag in commercial real estate market stress is likely to occur, followed by a slow and steady return to pre-pandemic rents and vacancy rates. ●