The domestic hotel sector has suffered more so than any other property type during the COVID-19 pandemic. Business travel and tourism have significantly declined due to shutdowns and health risks.

Data from the U.S. Bureau of Economic Analysis shows that hotel output dropped by 65% from fourth-quarter 2019 to second-quarter 2020 — exponentially higher than the overall gross domestic product decline of 9%. Only the 80% decline for the air transportation industry was worse than the hotel sector during this period.

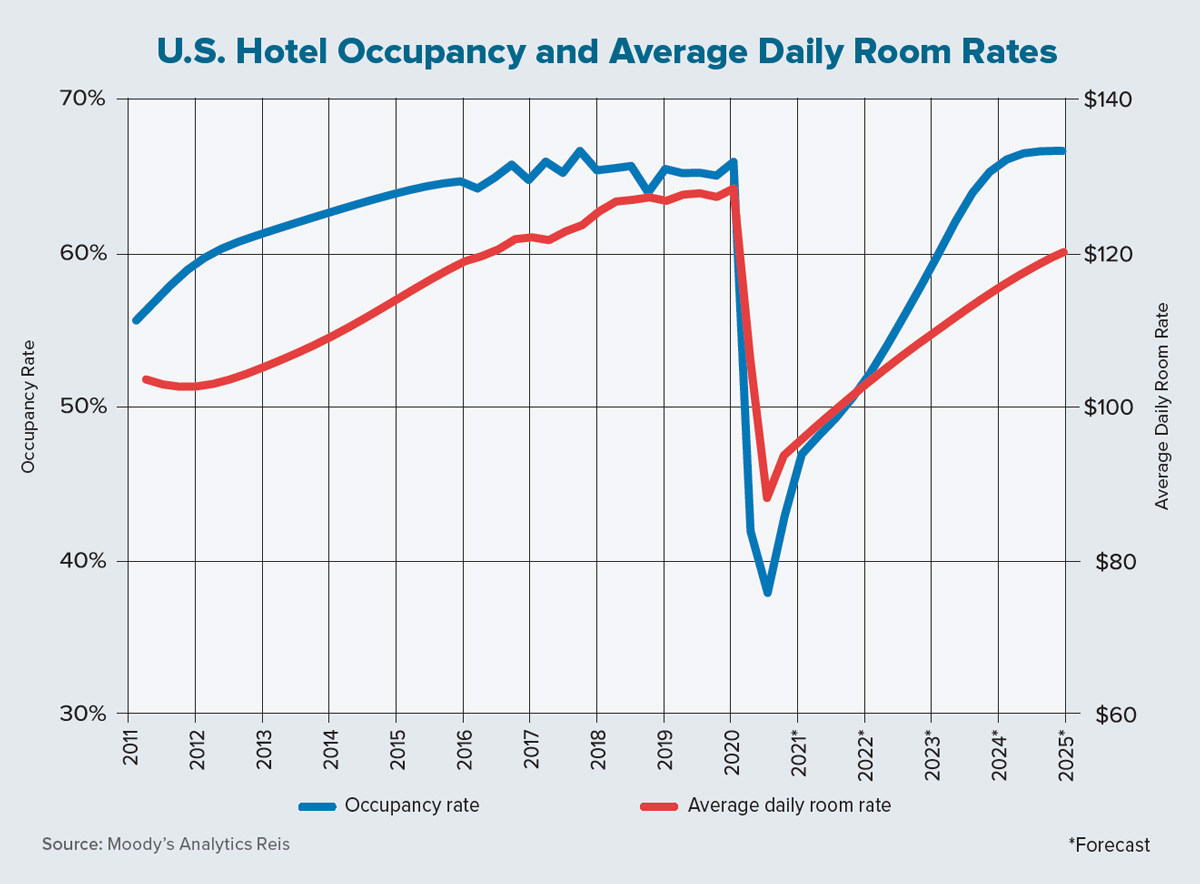

In the accompanying chart, Moody’s Analytics Reis hotel data (which sources raw data from Kalibri Labs) shows that the national hotel-occupancy rate declined from 66% in Q4 2019 to 38% in Q2 2020 before climbing to 43% in the following quarter. The average daily room rate declined by 31% during the first half of last year before rising by 6% in the third quarter. Indeed, the pandemic brought an unprecedented shock to the hospitality industry.

Our data shows that every U.S. hotel market suffered significantly, yet a number of well-known beach towns saw the smallest occupancy declines. These included Virginia Beach, Virginia and Myrtle Beach, South Carolina, as well as much of Florida’s eastern coast. Travelers drove to these destinations for extended vacations, especially during the summer months.

At the other end of the spectrum were destination markets such as Las Vegas and Orlando, along with northern urban markets such as Chicago, Minneapolis and Washington, D.C. These metro areas had the steepest hotel-occupancy declines in the second quarter with only moderate gains in the third.

Still, the differences in declines for occupancy rates, room rates and revenue per available room (RevPAR) did not vary as much in 2020 compared to how disparate the growth rates were over the prior five years. In fact, the numbers clearly show that even though demand growth for hotels was robust prior to the pandemic in each of the 69 metros analyzed, supply growth varied widely. As a result, metros that had low inventory growth saw high RevPAR growth while those that had significant inventory growth saw flat or, in some cases, negative RevPAR growth.

Houston, for example, added 20,000 hotel rooms from 2010 to 2019, a growth rate of 28%. It also suffered somewhat after Hurricane Harvey struck in 2017. As a result, its RevPAR declined by 17% from 2014 to 2019. Other metros that incurred a RevPAR decline over this five-year period were Oklahoma City, Pittsburgh, Cleveland and Omaha, Nebraska — none of which are known for being tourist draws.

On the other hand, Las Vegas incurred a slight decline in hotel-room inventory during the same period. But with strong demand growth, its RevPAR grew 63% from 2014 to 2019. Other markets with low inventory growth and strong RevPAR growth during these years also are metros with a thriving tourism sector: the Arizona cities of Phoenix and Tucson, as well as Jacksonville.

New York City’s hotel sector is in a class by itself: It added more than 35,000 hotel rooms from 2010 to 2019, or 42% growth, according to NYC & Co. Visitor growth kept pace with this astounding inventory growth until the pandemic hit, then New York’s RevPAR fell by two-thirds from Q4 2019 to Q2 2020.

The Moody’s Analytics Reis forecast for these 69 metros incorporates these supply-growth numbers, but the numbers show that the primary driver in the hotel forecast is the overall economy and a metro area’s draw as a tourism destination. Business travel will recover at a slower rate than leisure travel as many have recognized that virtual conferences are effective.

The pent-up demand for traveling has grown over time. Metros within densely populated regions could see higher domestic tourism levels as road-trip vacations are substituted for more expensive ones involving flights. Many hotels will not survive the downturn, but now that a COVID-19 vaccine is starting to roll out, there is hope that more people will get out and stay in a hotel. ●