In recent months, the market has been on a roller-coaster ride, highlighted by a global stock selloff in early in August, only to have prices make a recovery and stabilize a few weeks later. A main catalyst for the market meltdown was likely July’s weaker-than-expected nonfarm payrolls report.

The Bureau of Labor Statistics reported that July’s job growth came in below expectations, with employment gains of 114,000. The unemployment rate also ticked up by 20 basis points to 4.3%, triggering worries that the economy was showing signs of slipping into a recession. Initial jobless claims the following week were stronger than expected, declining to 232,000, signaling that despite the prior week’s unemployment-rate increase, the labor market was still relatively healthy. Despite the spike in volatility along with renewed worries of a recession, the real estate market ironically appeared to benefit from the confusion.

One result of the market turmoil is that the magnitude of future interest rate reductions is poised to be larger than previously anticipated. For example, the Mortgage Bankers Association (MBA) reported that the 30-year fixed mortgage rate for conforming loan balances ($766,550 or less) declined to 6.46% by Aug. 26, the lowest level since May 2023. Also given the falling mortgage rates, refinancing activity spiked in the week ending Aug. 9 by 35% week over week and 118% year over year, according to the MBA.

Even with increased activity, refinancing remained at historically low levels because nearly 90% of mortgage holders have home-loan interest rates below 6%. So, it’s going to take a very large rate drop to have a profound impact on housing. Most economists are expecting the Federal Reserve to cut interest rates at least twice by the end this year if inflation continues to moderate. Moody’s is forecasting that the rate cuts will result in the 30-year mortgage rate declining but that it will remain above 6% through the end of 2024.

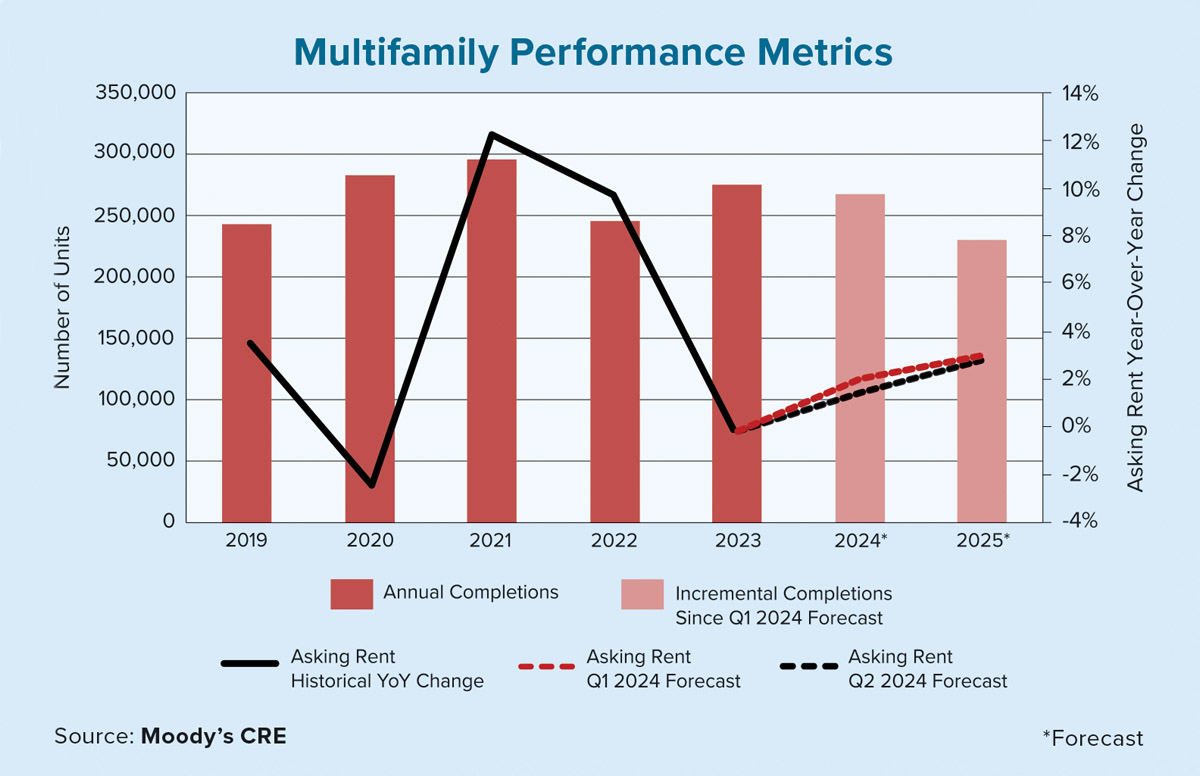

While even moderately lower mortgage rates should help slow rising housing prices, supply remains an ongoing problem. Moody’s Analytics estimated America’s housing shortage to be at least 1.9 million homes as of May 2024. The housing sector experienced years of underbuilding, which helped create the shortage. Ongoing challenges such as higher labor and raw material costs, exclusionary zoning policies and a lack of qualified construction workers are all contributing to slow new homebuilding. Thus, lower interest rates are not a panacea for housing affordability relief. Ultimately new construction needs to help fill that gap. The good news is that single-family and multifamily completions will be strong for the second year in a row. The projected completion of nearly 267,000 multifamily units in 2024 is likely to be revised upward to nearly 300,000 later this year, and is expected to cut rent growth to the low- to mid-1% range.

Lower interest rates will not only help home refinancing activity pick up, but also provide a more attractive entry point for those potential homebuyers and sellers looking to move. As affordability begins improving, more first-time homebuyers that are currently renting will have a better chance at building home equity. This trend also should help ease demand in the multifamily market and keep rent growth in check. This dynamic is already playing out as some landlords attempt to preserve occupancy by offering concessions, such as free or reduced rents over a certain portion of the lease’s term. In fact, according to Moody’s second quarter 2024 data, the average gap between asking rents (the price advertised by landlords) and effective rents (the adjusted price with discounts and incentives) remained above $90 for the third straight quarter, indicating the highest level of concessions in our tracking history going back to 1999. This means that effective rents imply a discount of approximately 5%. In short, despite all the negative headlines that came out of August, the real estate market may be primed to turn the corner.