Like other commercial real estate sectors, the financial well-being of U.S. consumers remains an important driver affecting retail property performance. Despite calls that a recession was imminent in the second half of 2022, those predictions have not yet come to pass due to a more resilient-than-expected American consumer. The spending by consumers accounts for about 68% of the nation’s roughly $28.6 trillion in gross domestic product. So, the financial well-being of consumers drives sales of brick-and-mortar retail establishments and the broader economy.

It’s been interesting to see just how resilient consumers have been, especially in the face of higher borrowing costs and inflation. It is true that inflation has come down from its peak of 9.1% in June 2022, to about 2.5% in August of this year – as measured by the Consumer Price Index. Interest rates, however, have remained in restrictive territory, despite the Federal Reserve’s 50 basis-point cut of its benchmark fund rate in September and further rate cuts likely on the horizon.

While disinflationary progress continues to work its way through the system, grocery prices, for example, are still elevated relative to the start of the pandemic. Food prices are not rising as fast as they were, but consumers continue to feel inflation’s lingering sting.

In particular, higher rates and inflation have disproportionately affected lower-income households as more affluent families have been better insulated due to earning higher real wages. More affluent families also enjoy an increased likelihood of accruing positive wealth effects from investing in the stock market or through homeownership. Nonetheless, aggregate measures of consumer expenditures continue to signal robust spending patterns. As long as the labor market remains healthy, the U.S. economy should be able to keep chugging along.

Given this backdrop, it shouldn’t be surprising that the retail sector’s neighborhood centers, which are smaller retail properties that are usually anchored by a supermarket; and the larger community shopping centers, which feature a wider range of apparel and other soft goods; have remained relatively stable over the past several years.

For example, Moody’s CRE data indicates that the vacancy rate for these centers is about 10.4%, and has only cumulatively increased by 20 basis points since its year-end 2019 level. This analysis doesn’t include malls, which have experienced more pressure in recent years.

In a similar vein, the retail sector’s regional performance has also varied, but within a narrow range. By using effective revenue (the occupancy rate multiplied by effective rents) to quantify the financial health of a property, we found that on a per-square-foot basis through June 30 of this year, the effective revenue rate grew by an average 48 basis points across the country. It varied, however, from the Northeast, which was up 57 basis points, to the Midwest, which saw the nation’s slowest growth at 15 basis points. The three metropolitan areas that saw effective revenue rise the most over the first half of the year were Hartford, Connecticut; Colorado Springs; and Cleveland. All three reported effective revenue growth of about 1.7%. While some locations dipped into negative territory during this period, results show that effective revenue performance grew in a relatively narrow band across most markets.

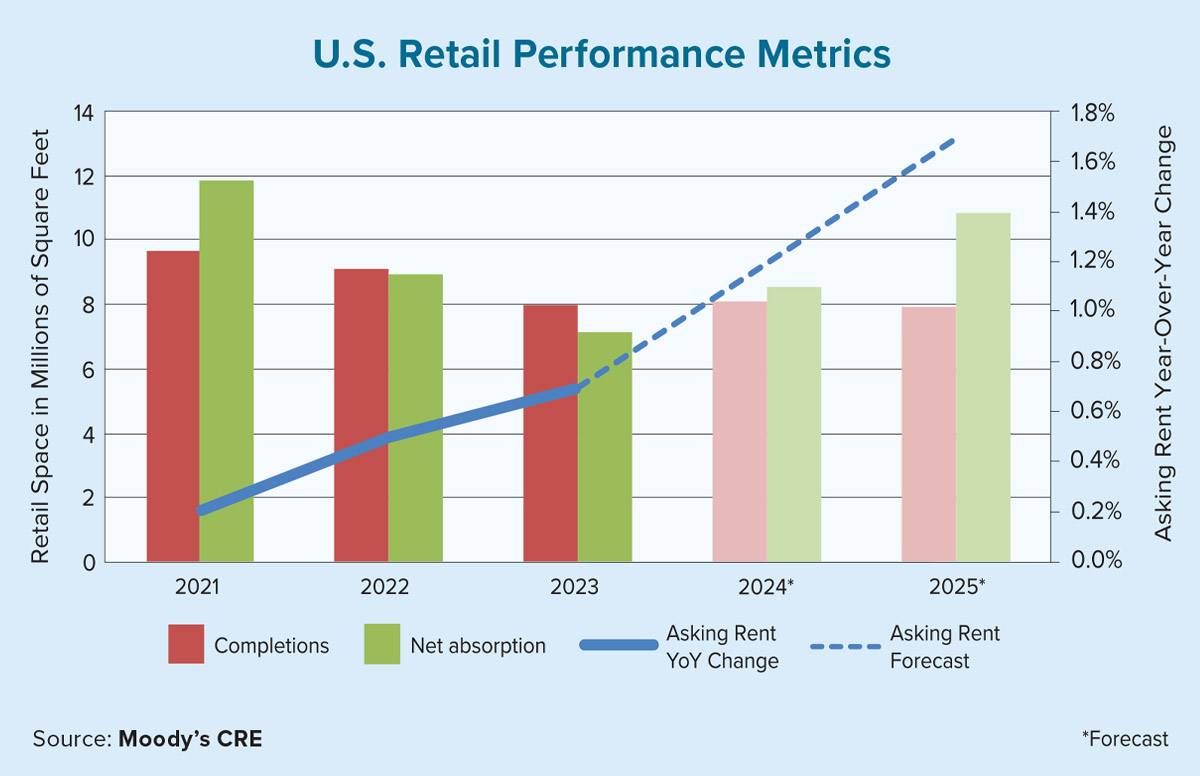

Looking forward, the Fed’s plan to gradually lower its benchmark rate should help the American consumer to propel the economy forward over the near term, despite various challenges, including rising credit card debt balances and an uptick in delinquency rates. After a nationwide excess in retail space in 2023, in which completions outpaced net absorptions, we expect this trend to reverse itself over the next two years, with asking rent growth projected to increase from the low-1% area in 2024 to the mid- to high-1% range in 2025.