Retail real estate has seemingly been in a state of flux since its origins. Main Street gave way to the strip center, which turned into the indoor mall and eventually pivoted to the power center. Over the past 20 years, the rise of e-commerce placed the entire bricks-and-mortar retail industry into question as words such as “apocalypse” were pondered regularly.

And while nothing close to an apocalypse has occurred, retail did take another turn in its long journey. Staples of 20th-century shopping such as Sears and Bed, Bath & Beyond have largely shuttered their doors. Others, like JCPenney, are doing whatever they can to stay afloat. Many malls have permanently closed, with others on the chopping block. And even some power centers and neighborhood centers have either closed or sit half empty.

When we look at the long-term national-level performance and development data, it is hard to find many bright spots. Construction of retail property has been anemic, with less than 100 million square feet of space added over the past decade, or less than 5% of total U.S. inventory, Moody’s Analytics found. For context, office-sector inventory grew by about 10% during the same period. As for rent growth, retail assets have fallen well short of inflation, even prior to the recent run-up in consumer prices.

But all of that is in the past, and while the retail sector will continue to see changes, we do see a new equilibrium on the horizon. The industry has somewhat rightsized itself, finding ways to appeal to consumers who desire the more social aspects of shopping and entertainment while also providing “showrooms” and customized spaces to enhance the online experience.

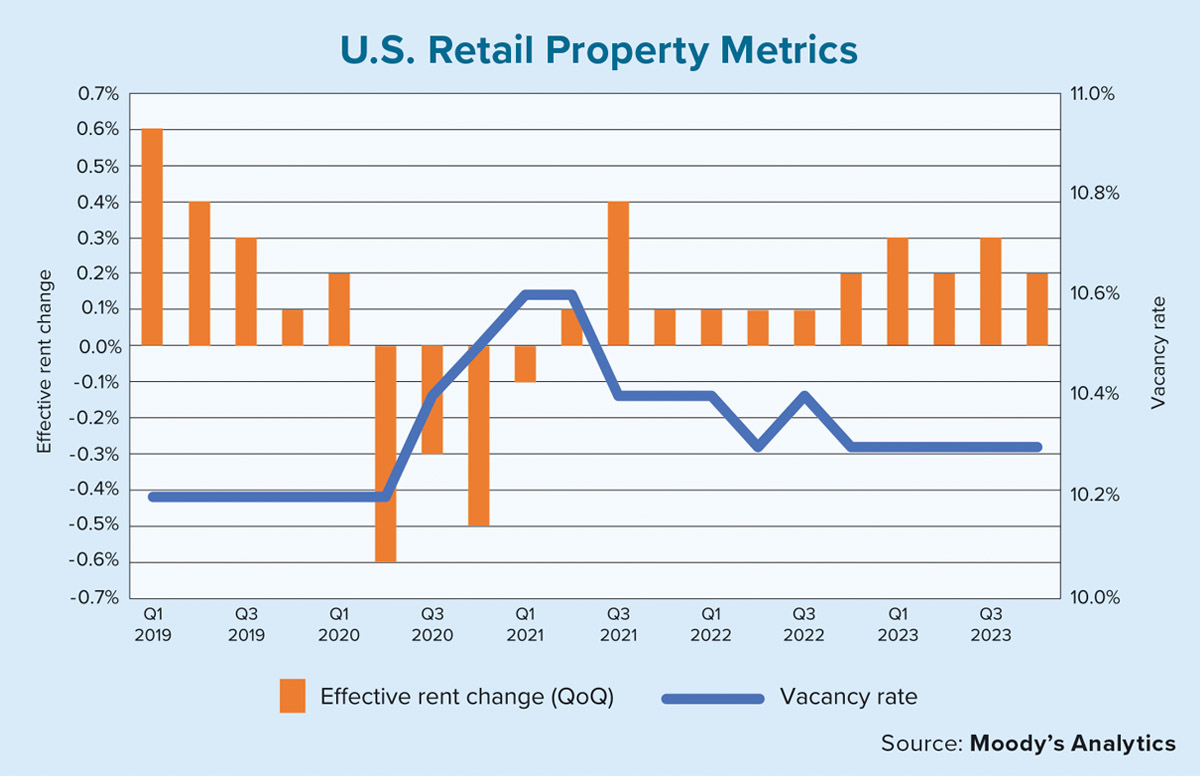

How have the performance metrics fared recently? As the accompanying chart illustrates, the U.S. retail vacancy rate has stabilized at a shade over 10%, while effective rent growth has picked up. This data shows that the sector still has plenty of room for further growth, but the aggregate statistics also mask some interesting pockets of positive activity.

One of the most startling statistics is rent by vintage. In the majority of metros around the country, there is a rent premium of 50% to 100% for properties built in the past decade — and recent rent growth has followed suit. Metro-level differences are also noteworthy. The areas of the country that have not seen large population or income gains tend to have elevated vacancy rates, often due to the disproportionate amount of older properties that are tied to a lack of development funding.

Some of the clearest examples of this trend include Indianapolis; New Orleans; New Haven, Connecticut; and Syracuse, New York, each of which have retail vacancy rates of more than 15%. Creative, modern developments in these metros may have great potential given the older stock.

Where does this ever-evolving property type head from here? Well, e-commerce is likely to continue growing. The online share of all retail sales has been trending around 15% for a while, and Moody’s Analytics expects it to jump to 20% by the end of the decade. Along with continued shifts in population and consumer preferences, this will sustain some of the same nuances for sector.

The national-level metrics will stay similar to where they are now, while older inventory will make way for trendy developments that incorporate more of the experiential and omnichannel needs of modern society. As always with commercial real estate (and maybe most importantly with retail), a close inspection of the asset, the tenants and the location are vital for a successful investment endeavor. ●