It wasn’t too long ago that pundits were opining about whether the historically high inflation being observed in the U.S. economy was transitory. As everyone soon learned, inflation was not transitory and the Federal Reserve was behind the curve in taming it. Consider that the yearly growth in the Consumer Price Index was 8.5% in March 2022 — the same month that the central bank chose to raise benchmark interest rates by 25 basis points (bps) from near-zero levels.

Another 500 bps of rate hikes later, it’s fair to say that the Fed has been able to get a handle on inflation while the labor market has remained surprisingly resilient. This brief backdrop is important for understanding the highly rate-sensitive nature of the real estate industry.

With the 10-year Treasury yield hitting 4.98% in October 2023 — and the average 30-year fixed mortgage rate briefly topping 7.75% that same month — higher financing costs coupled with a scarcity of available housing inventory has led to a significant slowdown across the residential real estate sector. Additionally, after more than a decade of ultra-loose monetary policy, sellers don’t want to give up their low mortgage rates, which has only exacerbated the already adverse housing supply conditions.

Consequently, these factors have provided an uplift to the multifamily housing sector as potential buyers are priced out of the purchase market and funneled into the rental market. Unfortunately, this is a lose-lose scenario for many households. On one hand, a median-income household that made a 20% downpayment on a median-priced home in the U.S. in third-quarter 2023 had a mortgage-to-income ratio of 35%, according to Attom. On the other hand, Moody’s data found that the national median rent-to-income ratio of 30% was only slightly better at that time, illustrating how discretionary budgets are being constrained on both fronts.

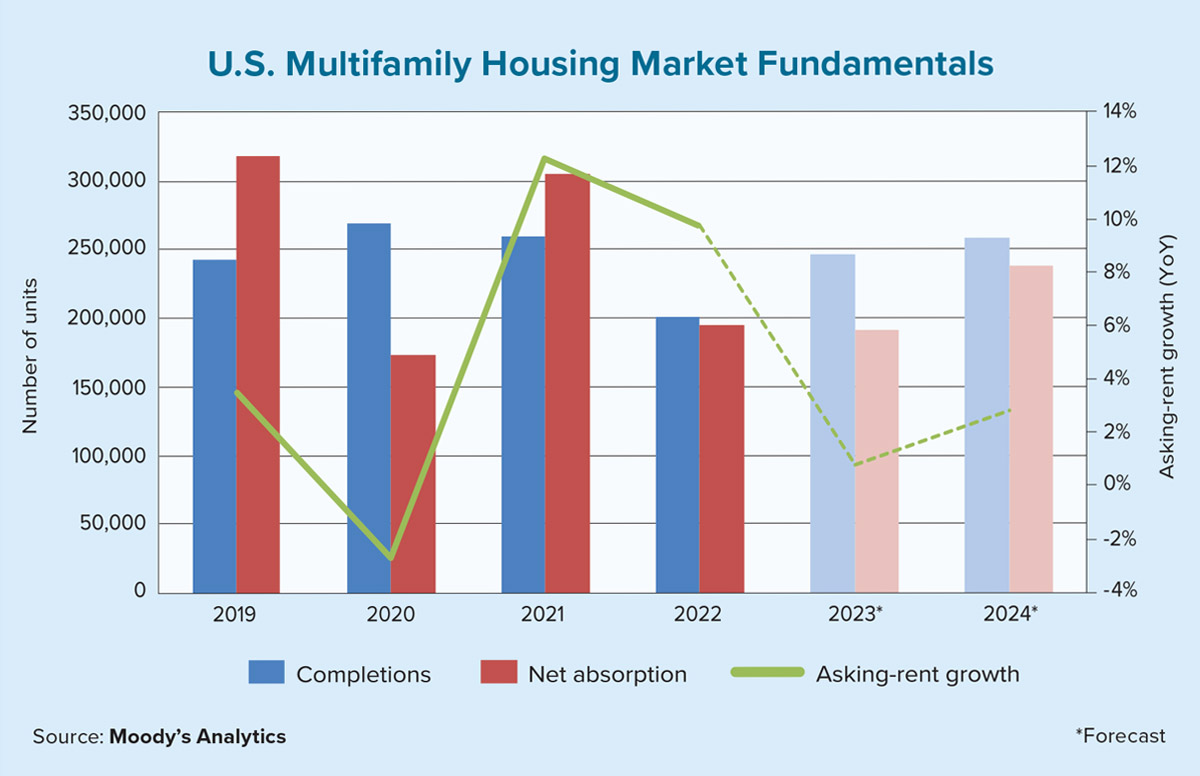

Renters can be thankful that multifamily supply conditions are not nearly as bad as they are in the owner-occupied market. For instance, as the chart on this page shows, Moody’s expects that 2023 will be a banner year for multifamily completions at nearly 250,000 units, which will help to keep annualized growth for asking rents from exceeding 1%.

Strong capital flows into the multifamily sector are a good omen for those stuck waiting in the rental market as the incremental supply created by developers eventually tends to place downward pressure on rents. In summation, while many potential homebuyers may be unhappy with their current living arrangements, it would behoove them to remain patient and continue saving for a larger downpayment. They’ll be better positioned to capitalize when the right homeownership opportunity presents itself. ●