The U.S. self-storage sector is notorious for its cyclicality — busy in the warmer months and bookended by quieter (and colder) first and fourth quarters. This follows patterns related to when households traditionally move, primarily in the spring and summer months that coincide with the academic calendar.

Domestic migration, however, was upended in early 2020 when workers and students abruptly went to fully remote status. Coupled with an inability to spend money on recreational activities due to pandemic-induced lockdowns and social distancing, this meant people spent their excess personal savings and stimulus payments on goods instead.

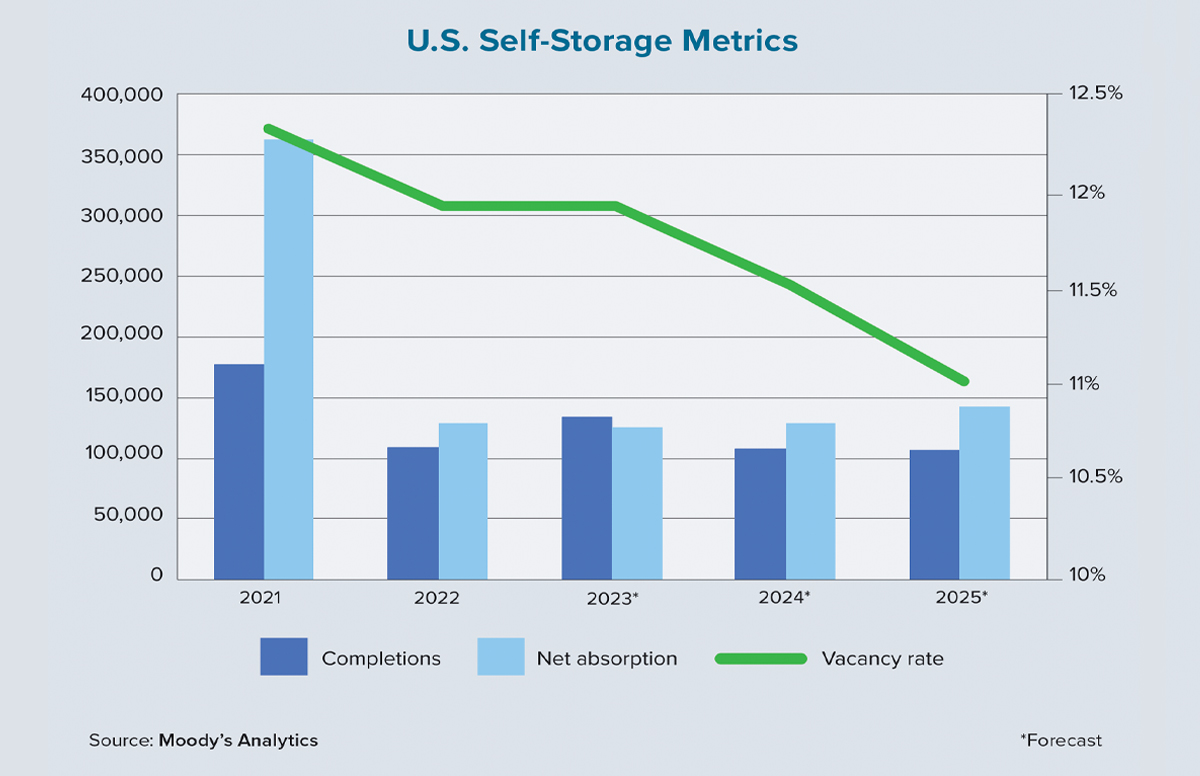

Between more flexible moving seasons and the accumulation of items that might not have otherwise been purchased, households began to scoop up self-storage space in record numbers. The sector shined as a result. Nationwide absorption peaked at just shy of 200,000 units in second-quarter 2021, as did annualized asking rent growth for 10×10 climate-controlled units (4.9%) and non-climate-controlled units of the same size (3.9%).

Today, however, self storage (like so many other pandemic-era superstar property types) is returning to earth. Slower growth and declines are happening across the country, which indicate that consumer spending patterns have shifted away from goods and back to services and entertainment. High inflation also cut into excess household savings, causing consumers to tighten the purse strings on discretionary purchases. This includes self-storage units that they may no longer want or need.

This confluence of factors is directly affecting performance metrics in the self-storage sector. The magnitude and direction of expected outcomes — patterns that have held relatively steady over the history of Moody’s data series — have shifted as the sector deals with new supply-and-demand expectations and moves toward a new state of stability.

For example, from 2012 to 2022, completions during the second quarter of the year averaged about 47,500 units. In second-quarter 2023, however, completions dipped to approximately 12,600 units. The same pattern held true in Q4 2022 and Q1 2023. In addition to demand-side headwinds that suppressed developer appetite for bringing new product to market, new supply has also been constrained over the past two years by surging costs for land and raw materials, as well as a tight labor market and higher project financing costs.

Although it’s partially unintentional, the sharp decline in the delivery of new supply has proven beneficial for sustained performance metrics, despite the slowing demand across the sector. Net absorption, while still positive in Q2 2023 at about 46,000 units, finished well below the long-term second-quarter average of approximately 159,000 units.

But an opposing trend occurred in Q1 2023. With 64,000 units leased during the three-month period, demand was 60% higher than the long-run first-quarter average of 40,000 units leased from 2012 to 2022. And while absorption was negative in Q4 2022, which was consistent with historical trends, the amount of space shed (107,000 units) far exceeded the average amount of space shed during the fourth quarter of previous years (38,500 units).

So, is the self-storage sector’s traditional seasonality coming to an end? Not quite. While there is a major recalibration underway for owners and operators in their ability to easily predict the magnitude and directionality of key performance metrics (including rents and vacancies), it is temporary.

It also appears that, especially on the demand side, unexpected weakness in some quarters is being supplanted — at least in part — by unexpected strength in other quarters. The drastic and unexpected external shocks that led to stratospheric growth in this sector have receded. Self storage is on a path to a new equilibrium and is poised for stabilization in the coming years. ●