The U.S. hotel sector has been on a roller-coaster ride for the past three years. After fears of Armageddon became paramount for much of 2020, COVID-19 vaccines and pent-up demand quickly brought the phrase “revenge travel” into our lexicon as people sought experiences they missed during the early stages of the pandemic.

Hotel occupancy rates rebounded and average daily room rates soared as households looked to spread their wings and spend their excess savings. But as we know too well, nothing lasts forever. Stimulus funds have dried up, home price appreciation is stagnant or declining, and equities are currently on their own bumpy ride. And while a national recession is far from guaranteed at this point, an economic softening is upon us.

The overall labor market will remain relatively tight over the next couple of years, given an imbalance in skill and a general shortage of workers, but companies have already been conducting layoffs, particularly in middle-management positions. Elevated uncertainty for these middle-class workers will surely dampen their plans for lavish travel this summer.

This is not to say that the bottom is about to fall out for the hospitality sector, but the reaction of hotel performance metrics to lower leisure demand will be an intriguing summer story. To gauge the impact of economic changes upon the hotel industry, let’s sift through some of the most relevant demand drivers.

Positives: Excess savings is declining but still in the black. As of February 2023, excess savings (or the extra money consumers saved beyond the level they would have without the pandemic) was approximately $1.5 trillion. This is well below the September 2021 peak of $2.5 trillion but is nothing to scoff at. Some cushion remains for those who have lost jobs, or fear a job loss, but these funds will most likely be saved or used for necessities.

Negatives: Retail sales growth has weakened over the past year. March 2023 spending levels were roughly level with their October 2022 reading. Service-sector performance is still outpacing that of goods, but consumers have been tightening their purse strings across the board. In fact, with annualized inflation still running well above normal, spending levels declined throughout much of the winter and spring. It’s likely that this will turn around a bit as lagging tax returns make it into consumers’ hands, but as previously mentioned, fear and uncertainty tend to lead to more conservative spending habits.

Neutrals: The labor market is softening — and will soften further — but it won’t fall off a cliff. This is not the same situation as the Great Recession and its 10% unemployment rates, but rates of 5% to 6% by this time next year are not out of the question. What is a wild card here (and what may keep unemployment down and wage growth positive) is a high ratio of job openings to unemployed persons. Entering the two other recessionary periods of this millennium, this ratio was considerably below 1.0. As of this past February, the ratio was falling but still above 1.5.

Neutral but leaning positive: Corporate and event travel is not part of the “revenge” definition, but it is still quite important to the health of hotels. Placer Labs recently utilized cell phone data to track visits and usage for a variety of locations and transit types. Using measurements such as the timing and frequency of air travel, as well as visits to convention centers, they concluded that business travel is seeing a resurgence but has yet to return to pre-pandemic levels. Will this type of travel fully return? It may not happen in the exact same fashion, but a full recovery is possible in the next few years with a realization that education, networking and sales are more effective in person.

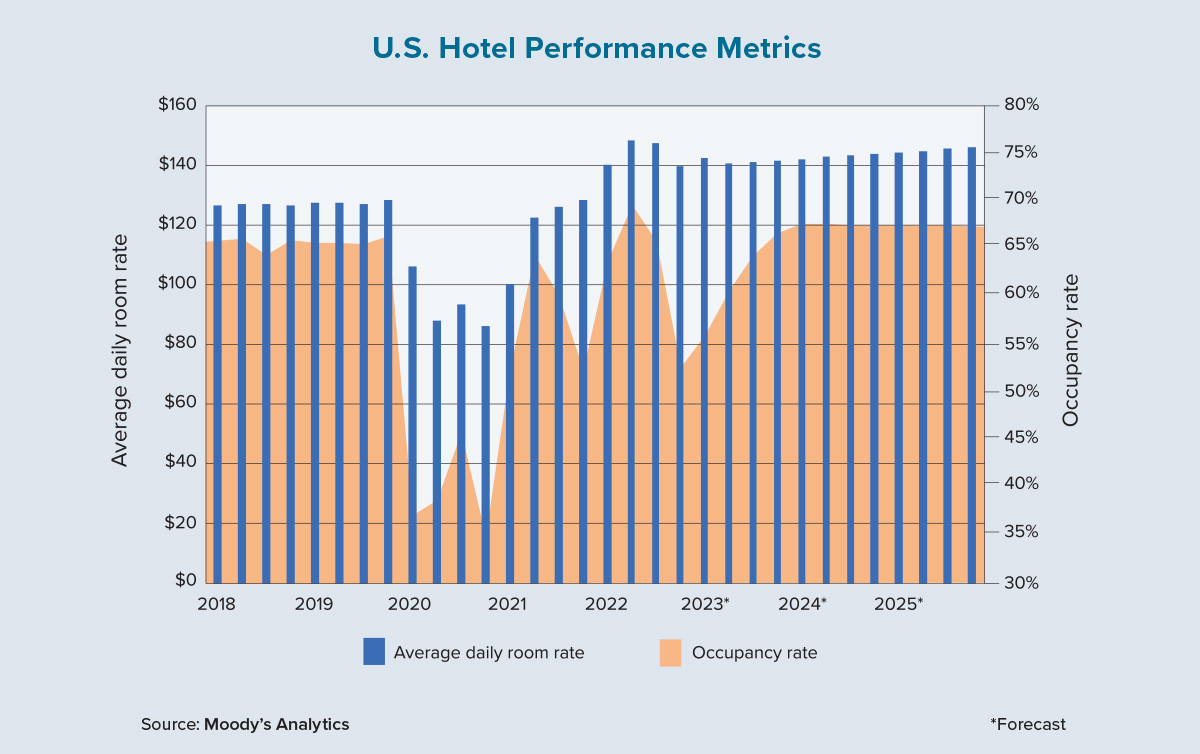

As the chart on this page illustrates, the hotel-sector roller coaster is forecast to come to an end, with occupancy and room rates above pre-pandemic levels. A continued resurgence of business and event travel, along with a resilient labor market, will outweigh a pullback in revenge travel. ●