Senior housing facilities primarily exist to provide shelter for a portion of the elderly population. This sector of commercial real estate is commonly divided into four types: assisted living, independent living, memory care and skilled nursing facilities.

The COVID-19 pandemic hit this sector disproportionately hard due to the initial lack of preventive health measures, the severity of infections and persistent staffing shortages. The sectorwide vacancy rate jumped from 10% in 2019 to 17% in early 2021 before vaccines became widely available among residents and staff. But as COVID concerns gradually faded, other emerging macroeconomic factors (geopolitical conflicts, persistent labor shortages, and higher costs for labor and building materials) continued to shake up the sector’s fundamentals.

Moody’s data shows that senior housing construction deliveries in 2021 were down to less than 60% of their pre-pandemic average while starts fell to a five-year low. Last year, as the cost of capital shot up and credit availability tightened, deliveries were only 10% of their 2021 level. While senior housing construction activity slowed, demand rose steadily as confidence in the safety of these facilities gradually returned amid robust need from the U.S. senior population.

Census data shows that the number of Americans who are 65 or older reached 55.8 million — or 16.8% of the nation’s population — in 2020. The rapid growth of this demographic since 2010 is being driven by aging baby boomers, who began turning 65 in 2011. This combination of persistent demand and reduced supply growth caused the senior housing vacancy rate to decline for eight straight quarters, by a total of 390 basis points (bps), to reach 13.2% in Q1 2023.

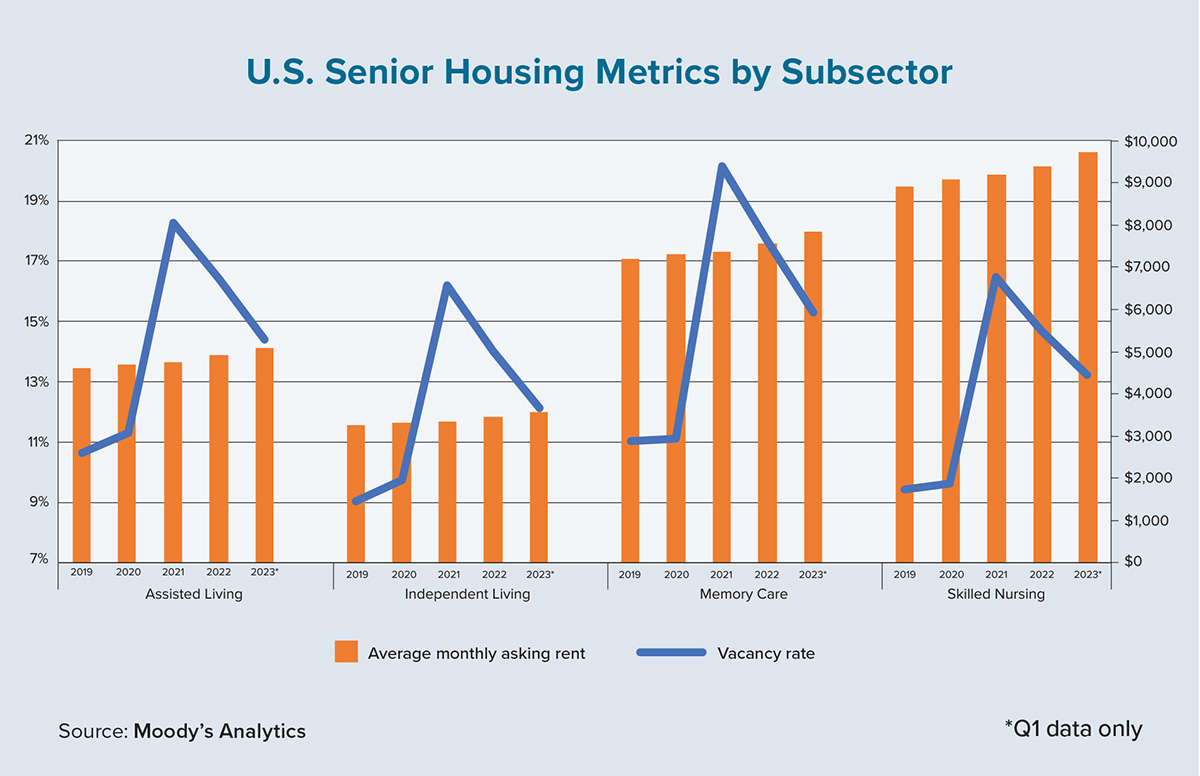

Across the four senior housing types, memory care facilities were under the most pressure during the pandemic due to their need for specialized living designs and trained staff members. Memory care lagged the other three subsectors with the highest level and steepest increase of vacancy rate during the pandemic era. At the other end of the spectrum, independent living facilities — which are the most affordable of the senior housing types — have been the most resilient.

Need-based demand and weak construction activity have continued to cause excessive supply to be absorbed. Across the board, vacancy rates dropped during the year ending this past March, led by memory care (-240 bps) and assisted living facilities (-200 bps). Independent living (-190 bps) and skilled nursing facilities (-150 bps) weren’t far behind.

The senior housing sector usually registers its largest rent increases in the first quarter, when repricing occurs as regulatory and budgetary considerations take effect. In Q1 2023, rents for the four subsectors jumped by 3.5% to 3.7%, the highest annualized growth in Moody’s 10-year tracking history. Strong demand tightened market conditions and justified rapid rent growth.

Moreover, rising inflation and elevated interest rates have forced the adjustment of rent to account for higher operational and capital expenses. Over the past four years, rents for assisted living and independent living units have grown the most due to their relatively lower rent levels. Cumulative rent growth has reached 10.5% for assisted living, 9.6% for independent living, and 9% for both memory care and skilled nursing facilities.

How long will the boom last? Although the answer may depend on the interplay of factors such as the cost of goods and services, the availability of mortgage credit and the supply of skilled labor, the need for senior community support services will continue to rise as baby boomers retire and age. The passage of the Inflation Reduction Act (which will lower medical expenses for senior citizens) is likely to produce some long-term benefit for the sector’s recovery.

Across various regions, Midwest and Northeast senior housing markets were hit hardest during the pandemic but have been leading the recovery up to present day. A full understanding of the senior population, especially at the local level, will be critical for investors to turn a profit during an approaching economic downturn. ●