Rents for U.S. apartments grew 3.7% year over year in 2019, according to data from Reis Inc. This figure was below the rent-growth rates of 5% in 2018 and 3.9% in 2017, and the decline is reflected by a drop in completions compared to prior years. New construction disproportionately impacts rent growth as these properties tend to have higher average rents.

Multifamily completions are expected to increase in 2020, which should prompt rent growth to accelerate a bit. But a projected rise in rents begs the perennial question: Is it cheaper to rent or buy a home?

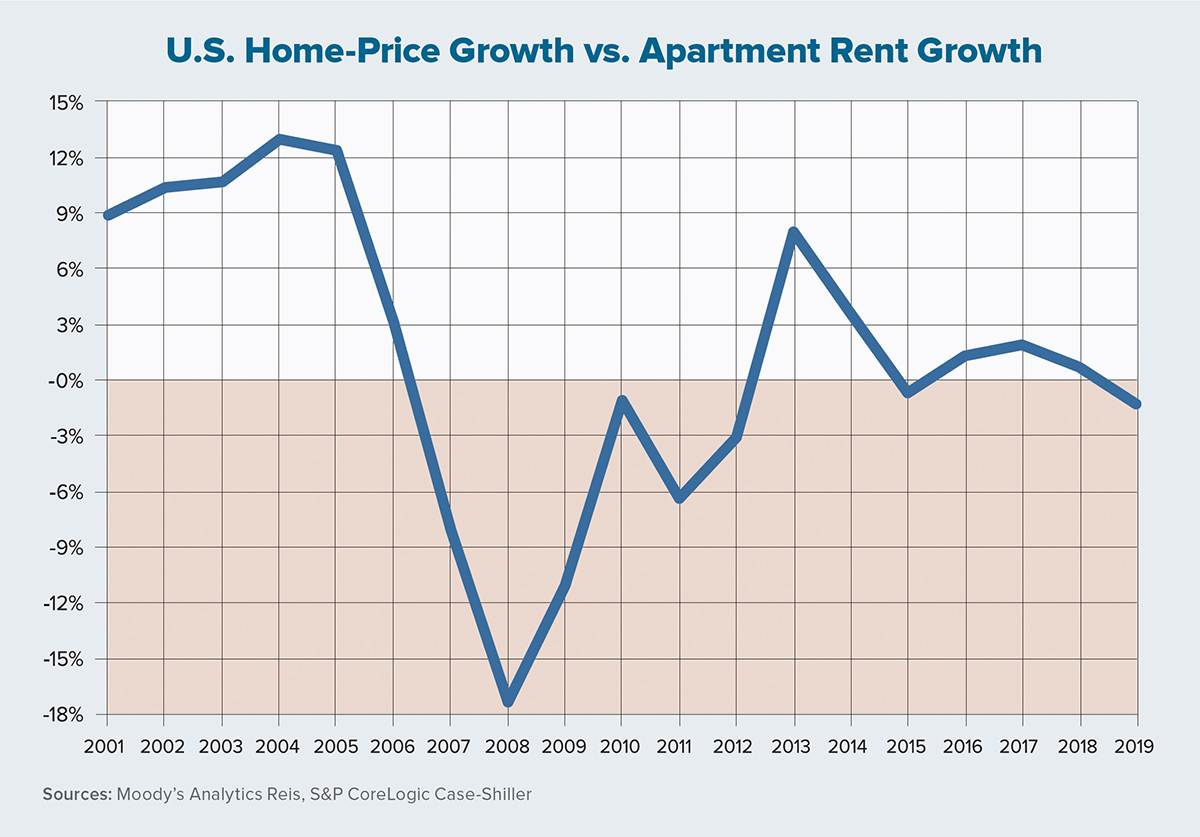

Rents grew at a stronger rate than home prices last year in the majority of U.S. metro areas. Although the Federal Housing Finance Agency’s house-price index climbed 4.9% year over year this past November, the S&P CoreLogic Case-Shiller 20-city composite index rose by only 2.6% that month.

The Case-Shiller index is more comparable to Reis’ apartment rent data, because even though the Reis data includes 79 metros, the average is heavily weighted by the top 20 metros that account for 58% of the national occupancy rate. In fact, the weighted average rent growth of the equivalent 20 metros included in the Case-Shiller index was 3.9% in 2019, only 20 basis points higher than the U.S. growth rate tracked by Reis.

The chart on this page shows how the two data series have fared since 2001. When the line falls below 0%, annual rent growth exceeds home-price growth, while the reverse is true when the line is above 0%. Since 2015, following a long period of housing booms, busts and rebounds, the two trend lines have moved nearly in step with each other — which is rather remarkable given the history of the two markets.

Of course, not every metro has seen the same smooth pattern that started in 2015, although most were relatively flat from 2015 to 2019 compared to prior years. Last year, in fact, only three metros had home-price growth that outpaced rent growth. In Las Vegas, the Case-Shiller home-price index climbed 5.6% compared to rent growth of 4.2%. In Tampa-St. Petersburg, Florida, home prices climbed 4.9%, just ahead of 4.7% rent growth. In Detroit, home-price growth of 3.7% exceeded rent growth of 3%.

Metros that saw the highest gap between rent growth and home-price growth were Seattle, San Francisco, New York City and Chicago.

Phoenix (at 6.5%) had the highest rent growth of the metros included in the Case-Shiller index, followed by Charlotte and Chicago, which each saw rent growth of 5.4%. Not surprisingly, Phoenix (6.1%) and Charlotte (4.5%) had two of the highest home-price growth rates. Chicago, meanwhile, saw its condo and home-price indices grow by 1.1% and 1.3%, respectively.

It is worth noting that most of the metros listed above had strong job growth of 1.9% or more in 2019, above the U.S. average of 1.6%. (The exceptions were Chicago and Detroit, with job growth of 1.1% and 0.3%, respectively.) Notably, Dallas had the highest job growth (3.6%) among the 82 metros tracked, yet its rent growth and home-price growth was only 4.3% and 2.9%, respectively.

Fluctuations in rent growth and home-price growth are driven by changes in supply growth versus demand growth. For many metros, supply growth has impacted prices as much — or more — than demand, which has held steady over the past 11 years and was nearly in step with job growth. With healthy supply and occupancy growth forecast for the apartment market, rents should continue to grow at a similar rate as the past few years.

Other factors, including mortgage rates, mortgage interest tax deductibility and the likelihood of people listing their home on the market, has and will continue to impact the home-purchase market. These factors should not change dramatically in 2020, meaning the apartment and owner-occupied housing markets should continue to move in unison.