Despite the Federal Reserve’s efforts to quell inflation by raising interest rates an incremental 100-basis points in 2023 (after increasing by 425-basis points in 2022), the economy has performed surprisingly well, avoiding the recession many forecasters had predicted.

In light of the inflation rate moving closer to the Fed’s 2% target, the Federal Open Market Committee announced it would consider three 25-basis points interest rate cuts this year. Those cuts couldn’t come soon enough for the troubled office sector. The lingering high interest rates coupled with the pandemic-exacerbated changes in office use have negatively impacted the sector more than any other in commercial real estate.

Since 1979, the long-term average office vacancy rate for the nation’s top 50 metro areas was slightly above 15%. The vacancy rate over the past four years, however, was roughly 340 basis points higher. In the fourth quarter of 2023, the rate hit an all-time high of 19.6%, surpassing the previous vacancy record of 19.3% set in both 1986 and 1991 during the savings-and-loan crisis.

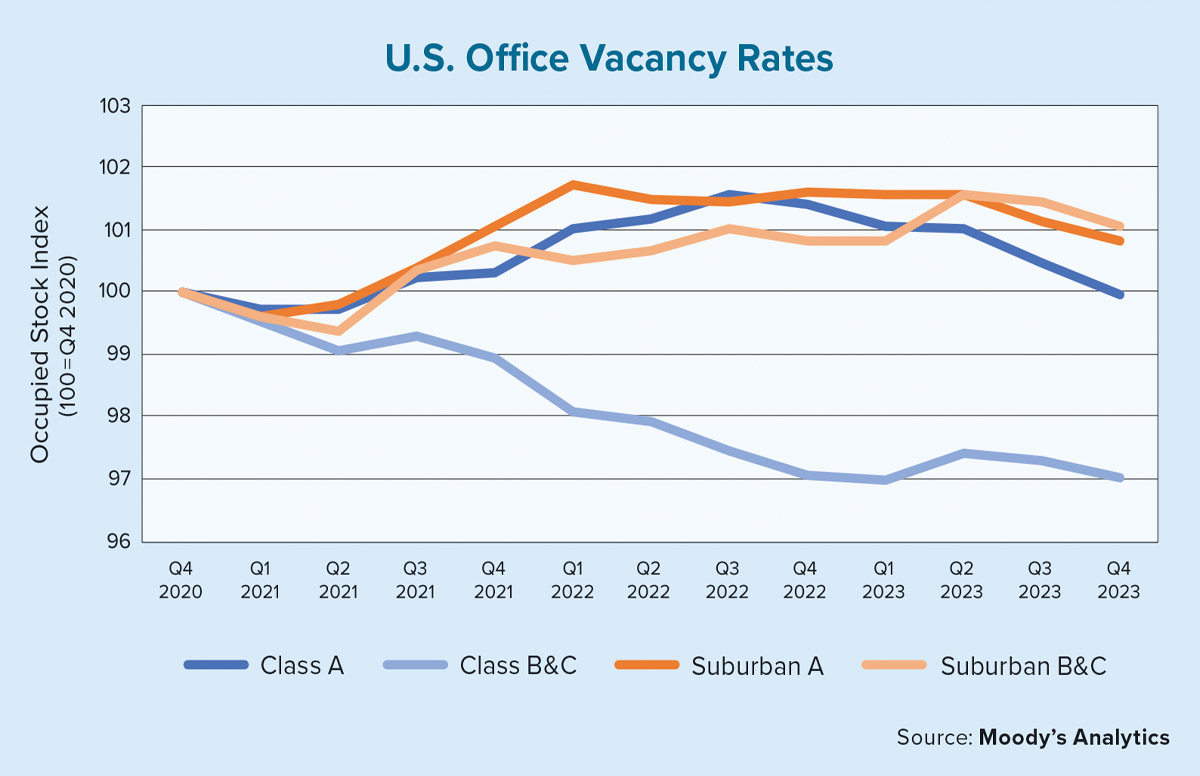

It is also instructive to see how these properties have performed based on whether they are located in downtown or suburban locations. The accompanying chart plots the stock indexes — the square feet of office space being occupied by tenants — for class A, a higher-quality classification, and B and C office properties, with lower-quality classifications. The chart plots indexes for central business districts and suburban locations. Each segment’s time series was then benchmarked to the fourth quarter of 2020 and set at 100.

The major finding is that class B and C offices in these business districts have exhibited a clear downtrend over the past three years. This segment’s occupied stock index decreased by a cumulative 3% over the period. Class B and C offices are typically older buildings that require higher capital expenditures to update the properties. The other finding is that class A offices in central business districts generally benefited from landlords and tenants seeking higher quality assets. This continued until about the end of 2022. Since then, the occupancy gains have been erased and as of year-end 2023, the index was essentially at parity with Q4 2020 levels.

Moving to suburban offices, class A properties have outperformed their class B and C counterparts through the first quarter of 2023. Although, since then, the tables have turned, and class B and C offices have fared marginally better. As companies continue to embrace remote work, lower-cost leases in the suburbs have become increasingly viable options. For example, trading down from class A to class B or C suburban office space results in a 31% reduction in asking rents per square foot as of the fourth quarter of 2023. Transitioning from class B and C offices in a central business district to a similar classified office building in the suburbs would result in an even greater cost reduction of nearly 35%.

These are national figures, so regional differences would alter the estimates. Nonetheless, given how office leases typically last between five to 12 years (and even beyond 20 years), it could take several years before a company is able to accrue any benefits related to a change in its real estate strategy.

As the office sector continues to evolve around how people live, work and play, road bumps are to be expected, but there are also opportunities for those who understand the nuances. Only time will tell when the office sector settles down. For now, it appears 2024 may be another turbulent year. ●