Even before a federal appeals court issued its Aug. 15 decision allowing the Trump administration to proceed with mass layoffs at the Consumer Financial Protection Bureau (CFPB), mortgage attorneys were reading the writing on the wall.

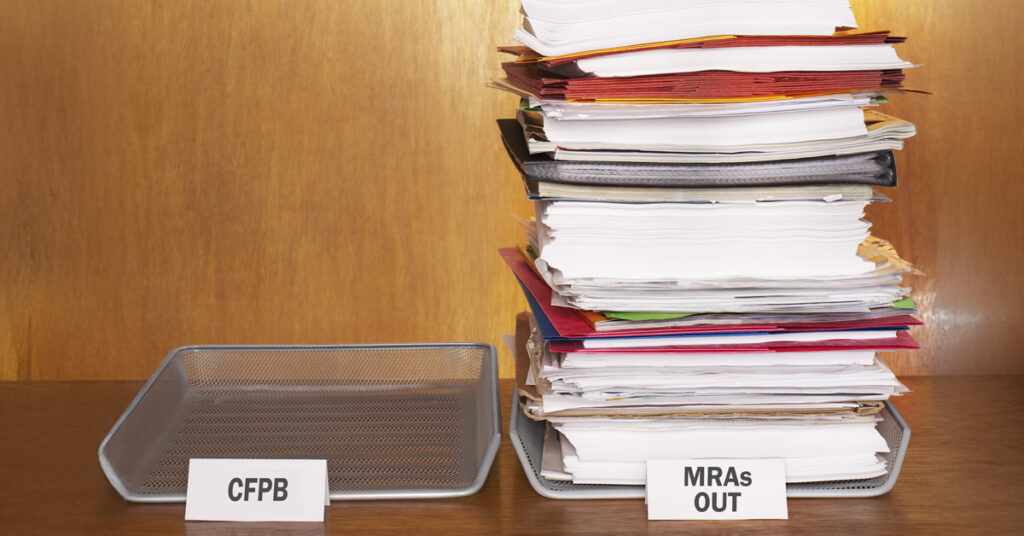

In the wake of recent Bloomberg reporting that the CFPB could close “as many as 99%” of all outstanding “matters requiring attention” (MRAs) by the end of this week, experts within the mortgage industry spoke with Scotsman Guide to shed light on that process.

“If you’re going to cut the workforce down by 90%, you’re going to have 10% of the people working there,” says Mitchel Kider, managing partner of law firm Weiner Brodsky Kider. He has represented companies that have had their MRAs cleared by the CFPB within the past month. “There’s not going to be anyone there to follow up on these MRAs.”

MRAs function as a tool for resolving compliance problems through the CFPB’s examination process, allowing mortgage companies — and other financial institutions under the CFPB’s jurisdiction — to confidentially address issues before public enforcement is necessary. State regulators issue MRAs as well.

The clearing of MRAs at the federal level, warranted or otherwise, should not lead mortgage companies to think regulations are any less enforceable, says David Cotney, senior adviser with FS Vector, a financial services consulting firm. Cotney spent 26 years as a financial regulator with the Massachusetts Division of Banks, including as commissioner of banks from 2010 to 2016.

“I don’t think that most institutions out there are taking it that way. They’ve been complying,” Cotney says. “From a supervisory standpoint, the laws are on the books, and as anyone who’s been around for a while knows, there is a dreaded word. It’s called ‘lookback,’” he says, referring to the capacity for future CFPB leadership to hold companies accountable for past compliance failures.

MRAs are ubiquitous and are issued for infractions as innocuous as outdated policies and procedures and as egregious as predatory lending and fraud. Under the Biden-era leadership of Director Rohit Chopra, the bureau was criticized for overissuance of MRAs for matters perceived to exceed its supervisory purview outlined in the Dodd-Frank Act.

As a 44-year mortgage industry veteran, Kider says “the vast majority of MRAs are those innocuous matters, like failure to document properly or complete your QC review properly.” Yet, the opacity of the CFPB’s examination process and the speed with which the bureau has moved to clear its outstanding MRAs raises questions of due diligence.

“Some egregious issues may get swept up in that effort, obviously, if it’s a large effort,” Kider continues. “I don’t think every egregious issue will get swept up in that effort. I do believe that someone is looking at these particular cases and making a determination as to whether or not they believe it’s egregious. They haven’t dropped everything.”

The CFPB did not respond to Scotsman Guide’s request for comment.

Still, the message the CFPB has sent to the mortgage industry is clear, says Daniella Casseres, partner and head of the mortgage regulatory practice group at Mitchell Sandler.

“The message is about priorities, and it’s clear to all the mortgage lenders what the playing field is, which is less enforcement and fewer examinations,” she believes, calling the wholesale clearing of MRAs “a positive thing for mortgage companies when it comes to being examined by the next administration.”

At mortgage companies where robust compliance is a feature and not a bug, “the playing field is what it’s always been,” Casseres continues. “For others, the impression is that they can take their chances on things they may have received MRAs for in the past.”

Nevertheless, even the cleared MRAs will provide a blueprint for future examinations should future leadership at the bureau reconstitute a more robust supervisory function.

“Rohit Chopra was amazingly aggressive, so he was leaning on this supervision team to come up with more and more MRAs,” explains Mark McArdle, the assistant director of mortgage markets at the CFPB from July 2017 until last February. Before an MRA would be issued to a mortgage entity, for example, the supervision team would consult with McArdle’s team to understand the issue that had been flagged and its potential impacts.

Now serving as senior vice president of regulatory affairs and public policy for Newrez, one of the country’s largest lender-servicers, McArdle says Newrez is “one of those entities that had a number of MRAs” now being cleared by the CFPB. Following a period of “zero contact” after the 2024 presidential election, the bureau reached out within the past month to start clearing.

“There’s definitely a risk that more serious matters are dismissed, as well as the more trivial.”

Citing an Aug. 6 letter sent by 11 Republican senators to leadership at the Federal Reserve, the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corp., McArdle says the wholesale clearing of MRAs may serve a dual purpose. That letter called for change to an MRA process dubbed “increasingly opaque, ineffective and inconsistent.”

“They believe the MRA process was too aggressive and too loose,” McArdle explains. “I think that’s a widespread belief that often supervision entities cite things that aren’t really problems. The second thing is I do think they want to have a reduced footprint in the supervision team and to do that you need to close out all these exams.”

Ultimately, he says most mortgage companies do not rely on the CFPB or state regulators to identify problems within their lending operations or outcomes, due to the work of internal audit teams. Private rights of action also function as avenues to accountability.

“There’s definitely a risk that more serious matters are dismissed, as well as the more trivial, based on a lot of the MRAs I’ve seen,” McArdle believes. “I think for most companies, the message that you hear all the time is stay the course, keep your eye on the ball, keep compliance going because if anything, this regulatory environment is more chaotic.”

Not all mortgage companies have waited for the CFPB to make the first move on clearing MRAs, however. Attorneys representing mortgage companies in ongoing examinations have solicited the clearing of MRAs for their clients, capitalizing on the bureau’s reduced supervisory footprint. Casseres of Mitchell Sandler says she is proactively trying to get MRAs cleared for clients.

The clearing of MRAs and reduction in the CFPB’s supervisory functions may not directly translate to a reduction in mortgage lenders’ compliance burden, though. Kider of Weiner Brodsky Kider has not observed a cutback in compliance departments as state regulators become the stickier thorn in mortgage companies’ sides.

“Looking at how states are starting to step up in their enforcement,” Kider says, “I think in some ways compliance is going to be busier because instead of dealing with one federal regulator’s interpretations, now you’re dealing with 50 different states and different jurisdiction interpretations as well.”

In some regards, states have sharper teeth than the CFPB because they control mortgage licensing. Additionally, the clearing of MRAs by the CFPB does not prevent states from picking up the regulatory tab for targeting their exams and investigations.

“The closing out of an issue at the federal level may close it as far as the CFPB is concerned,” says Cotney, the former Massachusetts banking commissioner, “but if there are substantive issues that remain unresolved, there are actions that the states can take.”