Ten years have passed since the Consumer Financial Protection Bureau (CFPB) issued regulations to provide safer and more sustainable home loans for consumers. In January 2014, qualified mortgages became the standard by which lenders must abide.

The Dodd-Frank Act imposed an obligation on lenders to make a good-faith effort to determine that the applicants have the ability to repay the mortgage, currently known as the ability-to-repay (ATR) rule. The act also mandates that qualified mortgages cannot have risky loan features such as negative amortization, interest-only, balloon payments, terms beyond 30 years or excessive points and fees.

Furthermore, qualified mortgages must also satisfy at least one of three criteria. The borrower’s debt-to-income (DTI) ratio must 43% or less. The loan is eligible for purchase, guarantee or insurance through the federal government or a government-sponsored enterprise (GSE). The loan was originated by insured depositories with total assets less than $10 billion and must be held in portfolio for at least three years.

Any home loan that doesn’t comply with the QM rules is called non-qualified mortgage (non-QM). While non-QM loans are necessarily high risk, they still need to satisfy ability-to-repay requirements. Examples of a non-QM loan include interest-only or limited/alternative documentation loans.

Non-QM loans constitute a small portion of the current mortgage landscape, but they play a crucial role in serving borrowers who are unable to secure financing through GSEs or government channels. These loans provide a valuable option for creditworthy borrowers, including self-employed individuals, gig economy workers, first-time homebuyers, borrowers with significant assets but limited income, jumbo loan borrowers and investors.

Following the CFPB regulation, the non-QM share of total mortgage counts has been declining, hitting a low of less than 3% in 2020 The non-QM market has increased over the last couple of years, nearly doubling to about 5% of the market in the first half of 2024.

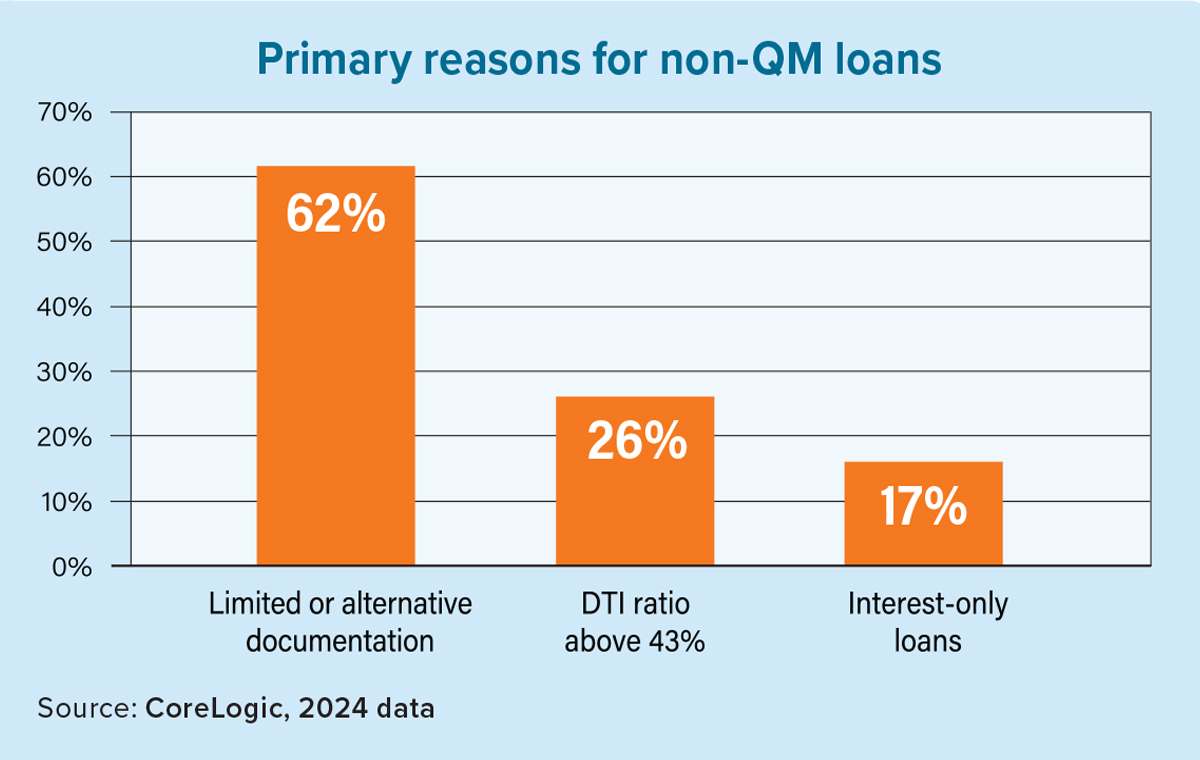

In addition, the composition of the risk indicators that characterize a non-QM loan has changed over time as well. Unlike in early 2000s when some of the loans had negative amortization or balloon payments, the main reasons non-QM loans did not meet QM standards in 2024 were the use of limited or alternative documentation (62%); DTI ratios for a mortgage above 43% (26%); and interest-only loans (17%).

The proportion of non-QM loans with DTI ratios exceeding 43% increased by 12 percentage points from 2020 to 2024. Conversely, the share of interest-only loans reduced by nearly half over the same period. Additionally, riskier factors such as negative amortization and balloon payments have been eliminated.

In addition to the risk factors that characterize non-QM loans, today’s non-QM loans are of higher quality than those originated prior to the Great Recession in terms of the key underwriting variables — credit score, DTI ratio and loan-to-value (LTV) ratio — for home purchase loans.

In 2024, the average credit score for non-QM borrowers was 776, compared to 781 for conventional QM borrowers and 699 for government loan borrowers. The average LTV ratio was 75% for both non-QM and QM borrowers, while government loan borrowers had an average LTV of 97%.

At 38%, the average DTI for non-QM is slightly higher than the 36% average for QM loans, but lower than the 45% average for the government loans.

And although the average DTI ratio for non-QM borrowers was higher than that for qualified mortgage borrowers, non-QMs are performing well. In fact, both non-QM and QM loans have historically low delinquency rates, significantly lower than those for government loans. For the loans originated in 2023, 4% of government loans were at some point 90-days delinquent while both QM and non-QM remained at the lowest levels since at least 2001, both at 0.3%. To offset the risk of default, lenders generally charge higher interest rates for non-QM loans; for example, the average initial 30-year interest rate for non-QM loans was 6.7% in 2024 compared to 6.4% for qualified mortgages. Lenders also are focusing on borrowers with higher credit scores and lower LTV ratios to balance the risks associated with high DTI ratios, limited documentation, and interest-only features of non-QM loans. Despite the inherent risk in non-QM loans, these loans have proven to be a valuable resource for creditworthy borrowers who do not qualify for traditional mortgage programs.