The United States is currently experiencing a well-documented housing affordability crisis. In addition to a significant shortage of existing single-family homes available for purchase, housing prices have increased by roughly 50% since the end of 2019, discouraging potential homebuyers.

Compounding the issue, despite a full percentage point reduction in the federal funds rate in 2024, mortgage rates have remained elevated with the 30-year fixed projected to remain above 6% in 2025. Having said that, today’s crisis has been exacerbated by years of insufficient housing construction following the global financial crisis, which has failed to keep pace with population growth.

While estimates of the housing shortfall vary, the lower end mark is believed to be at least 1 million homes. On a more positive note, 2024 marked a significant year for multifamily completions, at nearly 600,000 units. Although, recent declines in multifamily starts and permits data indicate that new supply is expected to decrease significantly, beginning in earnest in the second half of 2025.

“Despite America’s acute housing deficit, an interesting trend emerges when examining the multifamily sector — there is actually excess supply.”

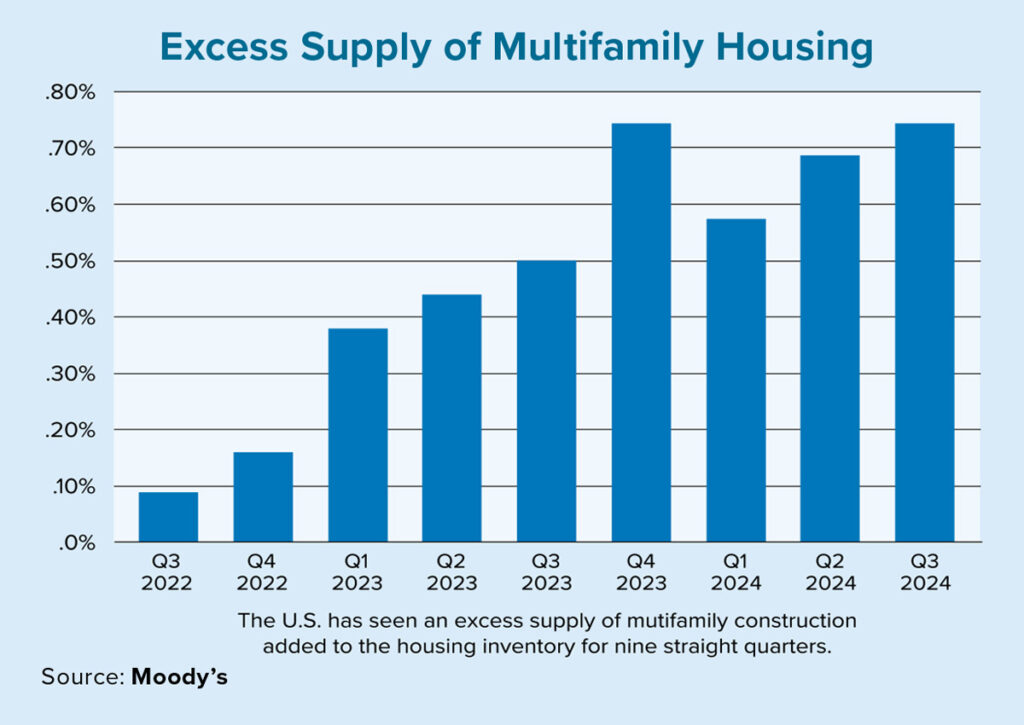

Despite America’s acute housing deficit, an interesting trend emerges when examining the multifamily sector — there is actually excess supply on a national scale. To clarify, excess supply was defined as total completions minus net absorption on a rolling 12-month basis.

Positive values indicate that completions exceed net absorption, signifying excess supply. Conversely, negative values, where net absorption surpasses total completions, indicate excess demand.

To account for variations in inventory size — particularly across metropolitan areas and to enhance comparability — excess supply (or demand) was expressed as a percentage of inventory. The data shows that, as of the third quarter of 2024, the United States recorded an excess supply-to-inventory ratio of 0.74%. Notably, this marked the ninth consecutive quarter in which supply exceeded demand.

In terms of regional performance, the Southwest reported the highest ratio of excess supply-to-inventory at 1.49% followed by the south Atlantic at 0.94%. On the other end of the spectrum, the West and Northeast reported relatively lower ratios at 0.39% and 0.43%, respectively. Lastly, among the five regions tracked by Moody’s, the Midwest was in the middle of the pack at 0.54%.

The length of time from the authorization of construction (i.e., building permit) to completion is generally longer in the Northeast and West, which at least partially explains their lower ratios.

In fact, Tacoma, Washington — from the Western Region — reported the lowest excess supply-to-inventory ratio among 82 primary markets at -0.89%. Its negative value indicates the market is characterized by excess demand. Furthermore, Austin, Texas — from the Southwestern Region — had the highest excess supply-to-inventory ratio at 2.97%.

While the multifamily sector is currently experiencing excess supply on an aggregate level, it is important to emphasize that this does not preclude the United States from having a significant housing shortfall. Excess supply is inherently short-term or cyclical in nature given the 12-month look-back period used in the definition.

In contrast, the housing deficit in the United States is a structural, long-term problem that reflects the cumulative effects of years of underbuilding. In other words, these two conditions are not mutually exclusive. As evidenced by the regional and metropolitan results, certain areas of the country may deviate from the broader trend due to factors such as economic policies, sectoral composition, demographics and other localized influences. While 2024 was a good year for residential construction, more are certainly needed to fill the gap.