Many experts believe that 2020 will go down as the worst year ever for the U.S. office market. This is not only because the COVID-19 pandemic has shut down operations at many office properties, but the general success of work-from-home measures has brought into question how businesses will lease space in the future.

Pundits have already started to debate the need for office space moving forward. Many believe that companies will downsize their footprints regardless of future growth while others recognize that the collective benefits of working on-site cannot be overstated. Indeed, the demise of the office market has been wildly overtold, just as many misread the future demand for dense downtown office space after 9/11.

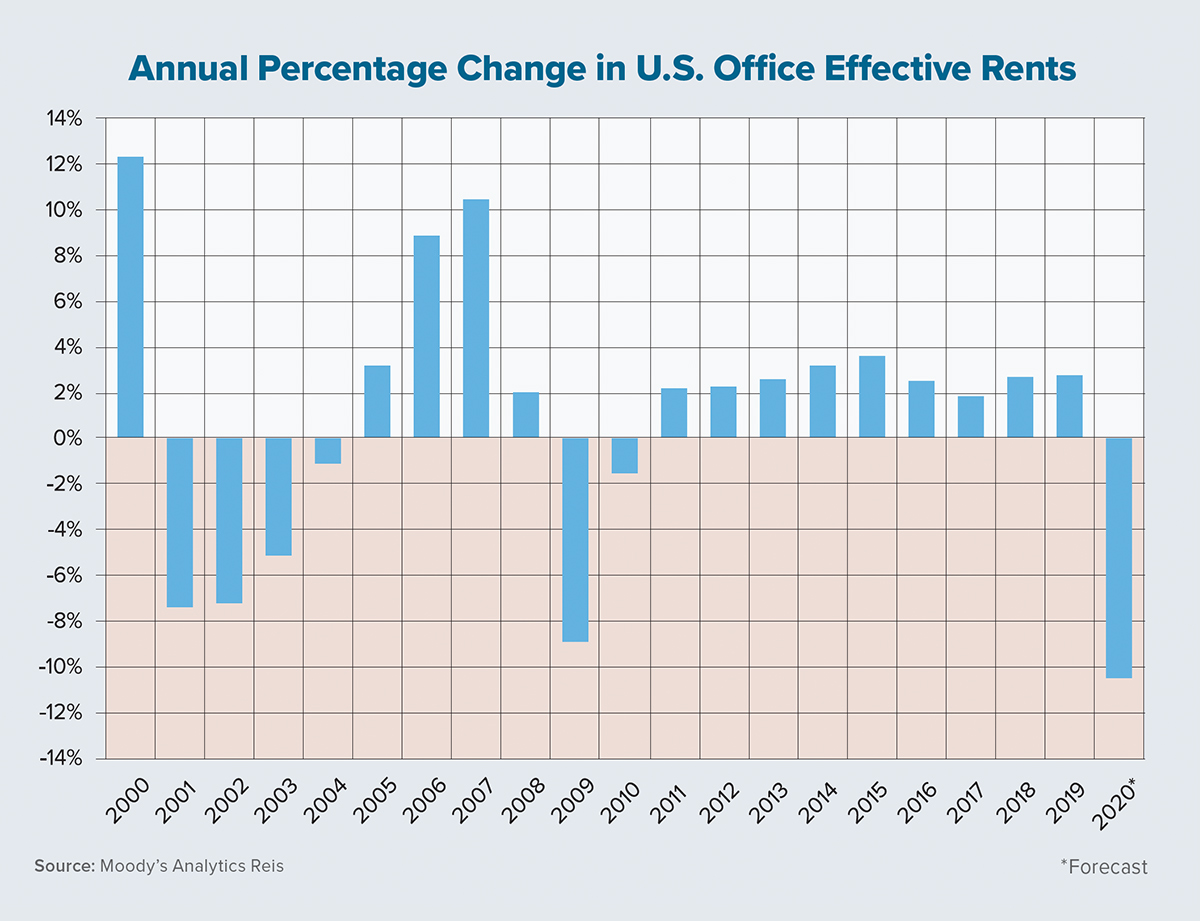

Still, the latest Moody’s Analytics Reis forecast for U.S. office rents calls for prices to decline more dramatically this year than in any other. Among the country’s top 79 metro-area office markets, our forecast calls for a 10.5% annual decline in effective rents in 2020, which is steeper than the record annual decline of 8.9% in 2009.

The next question is whether 2020 will be the worst year for each metro’s office market. The answer is, not even close. For those too young to remember, the dot-com bust of the early 2000s hit Silicon Valley office rents especially hard after the explosion of internet companies in the late 1990s drove prices up rapidly. Take San Francisco, where the average office rent fell 42.8% in 2001 after climbing more than 53% in 2000 alone.

Indeed, 19 of the top 79 metros incurred their worst office-rent decline in 2001 or 2002. This included other West Coast tech hubs such as Seattle and Oakland, as well as Dallas, Boston, Denver and Northern Virginia. In fact, across the U.S. as a whole, the collapse of tech companies in the early 2000s combined with 9/11 caused office rents to fall four years in a row (as the chart on this page shows) for a cumulative effective rent decline of 19.3% from 2001 through 2004.

Although the Great Recession was harder on the overall economy than the dot-com bust, only six metros (including Los Angeles, San Diego and Tampa) incurred their worst office rent decline during the former period. The cumulative effective rent decline for the U.S. from 2008 through 2010 was 10.2%. Four other metros (including Philadelphia, Baltimore and Jacksonville) sustained their steepest declines in the early 1990s. The cumulative U.S. rent decline for that period was 7.8%.

Fifty-one metros are on track to have their sharpest office-rent decreases in 2020. The average expected decline across these metros is 6.8%. New York City leads this pack with an estimated regression of 20.8% as it absorbs the impact of having high concentrations of COVID-19 cases, as well as some of the strictest government-imposed shutdown and reopening measures. Similar to San Francisco’s story in the early 2000s, however, New York is expected to suffer more this year because it had relatively healthy growth in recent times. Its average rent increase over the past five years was 3.2%, higher than the U.S. average increase of 2.8%.

The key difference between the current recession and past ones is that today’s is sharper but is expected to end sooner. Our forecast expects effective office rents to decline by 1.3% in 2021 for a cumulative decline of 11.7% for the two-year period. As referenced, this is less severe than the cumulative drop of the early 2000s.

Pundits will continue to debate about how the fallout from the pandemic will affect future demand for office space. Many will agree that office workers prefer some flexibility for telecommuting but ultimately want to get back to their old desk and see their colleagues in person. The more critical question is when the virus will be contained and few people can answer that. Assuming the worst is behind us, this will surely be a bad year, but the office market has suffered through and survived bad years in the past. ●