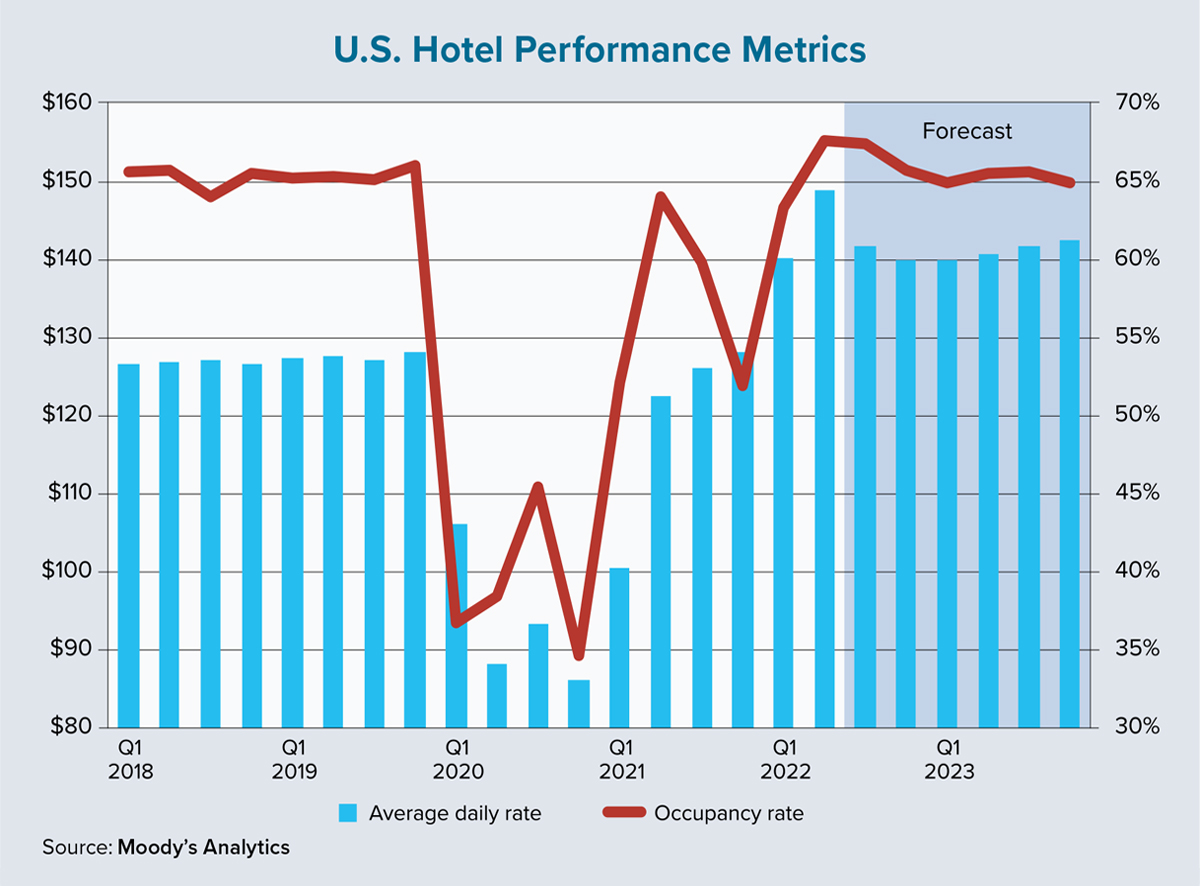

From a historic perspective, national-level performance metrics for the hotel sector have been surprisingly steady. In a given year, opposing patterns of peak business, event and leisure travel have typically provided balance to occupancy rates, average daily rates (ADR) and revenue per available room (RevPAR).

Summer leisure travel is replaced by robust autumn business travel, which then makes way for holiday and conference travel, and finally, spring break and another round of business and event travel to round out a 12-month period. Tracking the data between 2000 and 2019 validates this narrative. In fact, when excluding the two recessionary periods in this time frame, Moody’s Analytics found that occupancy rates have consistently hovered in a tight range of 60% to 65%.

All of this, however, was before the COVID-19 pandemic put a sudden end to nonessential travel. Hotels suffered mightily in the early stages of the health crisis. By March 2020, national-level occupancy declined to only 36.7% while ADR followed suite and dropped from a steady average of $127 to $108, a level not seen since shortly after financial crisis of 2007-08.

Unfortunately for the hospitality sector, the first month of the pandemic was far from the trough. A slight uptick in travel during the summer months of 2020 was followed by a second wave of infections that fall. Occupancy further dipped to 34.6%. Meanwhile, at only $88, ADR plummeted to its lowest level since the 1990s. At this point, hotel owners were having difficulty keeping up with debt payments. Moody’s data shows that the share of hotel assets tied to commercial mortgage-backed securities (CMBS) that were at least 60 days delinquent increased to about 15%.

Over the course of 2021, vaccination rates increased and various metrics of travel rebounded. The prevailing trend for hotel performance turned quite positive as occupancy and ADR quickly rose while CMBS delinquency rates began to drop. By late spring of 2022, occupancy rates had fully recovered and ADR jumped to record highs. By the end of second-quarter 2022, ADR was about 15% above its pre-pandemic peak.

Two questions remain. First, does this record performance have staying power? Second, will a lack of large-scale seasonality again reign supreme for the hotel sector? The answer to both questions lies in the analysis of the current situation.

To fully evaluate conditions, both supply and demand changes must be accounted for. On the supply side, while inventory declined substantially though the early portions of the pandemic, it has since fully rebounded. The number of available rooms is now 2.4% higher than its level at year-end 2019.

Consequently, fully recovered occupancy rates must require robust demand. On this side of the equation, much of the data and anecdotal evidence support leisure travel as the primary driver. During this year’s Labor Day weekend, the numbers of travelers passing through security checkpoints at U.S. airports slightly exceeded their 2019 levels. In subsequent weeks, however, numbers receded back toward 90% of pre-pandemic levels. This is likely due to a lack of business travel, which typically would pick up the slack for seasonal leisure travel declines.

So, if business travel has not fully returned, will ADR and occupancy be able to maintain their current pace? Not likely. Without strong business travel, occupancy in the latter half of 2022 is likely to recede a bit. Furthermore, ADR has been at least partially inflated due to shorter booking windows. Travelers were often waiting until the last minute to book, which typically resulted in fewer available lodging options and less price sensitivity.

As COVID-related health concerns subside, booking windows will likely increase again and travelers will be more likely to have the time to search and/or wait for lower room rates. Additionally, corporate and event travel will continue to rebound. While this is a boon for hotel demand, these mass bookings often come with significant discounts and will cause ADR to revert to its long-run average. As for the lack of seasonality, a full return of business travel is likely to be a slow process. Thus, at least for the near future, mild seasonality will be the new normal. ●