The effects of the COVID-19 outbreak across the U.S. economy are far-reaching. It’s expected that gross domestic product in the second quarter of this year will fall at a record rate, something in the range of a 30% annualized decline, which would be three times as severe as the previous record from 1958. With this kind of near-term outlook, how should the commercial mortgage industry think about downside risks for the multifamily-housing sector?

In formulating assessments of downside risk, at least three factors must be considered. First, we should study how specific geographic markets reacted during prior downturns. Some markets tend to experience larger numbers of moves during downturns, prompting vacancy rates to spike and rents to fall at various magnitudes.

For example, as our Moody’s Analytics Reis analysis shows, markets such as New York City and San Francisco tend to have relatively stable vacancy rates even during downturns. The distress, however, manifests more aggressively through negative effective rent growth.

Second, we should look at any recent evidence of oversupply. With close to 11 years of consistently strong performance, developers have tended to favor multifamily over other property types. In certain submarkets, construction of new apartments has reached historic levels, based on the 40 years of data tracked by Moody’s Analytics Reis.

Finally, we should be wary of any recent record of weak performance. A large amount of new apartment supply coming online isn’t necessarily an issue if occupancy rates hold steady. For some markets, however, recent historical performance shows that vacancy rates have started to climb. This suggests that implicit demand has not kept up with inventory growth.

Join 210,000 mortgage professionals

Get the news, trends and industry updates in your inbox to become a better mortgage originator. Subscribe to emails below.

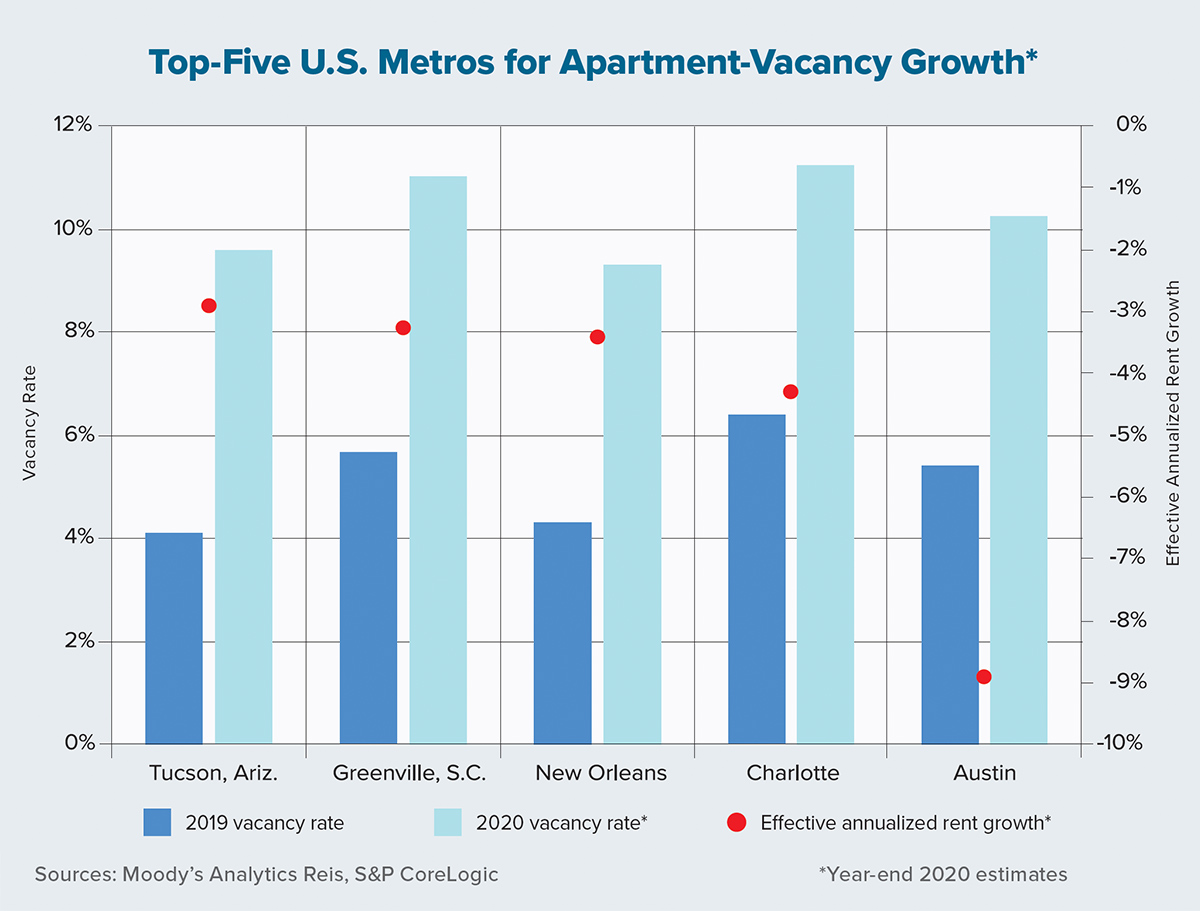

In the chart on this page, we present the top-five U.S. markets ranked in order of estimated vacancy-rate increases over the course of 2020 under the scenario of a protracted recession. This references a worst-case scenario in which the economy continues to contract until third-quarter 2021. Each of the markets in the chart are anticipated to have weakening occupancy rates and the stress points also manifest in rent declines.

In a protracted-slump scenario, New York apartment vacancies are expected to rise annually by 260 basis points to 6.5% at the end of this year. Effective rents are projected to decline by 5.8% — a larger decline than four of the five markets on the chart. Similarly, San Francisco vacancies are expected to rise by 285 basis points to 6.9%, but effective rents may fall by as much as 12.3%.

Occupancy rates and rent prices are the key determinants of top-line revenue for commercial real estate owners. Market players will need to carefully monitor these variables.

Nationwide, multifamily vacancies reached 8.1% in early 2009 during the Great Recession. We project the vacancy rate will hit that level again only if a severe, prolonged recession occurs.

The multifamily sector has performed well over the past decade and vacancies dropped to near-record lows. Thus, the vacancy rate is starting from a lower base in this economic cycle relative to 2006-2007, when apartment vacancies began rising in response to the housing-market bust. U.S. apartment vacancies were at 4.7% at the end of 2019, but the Great Recession began with a rate of 5.7%.

Preliminary first-quarter 2020 data had yet to show significant distress for multifamily fundamentals, given that widespread shelter-in-place rules due to the pandemic weren’t implemented until mid-March. With many places enacting eviction-moratorium policies during the crisis, occupancy rates may in fact remain stable in the near term. But if tens of millions of Americans lose their jobs — and if the unemployment rate stays relatively high — then multifamily will not escape unscathed.