The U.S. office market rarely gets considerable attention — at least during this expansion. It has neither the strong rent growth that the apartment market has had, nor the soaring construction levels that the industrial and self-storage sectors have seen.

And, unlike retail, the office market has not seen closures, conversions or even negative net absorption on a macro level. Rather, the office market is the steady if boring property type that posts positive rent and occupancy growth on a consistent basis.

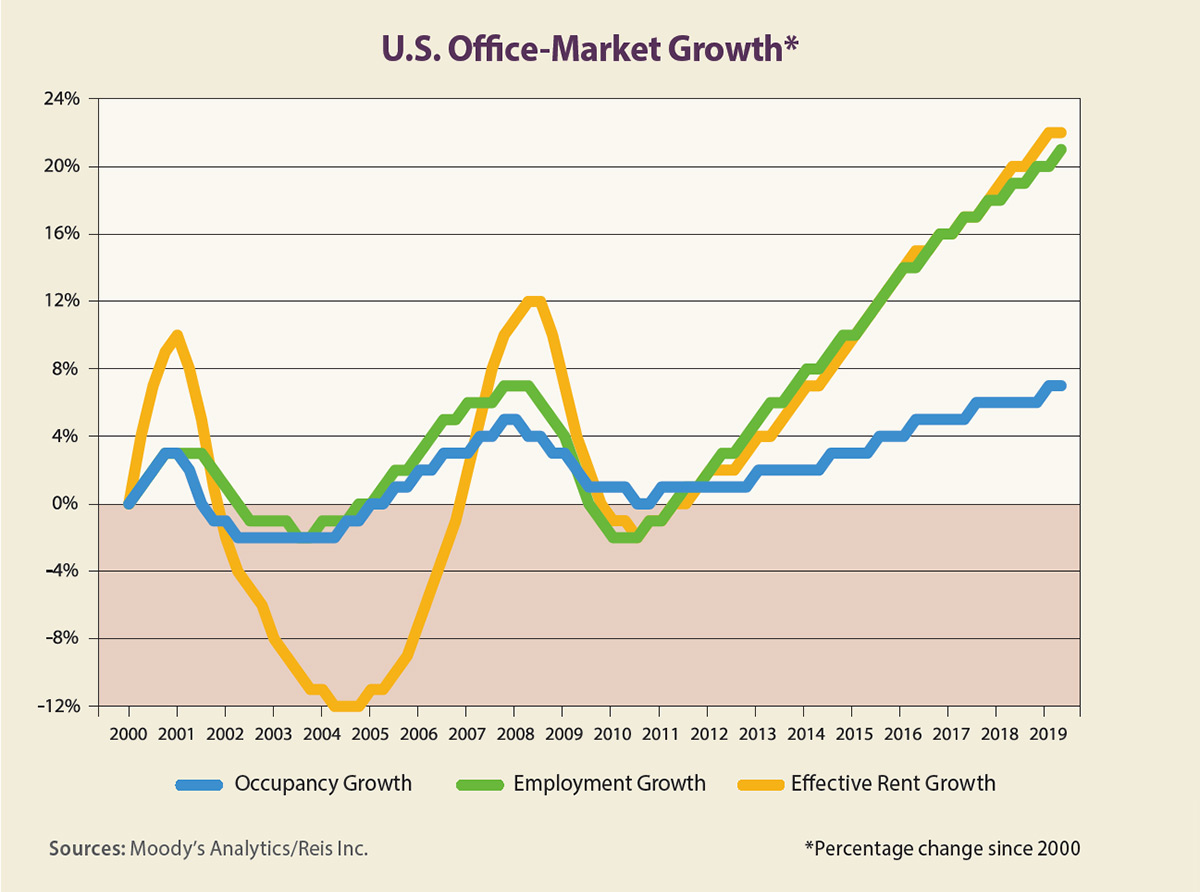

Those who are too young to remember previous cycles might be surprised to learn that this was not the case in the past two economic expansions. In the early 2000s, office rent growth climbed 2% to 3% per quarter. During the dot-com boom of the late 1990s and early 2000s, rent growth topped 5% in some quarters.

But in the past few years, occupancy growth has been considerably weaker. The chart on this page shows how occupancy growth moved in line with office employment growth from 2000 through 2007, but there has been a divergence since 2011. This is largely due to the open floor-plan trend in modern office designs. Removing cubicles and shrinking work stations allowed employers to lease fewer square feet per employee.

Our numbers that correspond to this chart show that the net absorption per added employee averaged 65 square feet from 2015 through 2019. This was just more than half of the net absorption per added job — 120 square feet — from 2004 to 2010. What is most striking is that the U.S. office vacancy rate has not fallen below 16% in 10 years, after dropping as low as 8% in 2000. This subdued pace has naturally kept rent growth low, as this has averaged 0.6% per quarter, or less than 3% per year, for the past five years.

The good news is that although occupancy growth has decelerated a bit in 2019, rent growth has held steady at this 0.5% to 0.6% average quarterly pace. The bad news is that the gap between the healthy markets and weaker ones has widened slightly as eight metro areas had quarterly rent declines in the second quarter of this year, including Rochester, New York; Milwaukee; Chattanooga, Tennessee; Wichita, Kansas; Providence, Rhode Island; and Little Rock, Arkansas. Their rent drops were less than 1%.

Metros with the strongest quarterly rent growth at that time included Minneapolis, San Antonio, Seattle, Austin and Louisville, Kentucky, each of which had growth of 1.2% to 2%. Another sign of the widening gap is that 21 of the 82 metros tracked by Reis Inc. lost office jobs during the prior 12 months, including Rochester and Providence but also, oddly enough, Minneapolis. Other metros, however, posted strong office job growth: San Francisco, Orlando, Dallas, Phoenix and Nashville had year-over-year job growth rates of 2.8% to 3.7%.

Despite this lackluster growth, however, office investment has remained steady over the past five years, even beyond the gateway cities. After dropping a bit in first-quarter 2019, office transaction volume in the top 50 metros jumped back to $24 billion in the second quarter of this year, in line with the volume in second-quarter 2018. And for the top 50 metros, the average price jumped to $320 per square foot, aided by Google’s purchase of a Manhattan property for nearly $2,000 per square foot.

This is the longest U.S. economic expansion ever recorded. One reason why the expansion has lasted so long is because the annual rate of growth has stayed so low. This sluggish growth has kept investors from overzealously speculating, which led to asset bubbles in the past.

But the clouds have grown darker with the threat of a trade war, and the Federal Reserve has already started to lower the overnight rate. A recession would surely hurt the office market, but the numbers have yet to show that a recession is imminent. The inverted yield curve seen this past August is usually a tell-tale sign that a recession is approaching. We will have to wait and see.