Rent-control policies tend to be highly politicized. Advocates believe that because rents have significantly risen relative to the earning power of households, the only solution is to regulate how much landlords can raise rents. Opponents believe that any form of rent regulation burdens landlords and discourages new construction, which further constraints housing-supply growth and worsens the problem that regulation was supposed to solve.

Recently, multiple states have enacted rent-control regulations designed to address the rapidly accelerating housing costs in these supply-constrained areas. In February 2019, Oregon passed Senate Bill 608, which included an annual cap of 7% plus inflation for rent increases. The cap applies to a property once it turns 15 years old.

This past June, the state of New York passed measures that effectively locked in all current rent-stabilized units in New York City. The new rules strengthen existing rent laws and give other cities in the state the ability to pass their own rent regulations. And this past October, California passed Assembly Bill 1482, which caps annual rent increases at 5% plus inflation.

Although each of these measures could potentially create a housing crisis, there are a number of misconceptions about them. In short, these recently passed rent regulations are unlikely to have a devastating impact on future supply growth.

New York City’s new laws apply to the current stock of rent-regulated apartments and some newly built market-rate apartments. But the statewide rules do not apply to the current stock of market-rate apartments, nor to public housing or any type of federally subsidized housing.

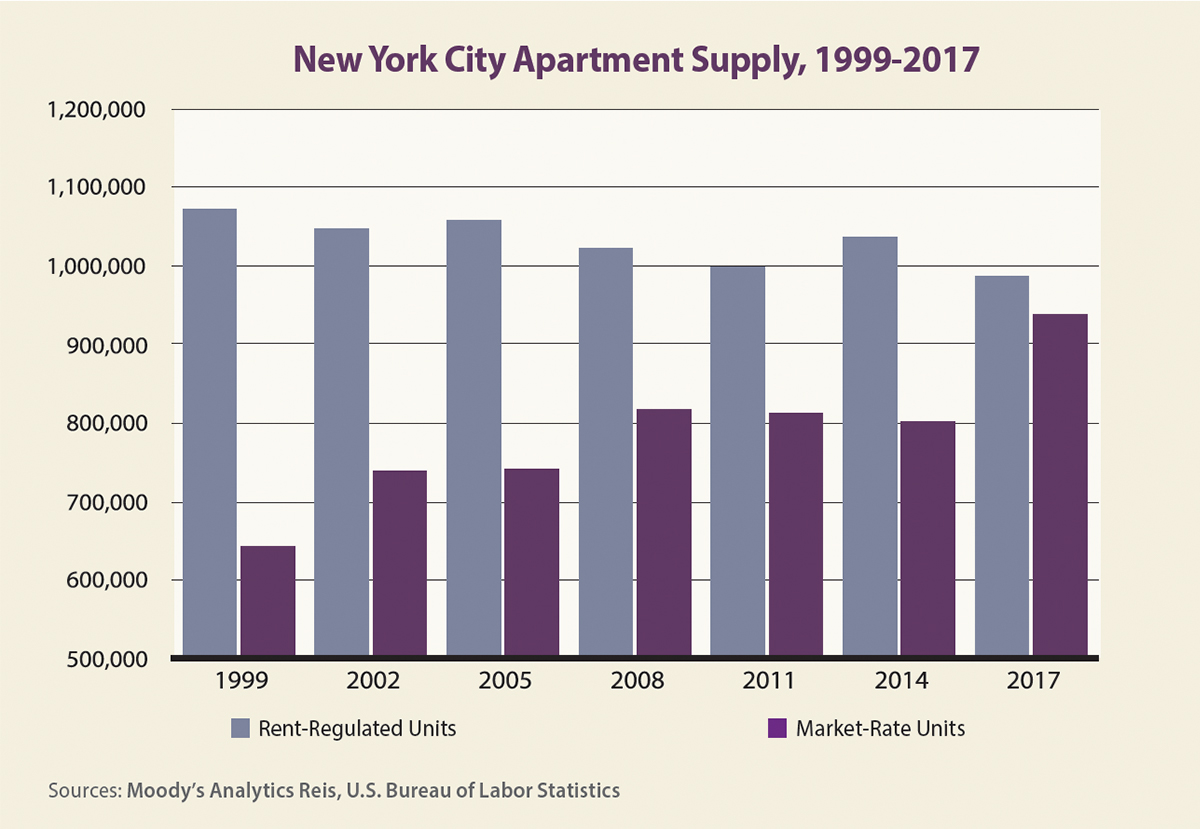

As of 2017, New York City had about 988,000 rent-regulated housing units, nearly half of the city’s 2.2 million rental units, although the former number declined from a high point of 1.07 million in 1999, per Moody’s Analytics Reis data. Thus, the supply of rent-regulated units declined by 8% during that 18-year period, while the supply of market-rate units increased by about 293,000 units (45.6%), as the chart on this page shows.

In New York City, many new apartment buildings are built under the current Affordable Housing New York program, which requires 25% to 30% of the units to be affordable for qualifying tenants. This program, which was enacted in 2017, is exempt from the new regulations if the units have rents that exceed $2,774 per month.

These market-rate units are not subject to rent caps and can be raised without restriction as long as the starting rent is above the threshold. This means landlords are only subject to rent regulations on market-rate units with initial rents below the threshold, as well as stabilized units that were already regulated prior to June 2019.

In short, the new regulations will create a small set of winners and losers. The winners include tenants who will see lower rent growth — those who are currently occupying a rent-regulated apartment and those who qualify for an affordable unit built in the future under the Affordable New York program.

Among the losers are owners of rent-regulated apartments who can no longer “decontrol” units by moving them from regulated to free-market status, or by increasing rents to cover renovation costs. And commercial mortgage brokers who work with these rent-regulated properties will see reduced sales activity.

The new rent regulations in Oregon and California exempt any newly built apartments for 15 years. Although this seems to constrain apartment owners, few submarkets in the metro areas Reis tracks have seen steady rent-growth rates of 8% or more in California, or 10% or more in Portland, annual increases that also account for inflation.

Also, vacancy decontrol is still allowed under both Oregon’s and California’s new regulations. This means that owners can raise rents as they please for any unit that is vacated, but they must then adhere to rent caps in subsequent years for the new tenant’s lease.

In conclusion, even though the new rent regulations in New York, California and Oregon are designed to protect tenants, none of them are likely to deter the future supply growth of apartments. The fine print on exemptions in all three states underscores how these new rules will not curtail the incentive to build.