The 2020-2021 academic year proved difficult for the U.S. student-housing sector, a niche for investors in multifamily housing. Concerns about COVID-19 infections, as well as travel restrictions and hybrid education models, diminished the demand for space, causing a spike in the vacancy rate and capital-market malaise for this segment.

As progress continues toward a full reopening of the nation’s economy, many of these transitory pressures on student housing will diminish, but deeper problems are likely to remain. Rising costs and shifting sentiments have subtly placed higher education and student housing in a longer-term quandary.

Enrollment continues to decline across all types of two- and four-year institutions. The 3.5% year-over-year decrease in spring 2021 was another blemish in a decade-old downward spiral. In fact, enrollment in U.S. colleges and universities has declined by 2.25 million students (or about 12%) over the past eight years, according to the National Student Clearinghouse Research Center.

The traditional model of higher education was severely tested over the past year. With the potential for social interaction greatly diminished, many students — including the ever-important international contingent — chose to study remotely or take a year off. Consequently, the student-housing vacancy rate as measured by the number of beds increased by 270 basis points (bps) to finish this year at 7.9%, according to Moody’s Analytics Reis data.

Both the annual increase and the current vacancy rate represent record highs since we began tracking this data in 2014. Asking rents managed to increase by 2% for the year, but this can likely be attributed to renewals and prelease agreements.

From a regional perspective, the West — where pandemic-related restrictions tended to be the most pronounced — experienced a dramatic vacancy-rate increase of 640 bps to finish the year at 9.3%. On the other side of the spectrum, the rate in the Midwest increased by only 39 bps to 6.7%. Interestingly, the 240-bps jump in vacancies for the Southern Atlantic region was mainly due to a glut of new supply as net absorption posted a modest gain of about 5,200 square feet. The Midwest was the only other region with positive net absorption.

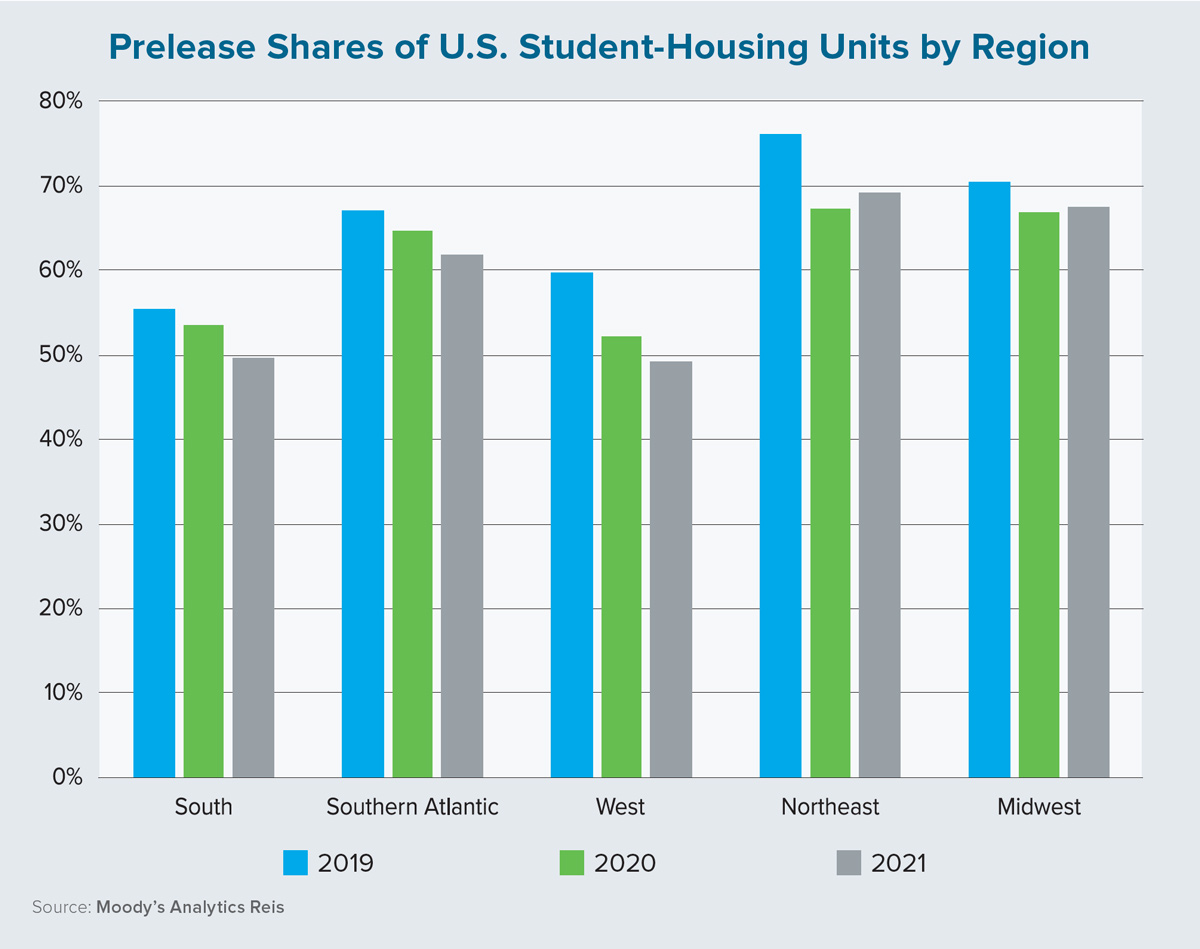

As the academic calendar turns the page to the 2021-2022 year, the student-housing sector still faces pandemic-related pressures. Preleasing, the best early indicator of near-term performance, shows widespread weakness. At 60.4%, the national rate is 1.4 percentage points lower than in 2020 and trails the 2019 level by 5.7 percentage points.

As the chart on this page illustrates, regional differences remain. While all five regions have lower preleasing rates in 2021 than two years earlier, the West faces the most severe negative pressures as this year’s rate is a whopping 10.6 percentage points below that of 2019’s.

In relation to 2020, the Northeast and Midwest are the only regions with higher preleasing rates in 2021. Given the increase in vaccinations, it is likely that more leases than usual will be signed at the last minute, but there are still enrollment concerns, especially from an international-student perspective. Vacancy rates will remain elevated and we anticipate rents pulling back by some 4% this year as landlords compete for diminished demand.

Given the longer-term trend of declining enrollment, distress in the student-housing sector will likely continue for the foreseeable future. Although we expect the vacancy rate to begin recovering in the 2022-2023 academic year, it is likely to remain above its 4.6% average from 2014 to 2019 through the end of this decade. Consequently, rent growth (which averaged 3.2% from 2014 to 2019) is projected to average only 2% over the course of this decade, even after excluding the two most recent academic years.

For many years, student-housing prospects were bright. Rent growth was solid and vacancy rates maintained modest levels even in the face of increasing inventory, but the story has shifted. Although there will be market-level differences in outcomes, higher education is facing a bit of a crisis and instability in the student-housing sector is a likely consequence. ●