With the global financial markets off to an uncertain start in 2023, the U.S. multifamily housing sector faces a number of challenges. These obstacles are driven by a combination of unique consumer preferences in the post-pandemic era and broader macroeconomic forces.

Over the course of 2022, Moody’s Analytics found that the multifamily vacancy rate fell by 30 basis points to 4.5%, while asking and effective rents increased on an annualized basis by 9.5% and 9.7%, respectively. But signs from the end of last year suggest that the apartment market has entered a period of adjustment.

As interest rates for home loans lingered on the higher side due to the Federal Reserve’s attempts to tame inflation, households that may have previously sought to exit rental housing via homeownership are likely to remain in the multifamily market. This has helped to sustain demand for more expensive and amenity-loaded Class A apartment units. Demand for Class B and C spaces has also been robust due to tight market conditions, even though affordability was already constrained by inflationary impacts on household budgets.

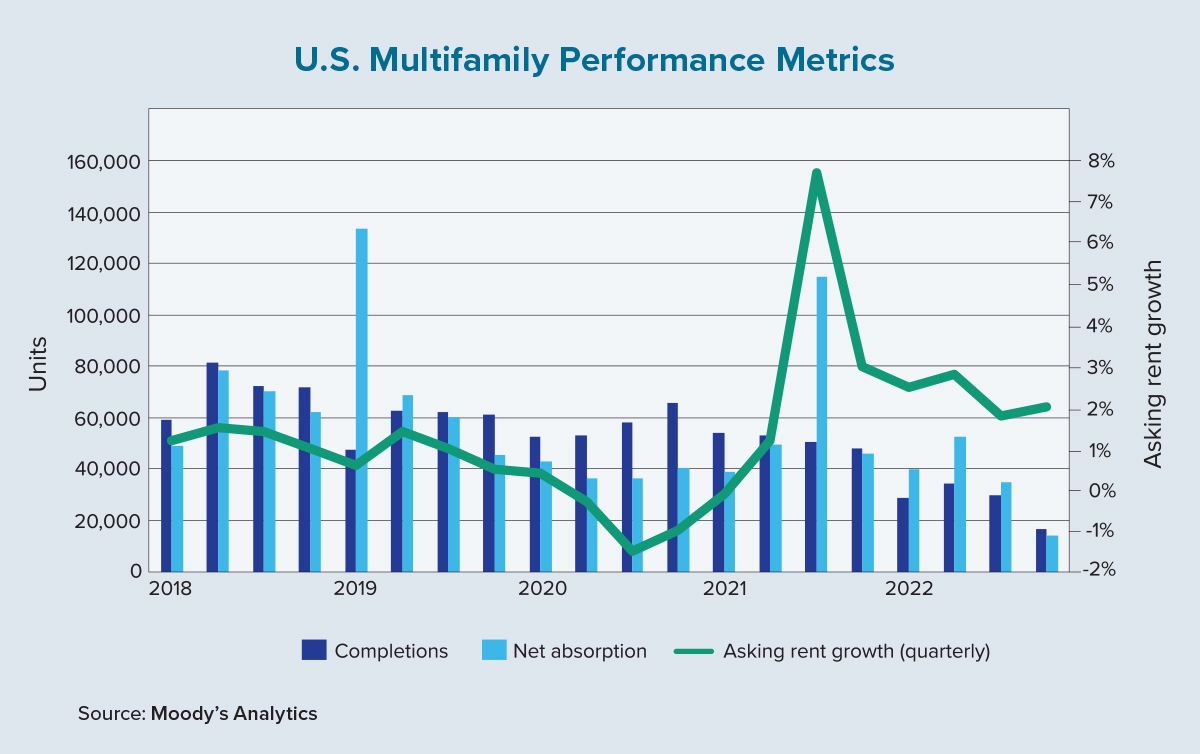

On the supply side, we anticipate record-level multifamily construction deliveries in 2023 after a slow year in 2022 (as shown on the accompanying chart). The average number of completions across these two years, however, will not deviate much from the sector’s five-year average. It’s also likely that construction financing constraints tied to higher interest rates and continued supply chain issues will delay some new projects and prevent completions from reaching some of the more optimistic forecasts.

In theory, however, exceptional supply growth could put downward pressure on the apartment market’s performance. This is especially true for Class A space, which already experienced more vacancies due to years of oversupply leading up to the COVID-19 pandemic.

As demand softens and completions possibly outpace net absorption in the near term, what does the supply-and-demand seesaw mean for multifamily rent growth? The answer is further deceleration on the horizon. The aforementioned market rent increases for all of 2022 were largely observed in the spring and summer months, with slowing growth and declines occurring in some metro areas to wrap up the year. Moody’s Analytics forecasts 2023 asking rent growth to cool to the 2% to 3% range.

Over the past three years, more than 90% (73 of 79) of the primary metros analyzed by Moody’s have had higher rent burdens than pre-pandemic days due to rents rising much faster than median household incomes. (Rent burden is measured by a rent-to-income ratio or RTI.) Seven of the top 10 metros with the largest disparities between rent and income growth are now found in the South Atlantic region, states that were popular post-pandemic migration destinations.

Metros that have enjoyed exceptional pandemic-related performance boosts, however, could be the first to see rent-growth moderation or declines. In fourth-quarter 2022, six metros had quarterly rent declines of more than 1%. Four of these (Baltimore, Memphis, Atlanta and Palm Beach, Florida) are in the South Atlantic region while the other two are in California (San Bernardino/Riverside and Ventura County).

Although the national average rent burden has reached the 30% RTI threshold, the deceleration of rent growth combined with continued wage increases will be welcome news for renters. But individual households may experience this relief differently. Desirable metros that have attractive demographic and economic factors may see further exacerbation of the rent burden, especially across moderate- and low-income households.

An imbalanced housing market mixed with macroeconomic uncertainty has left the multifamily sector in a precarious situation. While our baseline forecast indicates only slightly below-average performance for 2023, any policy or financial-market missteps have the potential to amplify the sector’s subtle weaknesses. ●