Moody’s Analytics

As expected, the slowdown for the industrial sector continued to manifest in the data for 2024. The vacancy rate for warehouse and distribution properties, for example, increased by 50 basis points annually to end the year at 7%.

While this remains below the sector’s long-term average, it’s worth noting that the vacancy rate has steadily increased in eight of the last nine quarters from its all-time low of 4.3% in the third quarter of 2022. Although completions continue to outpace net absorption, the gap has been narrowing, suggesting the pace at which any incremental softening occurs in the sector is expected to moderate.

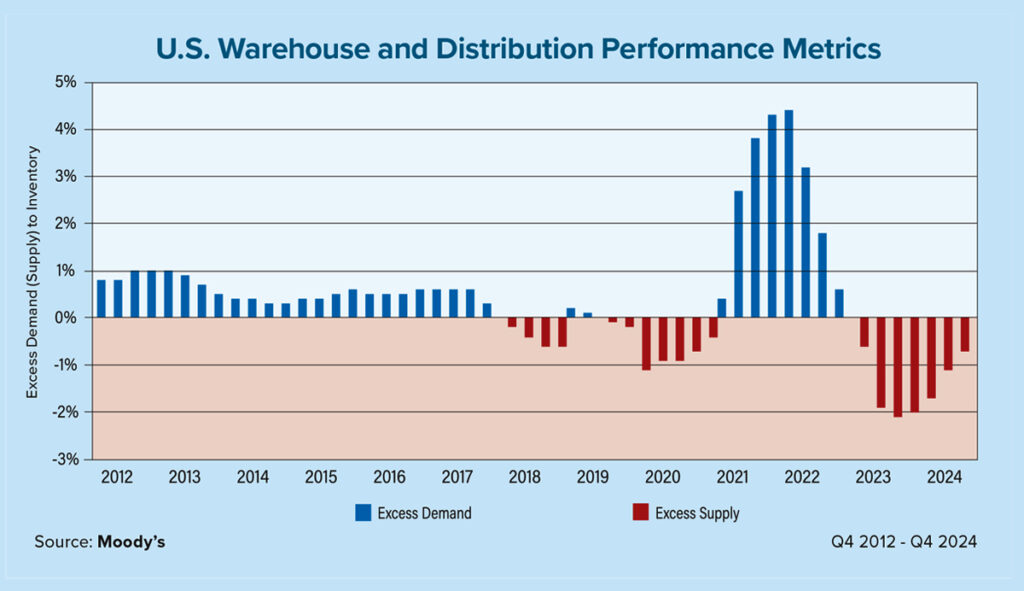

One such metric to support the previous statement is the nationwide excess supply-to-inventory ratio, which is illustrated on this page. First, to clarify, excess supply was defined as net absorption minus total completions on a rolling 12-month basis, divided by the size of the U.S. industrial market.

Thus, negative values are indicative of the market having excess supply and positive values are characteristic of excess demand. Moreover, a ratio of zero would imply that supply and demand are perfectly in balance. Given this context and returning to the graphic on this page, note that the excess supply to inventory ratio increased from -2.06% as of year-end 2023 to -0.66% as of year-end 2024.

In fact, the year-end 2023 value was the lowest on record going back to available data from 2011. As the gap between net absorption and completions continues to close, expect this ratio to approach parity by around the end of 2025. There will be regional differences, with the Southwest and Southern Atlantic regions, for example, likely to reach this equilibrium at a slower pace, given their relatively higher construction levels compared to demand.

As for rent growth, this too has manifested in a slowdown in the numbers for 2024. For instance, effective rents for warehouse and distribution properties increased by 1.6% annually in 2024 after increasing by nearly 5% in the previous year. Granted, this is nowhere near the level of rent growth observed in 2021 and 2022 from the pandemic-induced shock, but should nonetheless be considered healthy. Additionally, Moody’s baseline forecast expects rent growth for the industrial sector to increase by approximately 3% annually in 2025 and 2026, which is the highest rate of change across the core four commercial property types.

On the demand side, Moody’s baseline forecast over the next two years (and longer term) is underpinned by the dual tailwinds of e-commerce as well as reshoring and nearshoring manufacturing activities. The e-commerce share of retail sales has steadily risen since the turn of the century and could potentially reach 20% by the end of this decade.

This is important because e-commerce typically requires more space than traditional retail, thereby bolstering demand for industrial properties. As for nearshoring and reshoring, national security and political concerns have given rise to protectionist policies that are reshaping distribution networks.

While considerable short-term uncertainty remains, especially around tariff policies and perhaps to a lesser extent the CHIPS and Science Act, which authorizes about $280 billion in new funding to boost domestic research and the manufacturing of semiconductors, the fundamental need to store and deliver goods will likely remain unchanged, consequently reinforcing our long-term outlook.

Lastly, on the supply side, a slowdown in construction with inventory growth projected in the low- to mid-1% range over the next two years, is expected to support rent growth that is closer aligned with the sector’s long-term average. While 2024 unequivocally marked a period of moderating performance, the industrial sector’s rebalancing act is expected to persist throughout 2025.