This was supposed to be the year that clarity would emerge about whether interest rates were likely to stabilize. While the Federal Reserve lowered its policy rate by a full percentage point in the months after the September 2024 Federal Open Market Committee meeting, the benchmark 10-year U.S. Treasury yield has oscillated significantly — especially in April — around the low- to high-4% range.

The notion of higher-for-longer interest rates has continued to resonate, although the chances of a recession have risen, complicating the interest rate picture. It is important to note that despite elevated uncertainty about the Trump administration’s policies, particularly those related to tariffs, the labor market has remained remarkably resilient.

The U.S. economy has added nearly 17 million jobs since January 2021, and the unemployment rate remains historically low at 4.2%. Initial jobless claims, which can be viewed as a precursor to a weakening labor market, are still benign, remaining below pre-pandemic levels.

Even though employment and wage growth continue to moderate, incomes are still rising faster than inflation, which inevitably bodes well for consumer spending, the primary driver of U.S. economic activity. While economists are cognizant of the disconnect between the hard and soft data, should job growth hold steady, then this would inevitably be supportive for office space demand.

Having said that, the office sector is undoubtedly the most troubled commercial real estate property type in this economic cycle and is expected to experience further stress over the near term. This comes at a time when the office vacancy rate for the first quarter of 2025 reached 20.4%, the highest level in Moody’s nearly 50 years of available data.

Despite completions over the past five years remaining well below the sector’s long-term average and a projected transition to positive net absorption in 2025, excess supply conditions are expected to persist. This is primarily due to the negative impact on office demand from employees who work from home, resulting in vacancy rates that are expected to peak at about 21% nationally in early 2026.

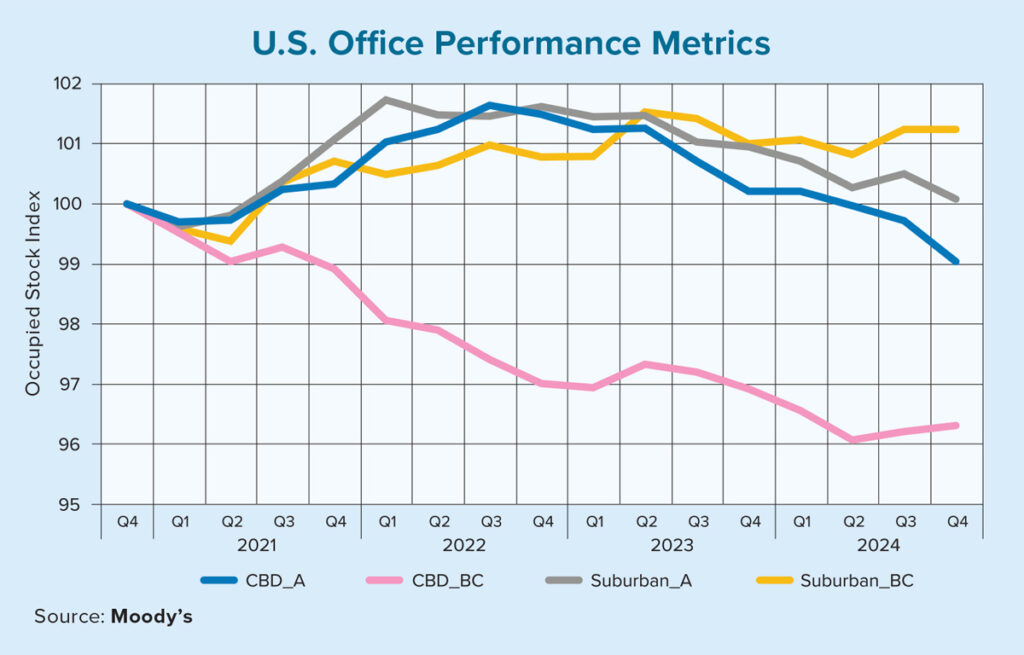

The location and quality of office assets will remain important determinants of performance. For example, as illustrated in the chart above, Class B and C offices located in central business districts (CBDs) have significantly underperformed their Class A counterparts over the past four years.

This is evidenced by the approximately 4% cumulative decline in their occupied stock index. Furthermore, Class B and C offices are likely to have a greater risk of functional obsolescence. This is because as employers reevaluate their space needs to prioritize flexibility and modernity, buildings with outdated layouts and limited adaptability are increasingly seen as less desirable by tenants, resulting in lower renewal rates. Although considering the average length of an office lease in a central business district is typically around 10 years, the pace at which tenants reassess their space needs (and get reflected in the data) is evidently a gradual and evolving process.

As for suburban offices, the continued embrace of remote work has translated into flat-to-positive performance across the Class A, B and C subsets, in contrast to more centrally located offices, where both subsets reported declines in occupied stock. Lower-cost leases in the suburbs are particularly attractive to tenants focused on reducing operational expenses. For instance, when holding class type constant, transitioning from a central business district office to a suburban office would result in about a 35% rent discount. Keep in mind, this estimate is at the national level, so regional differences would certainly apply.

While the broader economic outlook is largely clouded by policy uncertainty, should the labor market continue to generate steady — albeit moderating — job gains, then office space demand is likely to have a modicum of support, particularly in well-located, high-quality assets. Structural challenges, such as evolving workplace dynamics, rising vacancy rates and the recent wave of canceled leases for government office space, are likely to keep pressure on the sector in the near term.