Last year was a true test for Scotsman Guide’s Top Mortgage Lenders. A strong start to 2022 quickly turned into a scramble as interest rates rose, borrower affordability declined and mortgage companies were heavily impacted. Staying in the black became a challenge that loan originators, branch managers and executives had to work together to overcome.

The Top Mortgage Lenders worked harder than ever to stay on top in 2022. Strong referral pipelines, high home prices, smart financial moves and innovative loan programs helped to keep these lenders afloat while their originators worked to bolster individual books of business. And while this year’s numbers reflect a sharp decline from the 2020 and 2021 production periods, total volume actually increased from the 2019 production year (prior to the COVID-19 pandemic), as did the average loan size.

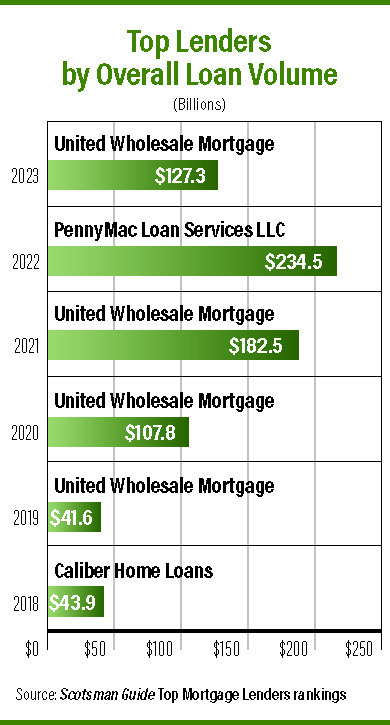

Welcome to Scotsman Guide’s 11th annual Top Mortgage Lenders rankings. United Wholesale Mortgage took first place on the Top Overall Lenders list for the fourth time, closing nearly 350,000 loans for an aggregate volume of $127.3 billion. Last year’s champion, Pennymac, took second place by closing $109 billion across more than 350,000 loans. Rounding out the top of the list are some familiar names: Newrez LLC/Caliber Home Loans finished in third place (216,000 loans, $68 billion), LoanDepot was fourth (161,000 loans, $53.8 billion) and AmeriHome Mortgage was fifth (152,000 loans, $46.3 billion).

On the following pages, you’ll also find our usual spread of specialty rankings. Three well-known lenders defended their No. 1 spots from last year in the retail, wholesale and correspondent divisions. LoanDepot remained in first place among the Top Retail Lenders, closing 88% of its volume in this category for more than $45 billion in retail loan volume. United Wholesale Mortgage again wears the Top Wholesale Lenders crown, closing all $127 billion of its volume in this category. And Pennymac kept the No. 1 spot for Top Correspondent Lenders, doing 78% of its business in this category for more than $86 billion in correspondent loan volume.

A new No. 1 can be found on the Top Non-QM Lenders list. Change Lending did 70% of its total volume last year in nonqualified mortgages, earning the top spot with more than $4 billion in non-QM origination volume. Pennymac swept the government lending categories, taking the No. 1 spot on the Top FHA Lenders and Top VA Lenders lists. In each category, Pennymac closed at least 83,000 loans with aggregate volumes exceeding $23 billion.

So far, 2023 has been marked by uncertainty, and the mortgage industry continues to adjust to the new normal. In these times, Scotsman Guide is proud to offer a moment of celebration. Congratulations to all of our Top Mortgage Lenders. Enjoy the summer sunshine and, as always, thank you for reading.

Verification: Hannah Darden, Brian Warr

United Wholesale Mortgage: No. 1 Top Overall Lenders

Industry giant United Wholesale Mortgage (UWM) is back on top after closing more than $127 billion in loans last year. In a recent conversation with Scotsman Guide, UWM chief operating officer Melinda Wilner said the company achieved this success by listening to brokers and launching useful new products.

“We’re following the same strategy we’ve always followed, which is really supporting the independent mortgage broker channel and giving them the tools, the technology, the products, anything that we can do to make their lives easier,” Wilner said.

UWM prioritizes the soliciting of feedback to better understand the needs of brokers and borrowers, she added. This leads to more useful product and technology development.

Wilner is excited about many of the tools UWM has brought to brokers over the past year. The company launched a training academy for new talent as well as loan officers who are switching from retail to the wholesale channel. UWM also revamped its closing system, started a program to help combat high title and closing costs, and launched Safe Check, which allows originators to prequalify their borrowers with a soft credit check that delays trigger leads.

“There’s an obscene amount of changes here every single day,” Wilner said. “We’ve always thought wholesale is the best way to go. I think that message is getting out there as we continue to educate consumers and as we get retail loan officers to bring their referral network in as well.”

Overall volume down compared to last year

The Top Mortgage Lenders saw their loan volumes moderate in 2022 and return to pre-pandemic levels after two years of historically high volumes. The 75 Top Mortgage Lenders closed a total of 2.6 million loans in 2022 with an aggregate value of $870.5 billion.

While this represents a decrease compared to the prior two years of rankings, it also is an increase from the volumes closed by the lenders in the 2020 rankings (based on the 2019 production year). That year, the top 75 lenders closed nearly 2.8 million loans for a total of $783.7 billion.

While total volume was higher this year, the total number of closed loans was lower, a reflection of escalating loan sizes over the past three years. The total volume to clinch the No. 1 spot also rose, from $107.8 billion in the 2020 rankings to $127.3 billion in 2023.

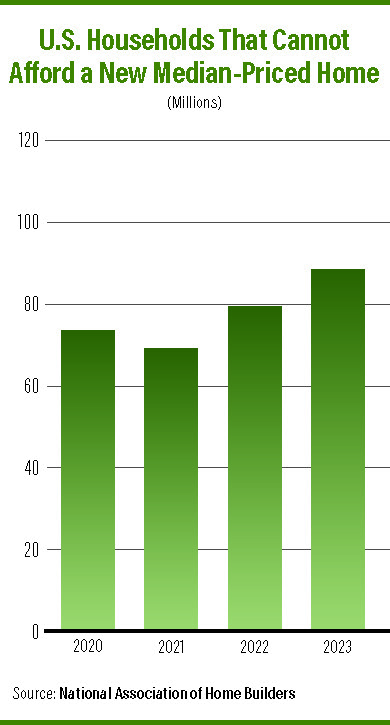

Majority of Americans can’t afford to buy a median-priced home

Only 36 million of the 132.5 million households in the U.S. can afford a new median-priced home, according to a special report from the National Association of Home Builders (NAHB). The report, released this past March, determines affordability based on the ability to qualify for a new median-priced home of $425,786 using a 10% downpayment and a 30-year loan with a 6.25% interest rate and no points.

Based on these numbers, a household needs an income of at least $129,645 to buy a home. Only 27% of U.S. households meet this threshold, while 73% (or 96.5 million households) do not.

Additionally, the NAHB calculated models which estimate the number of households that would be priced out by a $1,000 increase in the median home price. Using the same affordability calculations as above, an additional 140,000 households would be priced out with an increase of $1,000. The report also found that increasing the interest rate from 6.25% to 6.5% would price out another 1.3 million households.

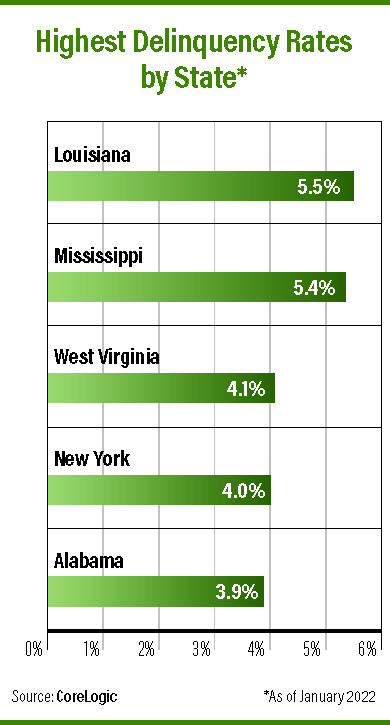

Mortgage delinquencies decline slightly

The U.S. mortgage delinquency rate decreased slightly during the year ending in January 2023, according to CoreLogic’s Loan Performance Insights report. Delinquency and foreclosure numbers are both near their historic low points and well below previous peaks in the spring of 2020.

This past January, 2.8% of mortgages were 30 days or more past due, including those in foreclosure. This represented a 50-basis-point (bps) decrease from January 2022 and a 4.5% decrease from the early stages of the COVID-19 pandemic. The states with the highest overall delinquency rates at this time were Louisiana, Mississippi, West Virginia, New York and Alabama.

While overall numbers are down, breakdowns tell a slightly different story. Mortgages in early-stage delinquency (30 to 59 days past due) and mid-stage delinquency (60 to 89 days overdue) were up slightly on a year-over-year basis. The foreclosure inventory rate in January was 0.3%, up 10 bps during the year. But the share of mortgages in serious delinquency — 90 days or more past due, including those in foreclosure — was down 60 bps during the year.

Despite some numbers rising slightly, they remain near historic lows and changes are relatively flat. The CoreLogic report also noted that while annual home equity gains slowed significantly in fourth-quarter 2022, borrowers still have about $270,000 in equity on average — a significant safeguard against foreclosure. The U.S. unemployment rate also stayed below 4% during the first three months of 2023, another good sign for foreclosure prevention.

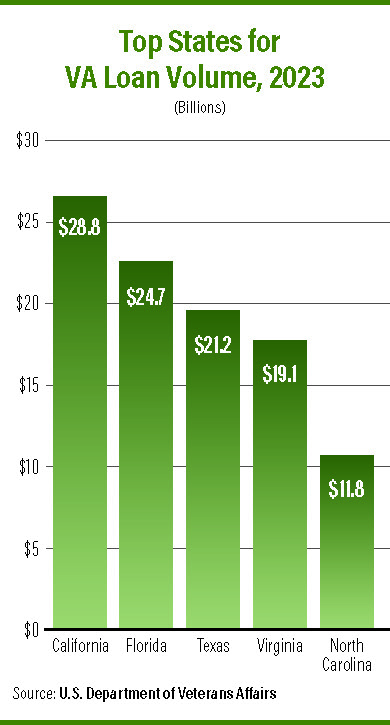

VA loan volume falls by half

The total number of loans closed through the U.S. Department of Veterans Affairs (VA) fell by nearly half in 2022, according to VA data. In 2022, roughly 746,000 VA loans were closed, compared to more than 1.44 million in 2021. The dollar volume of these loans fell by 43%, from $447.2 billion to $256.6 billion.

As usual, the most populous states led the charge in terms of total VA loan volume. California, Florida and Texas took the top three spots, each with more than $20 billion in volume. The states of Virginia, North Carolina, Georgia and Washington followed. Colorado, Arizona and Maryland rounded out the top 10, each with more than $8 billion in VA loan volume.

The highest average loan amounts were found in Hawaii and Washington, D.C., with average loan sizes in these locations topping $660,000. California’s average VA loan size exceeded $520,000, while the territories of Guam and the U.S. Virgin Islands each had average loan amounts of more than $450,000. The smallest average VA loan sizes were found in Puerto Rico ($199,632), Ohio ($237,943), Iowa ($238,352) and Michigan ($238,825).