Housing markets in the U.S. and Canada have experienced some of the same challenges since the start of the COVID-19 pandemic. These include strong homebuyer demand amid extraordinarily low mortgage rates, declining inventory of homes for sale and a resultant surge in price appreciation that peaked at about 20% year over year in the spring of 2022.

Also, the same inflationary pressures that the U.S. has been struggling with have impacted the Canadian economy, where the annual rate of inflation peaked above 8% in the summer of 2022 — the same time that U.S. inflation surpassed 9%. As a result, both countries have undergone an aggressive monetary tightening cycle, which has had an unfavorable impact on mortgage rates and the respective housing markets. In the U.S., existing home sales declined by 18% from 2021 to 2022 while Canada experienced a 25% pullback.

Nevertheless, there are some differences in the neighboring nations’ mortgage markets that have led to diverging trends since monetary tightening began. Four main differences, in fact, exist between the two markets.

First, Canada relies on five-year mortgages amortized over 25 years, meaning that the loan balance has to be refinanced at the end of the term. This exposes the borrower to mortgage rate hikes, which have been steep over the past year. Second, Canadian mortgages commonly have prepayment penalties that prevent borrowers from refinancing when interest rates fall, although loans are attached to borrowers and are thus transferable to another property.

Third, mortgage interest is not deductible in Canada. And fourth, Canadian banks (in sharp contrast to U.S. banks) generally keep loans on their balance sheets. This has impacted the difference in the mortgage rate spread across the two nations, with rates now somewhat higher in the U.S. than in Canada.

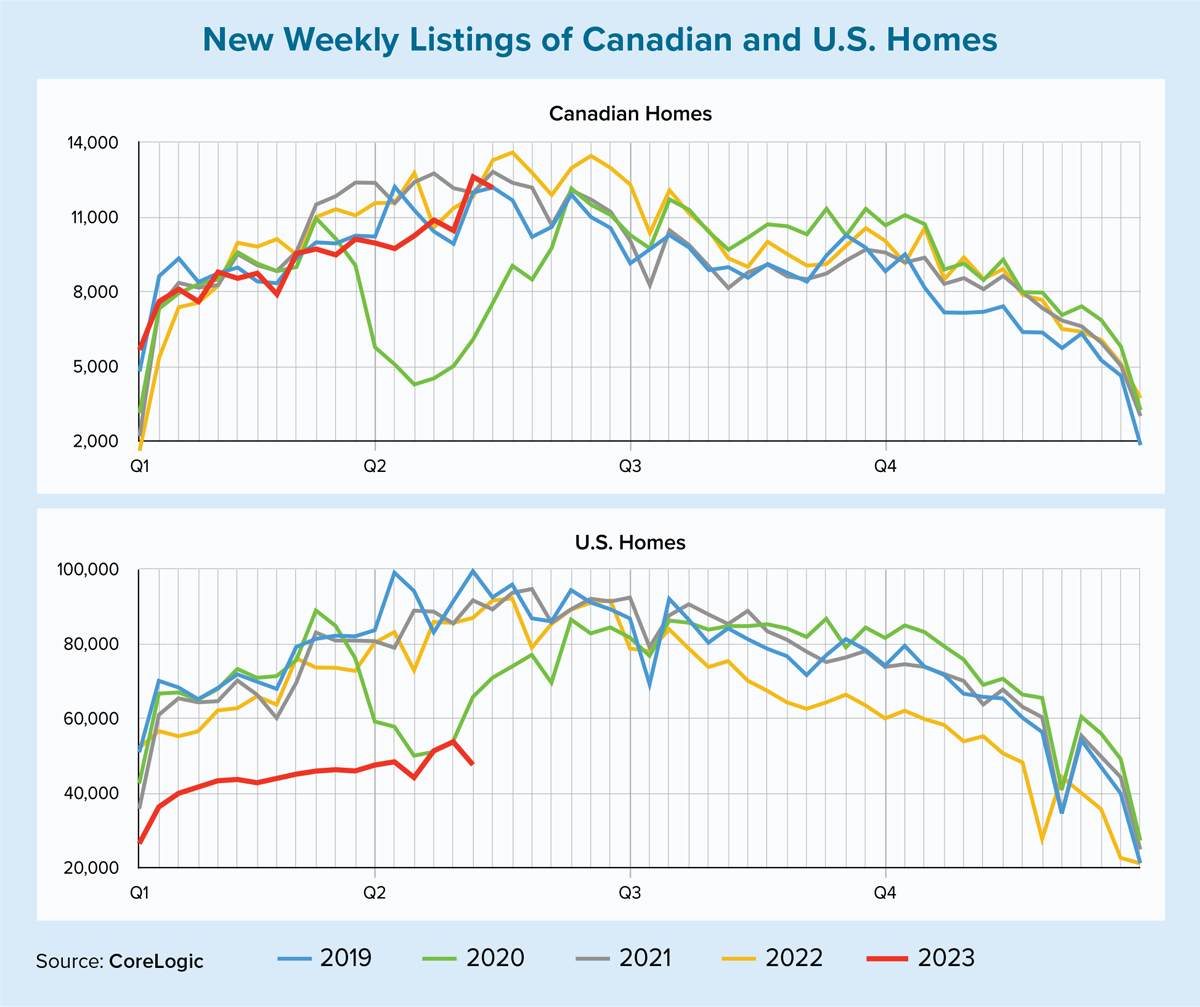

Given the differences in mortgage finance systems, Canadian borrowers tend to feel less locked in at low rates than U.S. borrowers, which impacts the availability of homes for sale and consequent sales activity. In the U.S., the inventory of existing homes for sale has been declining for the better part of a decade. This year, the number of new listings entering the market has been trending some 50% below the pre-pandemic levels of 2019 (and also well below 2022 levels) as homeowners are disincentivized to give up their historically low mortgage rate and sell their home.

As the chart on this page shows, active inventory across most U.S. markets is now at the lowest levels in the history of CoreLogic’s data series. This lack of inventory has considerably constrained home sales in 2023, which have fallen to the lowest levels in a decade. On the other hand, the chart also illustrates that Canada’s active inventory is back to pre-pandemic levels. As a result, home sales are forecast to exceed 2019 figures and come close to last year’s levels. Conversely, the U.S. market is expected to see another double-digit decline of about 17% in total home sales this year.

Nevertheless, differing mortgage systems and varying constraints on the availability of homes for sale have contrarily impacted home prices in the two countries. While annual rates of home price appreciation have decelerated in both nations, price growth in the U.S. stabilized at about 2% this past spring, according to CoreLogic data. With strong monthly gains recorded thus far in 2023, year-over-year growth is likely to end the year in the 4% range.

In Canada, meanwhile, a major house price index began recording annualized declines in December 2022, with the yearly pullback topping 8% as of April 2023. And while spring home prices north of the border were strong, it will take some time for the index to start recording positive yearly gains. ●