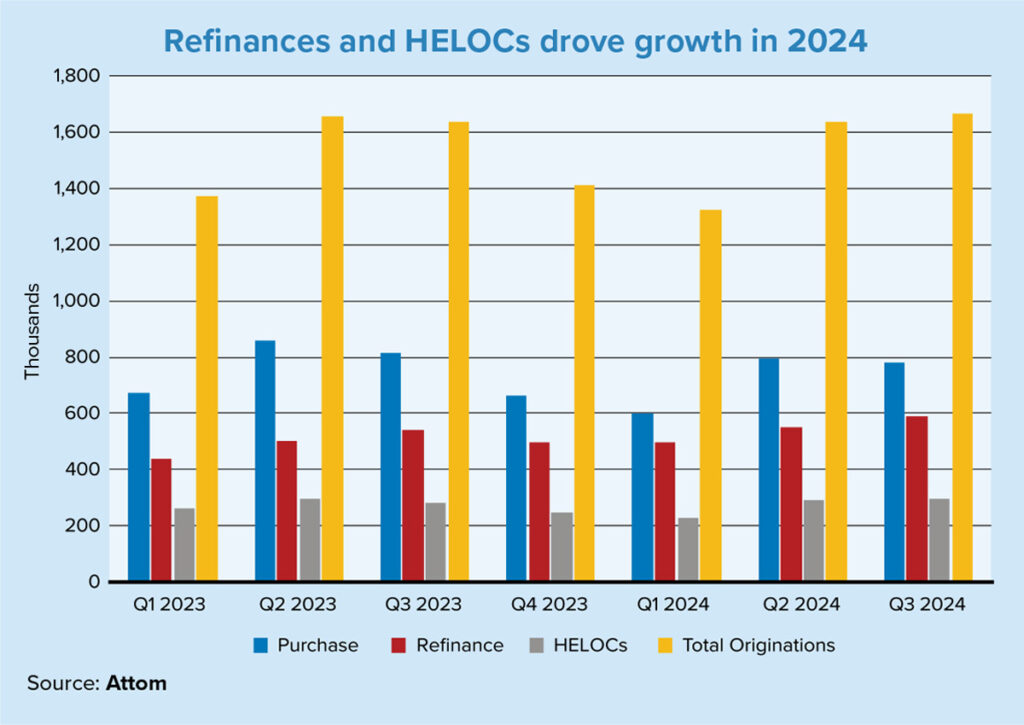

The total number of residential mortgage originations increased in third-quarter 2024, marking the second straight quarterly gain for the first time in three years, according to Attom’s U.S. Residential Property Mortgage Origination Report. Although the second quarter saw a significant leap of nearly 25%, third-quarter gains were more modest, coming in at just 1.9% higher than the previous quarter. Despite the gains, residential mortgage originations remain down nearly 60% from the high hit in first-quarter 2021 (when interest rates hovered around 3%).

Refinances and home-equity loans were the forces driving the growth in originations in the third quarter, as homeowners took advantage of the recent downward trend in mortgage rates, which dropped close to 6% by the end of third-quarter 2024. Purchase loans declined in the quarter, although they still made up more than half of all residential originations. Despite dropping a full percentage point in the quarter, the decrease in interest rates couldn’t overcome the challenges facing homebuyers in this market: high home prices and some of the lowest supply levels seen in 10 years.

In third-quarter 2024, there were 1.67 million mortgages issued in the U.S. for residential property (one to four units). Those mortgages represented roughly $550 billion in lending, up 2.9% in dollar value from the previous quarter and up 6.6% from third-quarter 2023. In the period, roughly 588,000 originations were refinances, representing a 6.9% quarter-over-quarter gain, and home-equity originations totaled 297,000, a 2.3% quarterly gain. Purchase originations hit 782,000, a 1.7% decline from the previous quarter, a trend which reflects both the tight supply numbers as well as the typical slowdown in sales seen in the latter half of the year.

The uptick in refinances represents a bright spot for the mortgage industry, since the third-quarter 2024 originations stand out as the most refinances seen since third-quarter 2022. The spike in interest rates in 2021 and 2022 saw refinance originations drop a whopping 80%, and recent increases may signal steps toward recovery in this area — providing interest rates don’t spike again. Refinances increased across the U.S., with quarterly activity up in 75.8% of the metro areas analyzed in the report.

Continuing to look at the data on a more local level, most metropolitan areas in the U.S. saw gains in overall originations similar to the national average. Originations increased quarterly and annually in 60.4% of the 207 metropolitan areas covered by the report (those with a population of at least 200,000 and at least 1,000 total residential mortgages issued in the quarter). The largest total residential lending increases quarter-over-quarter were seen in: Anchorage, Alaska (up 78.6%); Yuma, Arizona (33.3%); Ann Arbor, Michigan (33%); Huntington, West Virginia (21%); and Trenton, New Jersey (20.5%). Looking at just the larger metropolitan areas (with a population of at least 1 million), the biggest quarterly increases were seen in: Rochester, New York (up 20.1%); Detroit, Michigan (14.7%); Grand Rapids, Michigan (13.5%); San Diego, California (13.2%); and Hartford, Connecticut (12.7%).

On the other side of the trend, several metro areas saw quarterly declines in overall residential lending. The areas with the largest losses in lending include: Boulder, Colorado (down 44.3%); St. Louis, Missouri (-36.5%); Jackson, Mississippi (-25.2%); Myrtle Beach, South Carolina (-20.4%); and Springfield, Missouri (-19.4%).

In terms of refinance activity, the local data shows the largest quarterly increases in: Anchorage, Alaska (refinances up 59.1%); Ann Arbor, Michigan (46.9%); Vallejo, California (46.7%); Colorado Springs, Colorado (42.4%); and Charlottesville, Virginia (41.7%). In metro areas with a population of at least 1 million, the largest quarterly refinance activity increases were seen in: San Jose, California (up 28.7%); Milwaukee, Wisconsin (27.4%); San Diego (27.2%); Richmond, Virginia (24.4%); and Los Angeles (24%).

Drilling down into the loan composition data further, mortgages backed by the Federal Housing Administration made up 13.8% of all residential property loans this past third quarter, the same figure seen in second-quarter 2024, but down from the 15.1% seen in third-quarter 2023. Loans backed by the U.S. Department of Veterans Affairs made up 5.9% of overall residential originations in third-quarter 2024, an increase from the 5% seen in the second quarter and from the 4.8% seen in third-quarter 2023.

Despite the decrease in purchase loans, the overall residential origination numbers indicate some positive trends for the industry. But much of what happens next will depend greatly on interest rates; if rates dip further, both refinances and purchase originations should continue to improve.