Brick-and-mortar retail is under siege from e-commerce — an ongoing trend over the past few years that has been accelerated by the COVID-19 pandemic. E-commerce as a share of all U.S. retail sales is now at 14%, up 300 basis points from its level at the end of 2019.

The transition to e-commerce dates to the early days of the new millennium, and its share of all sales is likely to exceed 20% within the next few years. Amazon has led this shift, but many big-box stores and even niche retailers have made their online footprint a priority in recent years.

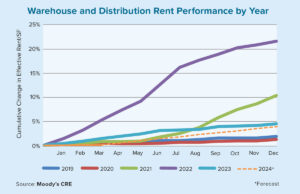

This has had two major impacts on U.S. commercial real estate. First, a record level of new supply in the distribution and warehouse space is needed to satisfy consumer desires for faster shipping. Second, there is a decline in retail construction along with a slow but steady increase in the retail vacancy rate.

With this in mind, however, not all retail subsectors or properties are realizing the same fate. At the same time that a flurry of department-store closures puts pressure on Class B and C malls, modern amenity-filled spaces located in wealthier submarkets have held quite steady. Preliminary data and anecdotes support the excitement of shoppers to return to these spaces as the pandemic subsides.

A similar story holds true for grocery-anchored community and neighborhood retail centers. Grocery stores have proved resistant to the pandemic and somewhat resistant to e-commerce. As of today, even if large swaths of consumers become more comfortable with online grocery shopping (a big assumption), the perishable nature of food and the desire for “instant” delivery will help prop up these well-located retail centers.

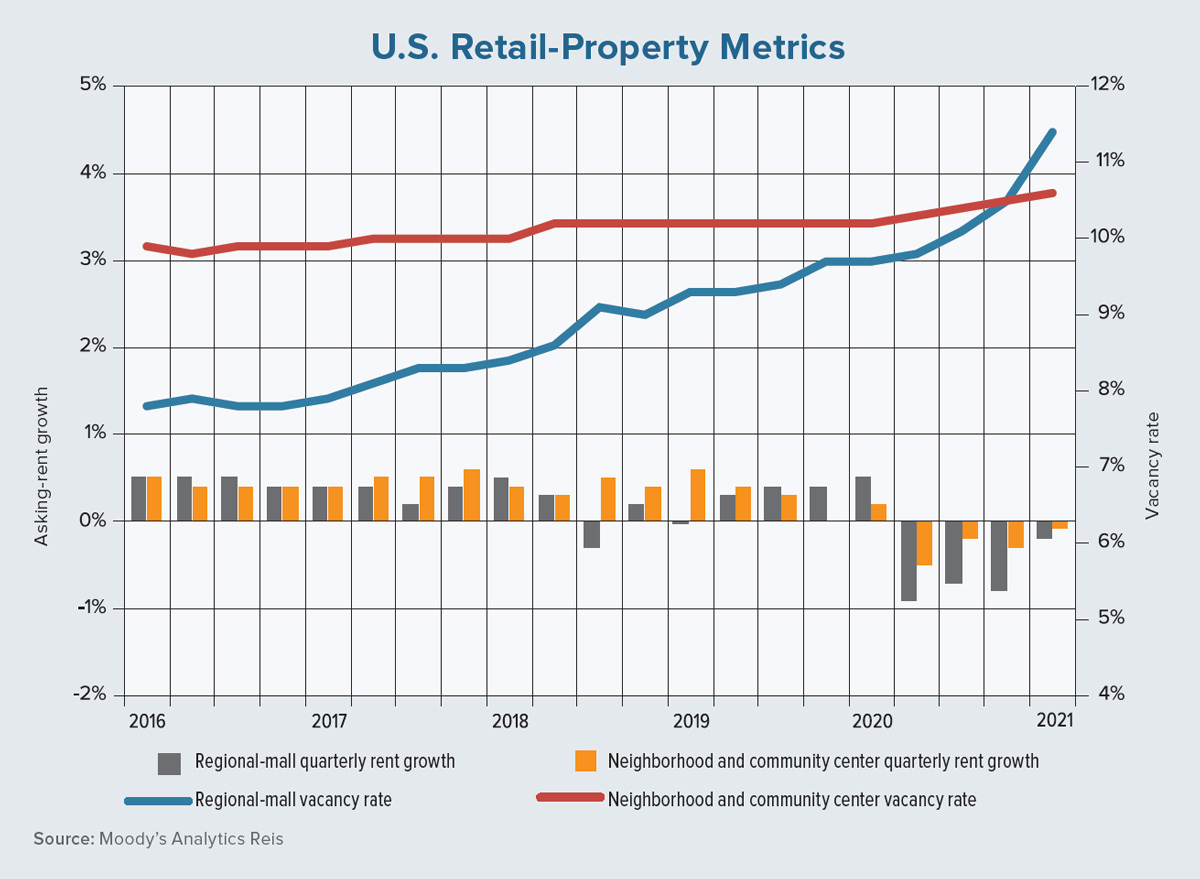

So, how are these factors playing out in national retail data and forecasts? At 11.4%, the nationwide vacancy rate for regional malls is now at its highest rate since Moody’s Analytics Reis began capturing this data more than 20 years ago. As shown on the accompanying chart, the vacancy rate began rising long before the pandemic. This supports the argument of an evolutionary change and not simply a COVID-related change, although a recent acceleration of vacancies is noted.

Not all malls are created equal. By digging deeper into the data, we have found that much of the vacancy increase is due to stress in Class B and C properties. The trends for neighborhood and community shopping centers, however, are quite different. Although the annualized vacancy rate for these properties increased by 40 basis points in first-quarter 2021, it has stayed relatively flat since 2016, while the year-over-year rent decline of 1.1% at this time was modest.

From 2016 through 2019, asking-rent growth across all retail assets averaged 1.7% per year. Moving forward, even though employment and retail sales will rebound nicely in 2021, retail properties are not completely out of the woods. History shows us that the sector faces a recessionary lag in stress due to the long lease terms for these assets. Given that, it is possible that rents will drop another 3% to 6% this year before rebounding in 2022.

Interestingly, there is no strong regional element to this story. The metro areas at the top and the bottom of the list for effective rent growth in retail tend to be missing a common thread. This is at odds with the multifamily, office and industrial sectors, where on average there is a bit more growth (or fewer declines) in the South Atlantic and Southwest regions.

The nuance for retail occurs at the submarket and property level. Across all metro areas, about 20% of retail properties are classified as “troubled.” Older retail clusters, typically those in less-affluent submarkets, are facing stress while larger and more modern “destination” clusters are pulling consumers in. This was the emerging pattern prior to the pandemic. Even with the acceleration of e-commerce, the destination-type facility will likely have the critical mass of customers to remain successful.

In summary, using a broad brush to paint the retail picture leaves out necessary detail. To understand the evolution of retail, a more granular analysis is required. Location, tenant mix and property style are vital for forecasting future success or failure. And there are both opportunities and risks in this sector regardless of the overall metro-level trend. ●