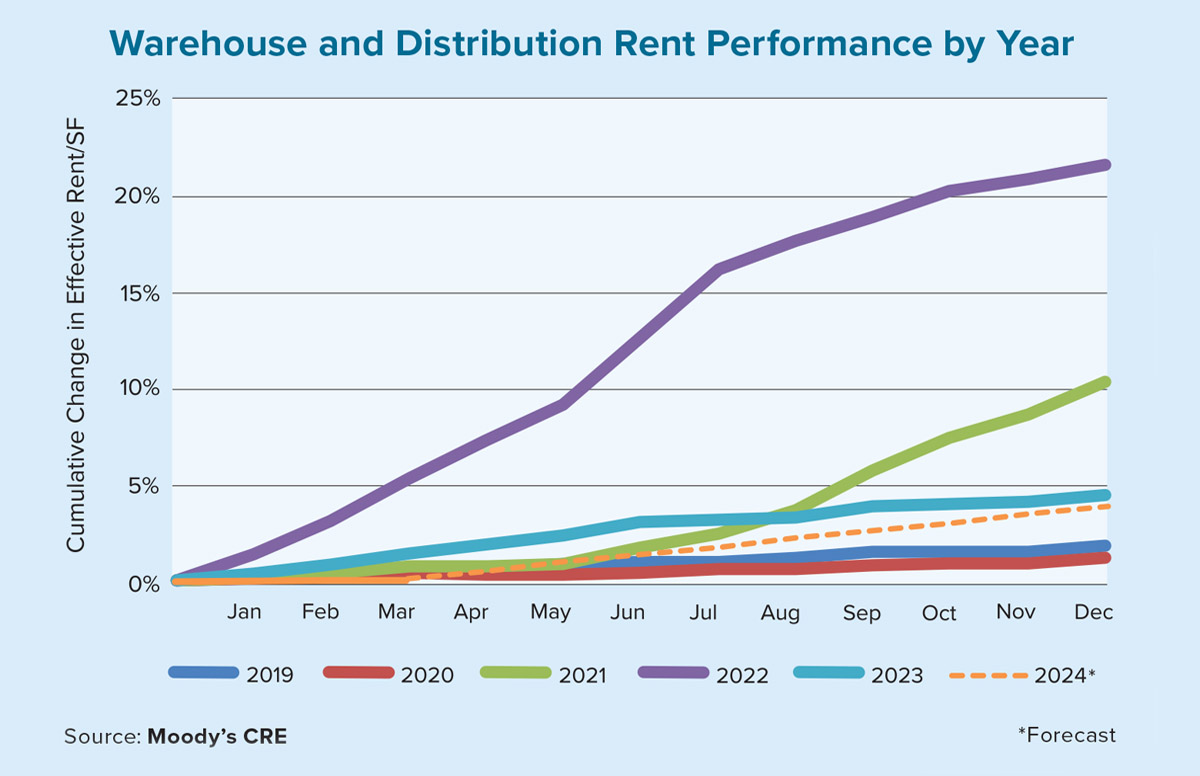

After several years of extraordinary growth, the industrial sector’s moonshot performance has started to come back down to Earth. Rent growth has cooled considerably in recent years, as illustrated in the accompanying chart.

For example, commercial real estate effective rent growth for warehouse and distribution properties in 2022 increased by 21.7% annually, according to Moody’s Analytics. Construction in 2023 ramped up to about 275 million square feet, which helped hold down rent growth to a still-solid 4.8%. Over the first three months of 2024, however, the vacancy rate ticked up another 20 basis points (bps) to 6% and effective rents — which represent the uniform rental amount for each period throughout a lease term — have only risen by 30 bps. Despite the year’s slow first quarter, Moody’s expects effective rents for these properties to increase by about 4% annually in 2024, which implies a trendline just below that of 2023. Such growth is nowhere near the blistering pace set just a few years ago.

Among Moody’s five U.S. regions, the Western Region was the only one to have negative net absorption in the first quarter of this year. Additionally, the Western Region saw its vacancy rate rise the most — by 60 bps to 5.8% — and was the only region to see effective rents decline, falling by 30 bps. Conversely, the Southern Atlantic Region, which has recently been experiencing arguably the best performance of any area, had the second lowest vacancy rate at 5%, while effective rent growth increased the most at 0.8%. The Midwestern, Northeastern and Southwestern regions all had positive net absorption rates and practically unchanged vacancy rates for the quarter. The Midwestern Region had a vacancy rate of 6.2%, The Northeastern Region registered a 4.8% vacancy rate, and the Southwestern Region had an 8.9% vacancy rate.

Among the 47 primary metropolitan areas tracked by Moody’s, two of the top-three cities in rent increases were, not surprisingly, in the Southeast. The cities experiencing the largest warehouse and distribution rent increases were Jacksonville, Florida, which saw quarterly effective rents jump 1.14%; Atlanta, with an effective rise in rents of 1.13%, and Sacramento, with an increase of 0.39%. Only four of the 47 metros reported declining effective rents. Interestingly, three of those four metros were located in California. The largest decline was experienced by Los Angeles (-0.96%), followed by San Bernardino/Riverside (-0.80%), St. Louis (-0.39%) and Orange County (-0.10%).

While there are rent gains in various regions and metro areas, the overall trend of decelerating performance has nonetheless been happening across the nation. It’s likely headwinds will continue to occur for the sector throughout the remainder of 2024, especially as geopolitical risks remain front and center. Ongoing Houthi attacks on containerships in the Red Sea/Suez Canal as well as the severe drought affecting water levels on the Panama Canal have increased shipping costs for businesses and have increased the difficulty of mitigating supply chain disruptions.

Consequently, in the near term, space market dynamics are likely to soften from logistical delays. There will also be pressures from above-average supply growth — albeit this too has been moderating recently.

The long-term prospects for the industrial sector, however, appear to remain bright. Despite geopolitical troubles, new suppliers, possible substitute components, alternative routes and increasing transportation options will be identified. This should allow inventories to build back up, which will bolster the needs of businesses for industrial real estate space. In short, the industrial sector remains a darling of commercial real estate, but its performance is no longer in the heavens. ●