A combination of sturdy space-market fundamentals, a rosy outlook and uncertainty elsewhere in the commercial- property sector has led to increased investor enthusiasm for industrial real estate.

Although capital-market and development activity plummeted this past year for most other property types, industrial investors showed a greater willingness to move forward with acquisitions and construction projects. Capitalization rates fell to recent historic lows while completions in 2020 surpassed pre-pandemic expectations. Looking forward to the final three quarters of this year and beyond, both space- and capital-market fundamentals will remain strong for the industrial segment.

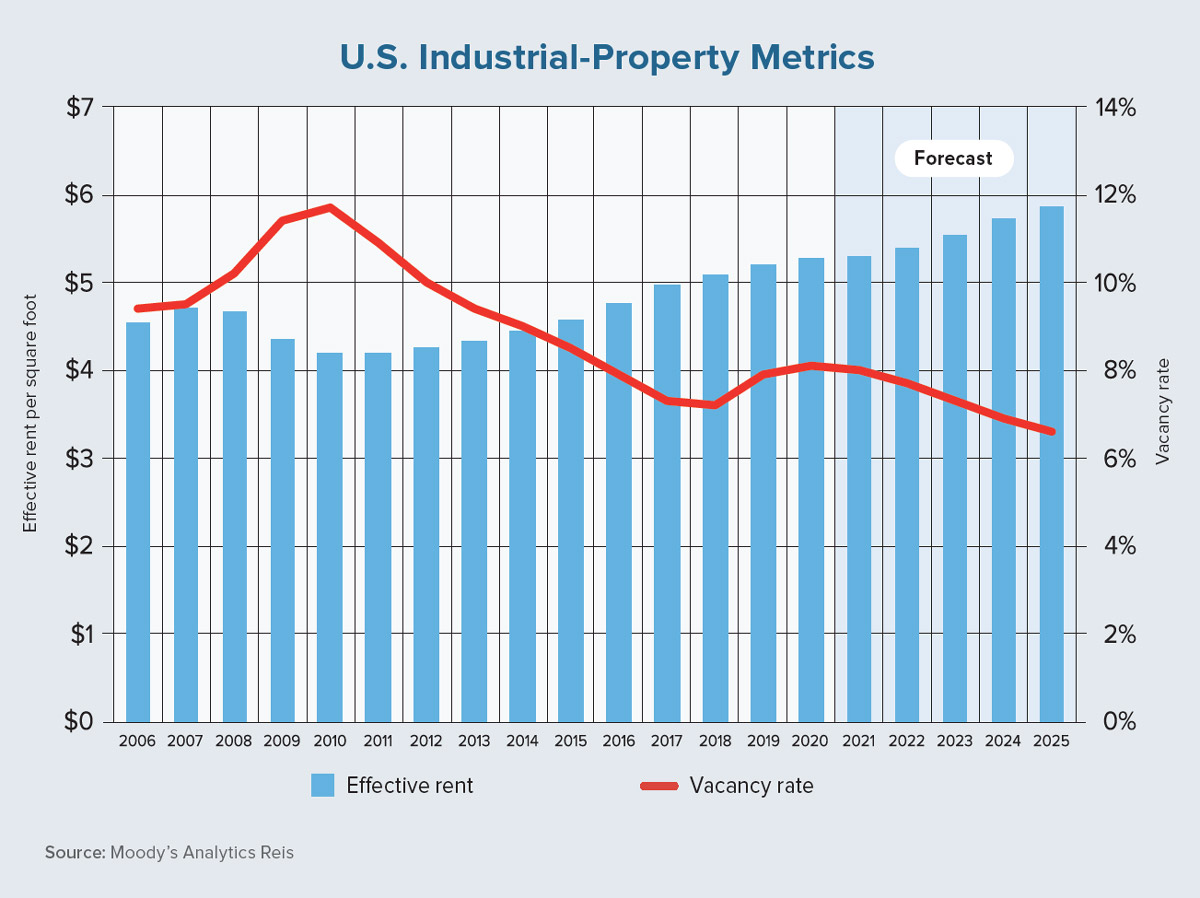

In the midst of an economic recession where the U.S. unemployment rate spiked to nearly 15% — and even during the recent rebound where more than 10 million people were still out of work this past January — the resilience exhibited by industrial real estate is remarkable. Over the course of 2020, industrial asking rents and effective rents each increased by 1.3% while the nationwide vacancy rate of 8.1% was only 20 basis points (bps) higher than the 2019 level, according to Moody’s Analytics Reis data.

This performance dramatically outpaced all other commercial real estate sectors. And for reference, the Great Recession induced an aggregate vacancy-rate increase of about 200 bps for U.S. industrial properties.

The contrasting nature of outcomes for industrial properties against their commercial- asset counterparts, as well as the industrial sector’s own historic relationship with recessions, emphasizes the unique quality of a pandemic-induced downturn in a digital age. Without the ability for people to explore an expanded e-commerce universe, consumer spending would have faced greater peril and the industrial sector would have undoubtably fared worse.

Also, consider the additional warehouse and distribution space required for e-commerce versus traditional brick-and-mortar retail activities. Our estimates show that e-commerce requires about three times as much space to generate the same revenues. With these factors in mind, the rationale for industrial-sector success becomes clear.

Transaction activity for the industrial sector slowed due to the COVID-19 pandemic and subsequent stay-at-home orders but much less so than other commercial real estate sectors. While year-end deal- and dollar-volume declines ranged from 40% to 60% for much of the U.S. commercial-property market, the annualized declines for industrial were only 15%.

Even more eye-catching, the median sales price for an industrial property increased from $126 to $150 per square feet, and cap rates plummeted to slightly less than 6%, about 130 bps lower than their five-year average.

Prior to the pandemic, e-commerce accounted for about 12% of all retail sales. We expect this share to increase to the range of 15% to 20%. The metaphorical bandage has been ripped off. Some consumers may fully go back to their old ways, but many have likely found that purchasing certain products via the internet and the comfort of their own home is efficient and satisfying.

This structural shift, combined with our bullish macroeconomic forecast of nearly 5% gross domestic product growth in each of the next two years, make for a bright outlook for the industrial sector. We now expect industrial rent growth to average more than 2% per year through 2025, while vacancy rates are on a slow and steady path toward 5% by decade’s end (the current rate is 8.1%).

The race to providing customers with goods in hours rather than days will prioritize space in population centers. New construction and conversions of older space are at the top of the agenda for logistics specialists. Locations with solid infrastructure, which allow for quick access to large swaths of the population, will be in high demand going forward. ●