Higher interest rates and an uncertain economic environment are beginning to weigh on the commercial real estate and mortgage industries. Origination activity plummeted during second-half 2022 as costly financing reduced buyer interest, and while rent levels have yet to show much evidence of widespread declines, rent growth has slowed substantially. As we begin a new year with plenty of headwinds, what’s in store for commercial real estate?

The direction of inflation and Federal Reserve monetary policy will play significant roles in answering this question. If inflation remains stubbornly high due to a reemergence of supply chain issues or geopolitical tensions, this will prompt continued benchmark rate increases in the early portion of 2023. On the other hand, some supply-side luck and reduced consumer spending would likely mark the end of the Fed’s rate hikes, potentially leading to the much-discussed “soft landing” in which the U.S. avoids a recession.

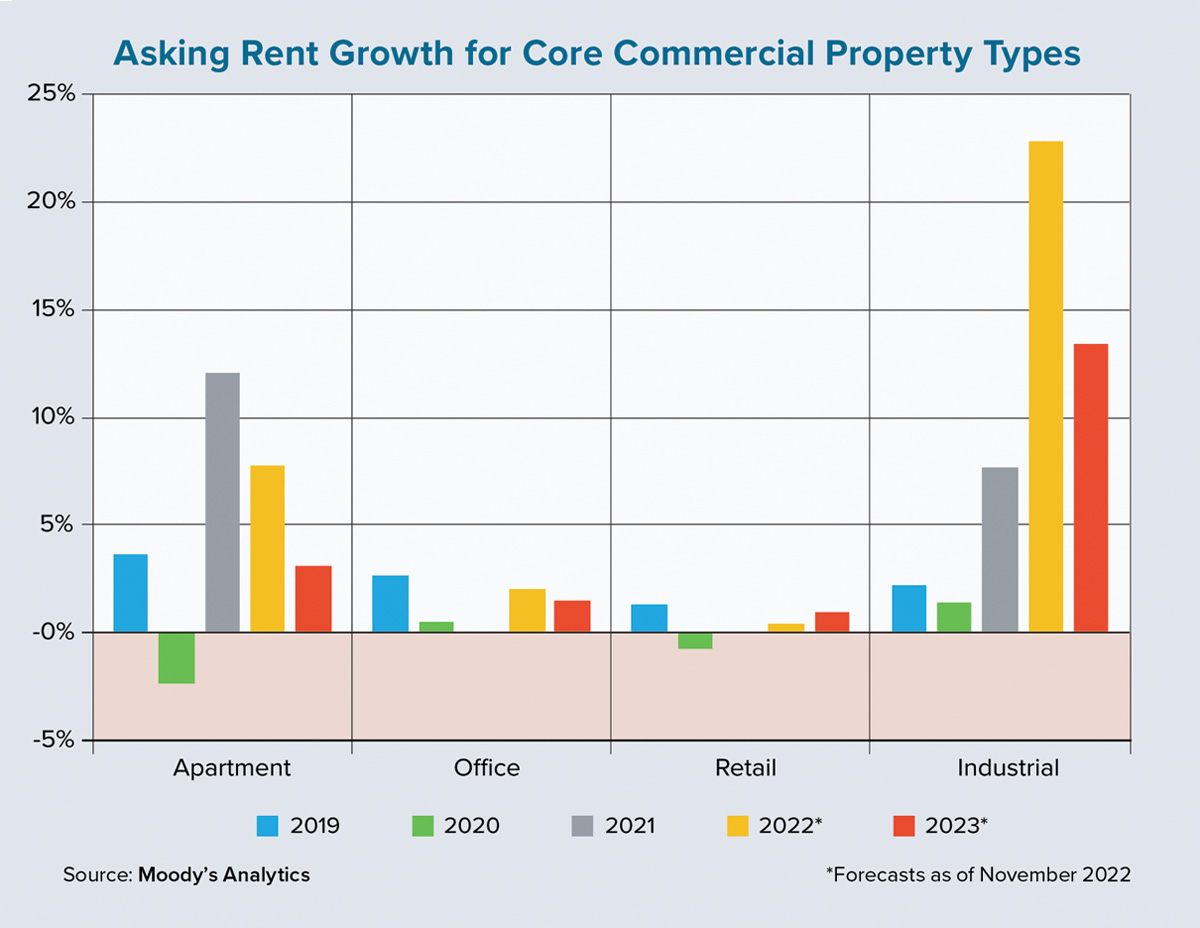

The Moody’s Analytics baseline forecast for 2023 anticipates real gross domestic product (GDP) growth of approximately 1% for the year. Unemployment is expected to grow by half a percentage point and crest at 4% by year’s end, while the 10-year Treasury rate should peak at 4.6% in second-quarter 2023 before slowly receding thereafter. As shown on the accompanying chart, this macroeconomic environment would lead to yearly rent growth across the major commercial property types that is slightly below 2019 figures but within the range of what we consider “normalized.”

The industrial sector (warehouses and distribution centers) is an exception. This sector has a runway for one more above-average year as long-term momentum caused by structural shifts in the economy is strong enough to compensate for slightly below-average economic performance. Continued growth in e-commerce, reshoring of manufacturing facilities and adjustments to the global logistics network will combine to push the industrial sector to a new and higher long-term equilibrium.

What about the other core sectors? The housing shortage and single-family recession will keep multifamily afloat. In the past, it has taken a significant hit to wages or employment to severely affect apartment rents. As for office and retail, each will continue their longer-term evolutions, which will result in a wide distribution of market- and property-level outcomes. In short, strong performers will slightly outweigh weak ones, causing national-level performance to remain slightly positive.

But what if this economic scenario is too optimistic? What happens to commercial real estate if the U.S. economy falls into a deep recession or — potentially worse — a stagflationary environment? Historic evidence supports a much more significant struggle for the industry in these situations.

Stagflation (high inflation, rising unemployment and slow economic growth) was previously caused by negative supply-side shocks. A spike in energy prices due to geopolitical tensions will continue to be a risk in 2023. If that were to occur in the near future, the Fed’s playbook calls for an even higher interest rate environment, which would potentially result in years of sluggish economic performance. A significant near-term decline in real GDP (without a full recovery until 2025 or 2026) would be likely.

Although the probability of stagflation is relatively low, this wild card would be quite problematic for commercial real estate. All core sectors would take a hit as this scenario would overwhelm even the long-term positive trends for industrial properties.

In summation, commercial real estate has shown greater resilience to economic slowdowns compared to other asset classes, and the U.S. economy remains a safe haven for global investors. This is expected to continue in the scenario of sluggish economic growth (which remains our baseline domestic forecast), but there are significant risks of a deeper recession or stagflationary environment. Either of these would lead to greater difficulties for the commercial mortgage industry. ●