Those with a vested interest in the multifamily-housing sector tend to pay particular attention to young people and where they are moving. But the statistics associated with this demographic only partially support the claim that the apartment market moves in step with millennial population growth.

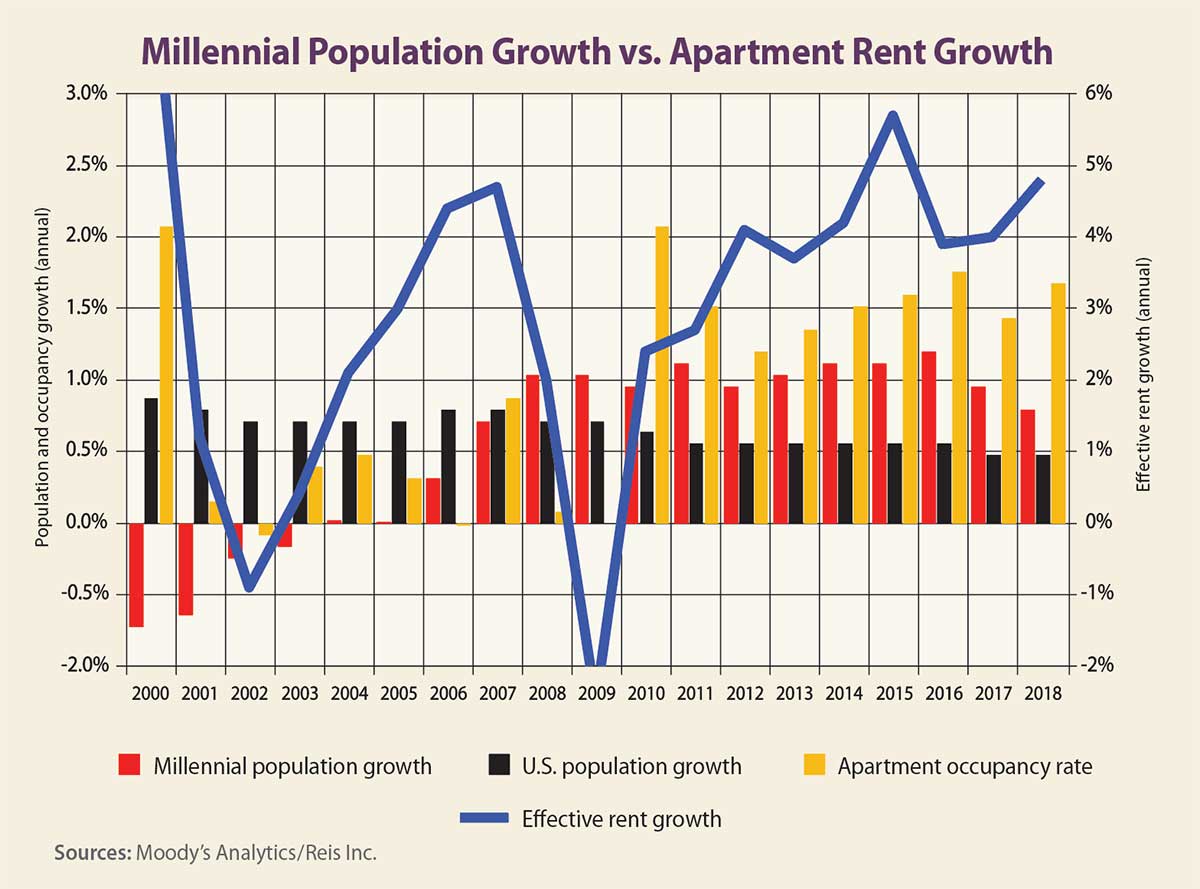

Indeed, the chart on this page shows how apartment occupancy growth has held steady throughout the last nine years, in line with millennial population growth. Yet this age group’s population growth slowed in 2017 and 2018, while occupancy growth accelerated in 2018. With rent growth, however, the story is less compelling as rent increases and decreases correlated more closely to the overall economic trend, even when the millennial segment of population growth was healthier.

Oddly, the correlation between apartment occupancy growth and population growth for the millennial set is 38%, yet this age group’s population-growth correlation with effective rent growth is 67%. That said, the caveat of correlation rather than causation is true in this case, as the shifts in the housing market also have affected rent growth as much as the changing demographics have.

While the macroeconomic story is easy to tell, the microeconomic (or metro-level) picture is quite different. In fact, the metro areas that saw the highest population growth of 25- to 34-year-olds were not what one would expect. That is, many might assume that the metros with the highest population growth are tech-focused markets on or near the coasts, such as San Francisco, Seattle, New York and Boston. Indeed, these metros saw some of the highest rent growth. But only Seattle cracked the top 10 in terms of millennial population growth, increasing 16.5% from 2013 to 2018, which was second only behind Orlando, Florida.

Other primary metros with the highest population growth rates for 25- to 34-year-olds are Austin, Texas; Charlotte, North Carolina; Colorado Springs, Colorado; Tampa, Florida; and Raleigh-Durham, North Carolina. The average annual apartment rent growth rates from 2013 to 2018 for these metros ranged from 5% (Raleigh-Durham) to 10.4% (Seattle). The correlation of rent growth and population growth for primary metro areas was 60%.

A more interesting story lies in the tertiary metros in which population growth of the millennial segment was quite high. These metros include Lakeland, Florida; Bend, Oregon; College Station, Texas; the Colorado cities of Greeley and Fort Collins; and the Washington cities of Bremerton and Bellingham. Each of these metros had population growth of 16% or more among the millennial set from 2013 to 2018.

Bend and Greeley saw high average rent growth of 9.2% and 7.1%, respectively, from 2014 through 2018. But the other tertiary metros mentioned averaged rent growth that was near to or below the U.S. average of 5.2% — ranging from College Station (2.6%) at the low end to Bremerton (6.1%) at the high end. In fact, the correlation between population growth of 25- to-34-year-olds and rent growth was only 57% for the tertiary metros.

At the other end of the spectrum, three primary metros saw population declines among millennials: Milwaukee, Chicago and Fairfield County, Connecticut. Yet rent growth for all three metros was positive, ranging from 2.6% in Fairfield County to 4.8% in Chicago. Likewise, 28 tertiary metros saw millennial population declines, led by the West Virginia cities of Charleston and Huntington; the Illinois cities of Peoria, Springfield and Davenport; Lawton, Oklahoma; and Vineland, New Jersey. Most of these metros saw overall population declines during this five-year period, but all of them had positive (although relatively low) average rent growth.

Looking to the future, a few metros show sharp population growth in the 25- to 29-year-old age group, including Greenville, South Carolina; Nashville, Tennessee; and Detroit. Rent growth in Nashville also has been robust, averaging 7.3% over the past five years, but other cities have seen rents grow at rates close to the national average. Will this change in the coming years? We’ll check back with another report in the near future.