The aftermath of the COVID-19 pandemic is not the first time that the importance of the office has been questioned. In the latter half of the 20th century, business leaders and economists debated the merit of a meeting place full of cubicles and 9-to-5 workers. During an era of high-speed computing and rapidly improving communication technology, it was thought that offices would become obsolete and drag cities down with them.

As we now know, the exact opposite occurred. Technological advances helped to build a more global economy and allowed U.S. companies to offshore simple manufacturing tasks, which freed up vast amounts of highly skilled labor. America was focusing on what economists refer to as a comparative advantage, in which goods and services could be produced at a lower opportunity cost. This process ultimately helped the country to became a global center of knowledge creation — and the office became its castle.

Why has the office been so important to knowledge creation? The term “agglomeration” is at the root of this answer. Agglomeration generally refers to gains made through proximity. These gains can be borne by employers and/or employees, and proximity can refer to either a single office setting or an entire metropolitan area. Prime examples include tech startups in Silicon Valley and auto manufacturers in Detroit. The two main themes of agglomeration refer to the matching of skills and jobs, as well as informal information exchanges. Proximity tends to increase the likelihood that both of these things occur, which in turn increases productivity and innovation.

Does any of this still matter given the relatively solid performance that many knowledge-based companies have had during this great remote-work experiment? In other words, have the most recent tech advances proven effective enough to finally make the office obsolete? While various surveys and anecdotes suggest that managers are somewhat satisfied with the shift to remote work — with some companies even announcing their intentions to allow employees to remain remote indefinitely — the jury is still out in terms of the longer-term effects of remote work on innovation.

Without the ability to have moments of unscripted illumination that result from bumping into a co-worker at the office, some brilliant ideas are likely to be lost in empty space or, at a minimum, they may take longer to form. It is this line of thinking, along with fears that the gung-ho attitude displayed by many workers over the past 18 months will lose steam, that has prompted some companies to maintain office leases and push discussions about a fully remote-work environment down the line.

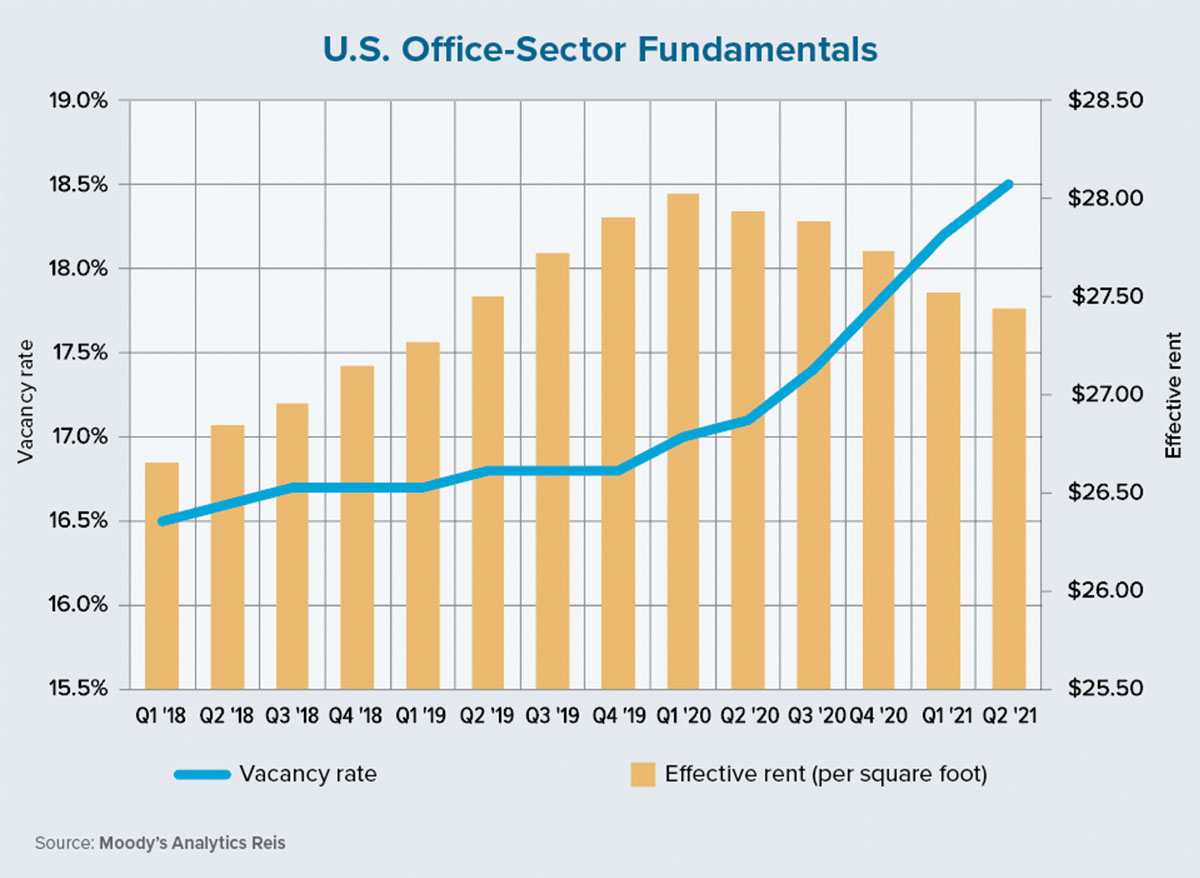

These fears and uncertainties among business leaders, in addition to projected job growth, has helped to prop up commercial real estate fundamentals for the office sector. As the chart on this page shows, a bit of distress has been recognized in the vacancy rates over the past few quarters, but rent declines (which amount to about 2% in relation to year-end 2019) have so far been modest.

Furthermore, distressed pricing of office assets are nonexistent at present. The Moody’s Analytics Commercial Real Estate Price Index reported an increase in value of about 2.5% from fourth-quarter 2019 through second-quarter 2021. The combination of modest rent declines and positive growth in values gives us reason to believe that property owners and investors are still bullish on the long-term prospects for the office.

None of this is to say that the office does not have any struggles ahead. It is likely that we will notice some pain over the short and intermediate term as companies test out various remote-work policies, in addition to some migratory or demographic shifts that lead to geographic-performance variations. Most importantly, however, the market is not telling us that the end of the office is coming anytime soon. ●