Amid signs of a slowing labor market and confidence that inflation is moving back toward policy objectives, the Federal Reserve opted for an interest rate cut of 0.5% in September. Unlike previous cycles where the Fed lowered rates due to economic weakness, the U.S. economy is currently strong, with the real domestic product for the second quarter of 2024 expanding at an annualized rate of 3.0%.

Consumers have been more resilient than expected. In turn, they have helped propel the economy forward. But just how much further this dynamic continues remains to be seen. Obviously, a more accommodative Fed and lower energy prices of late will provide marginal relief for consumers. Households are nowhere near as flush with cash, however, compared to the early days of the pandemic when the federal government provided a massive stimulus response. For example, the Federal Reserve Bank of San Francisco estimated in a recent blog that after peaking at $2.1 trillion in August 2021, cumulative pandemic-era excess savings have already been depleted. As of August, America’s cumulative aggregate savings had declined to approximately -$216 billion.

In spite of consumers running through their savings, there are reasons to expect that recent robust spending patterns will continue. This trend bodes well for the health of the hospitality industry. On aggregate, the net worth of U.S. households has risen, thanks in large part to rising home prices and stock market gains. For instance, according to the Federal Reserve’s Survey of Consumer Finances, between 2019 and 2022 the real median U.S. family net worth surged by 37% to $192,900, which was the largest three-year worth increase since 1989 — and more than double the next-largest value surge during the past 35 years. Moreover, non-financial assets such as real estate holdings and vehicles are higher relative to pre-pandemic levels, another sign of increased wealth.

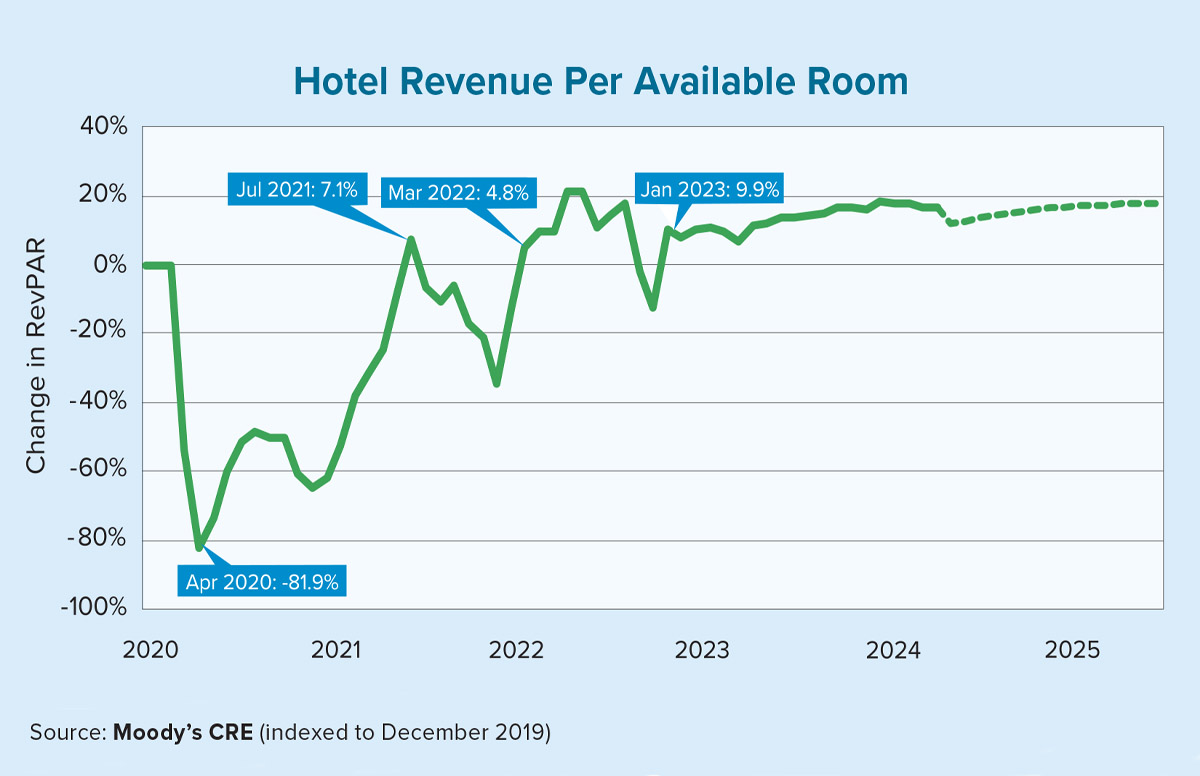

As for the hotel sector, Moody’s Analytics data indicates that the annual change in revenue per available room, also known as RevPAR — a function of occupancy multiplied by the average daily room rate — increased by approximately 123% in 2021. While a resounding number, the popular industry measurement declined by nearly 65% the year before, thus providing an inflated comparison. While 2023 growth in revenue per available room was just north of 30%, Moody’s forecasts 2024 will see little change (down 44 basis points), before increasing slightly in 2025 in the range of high 2% to low 3%. As illustrated in the accompanying chart, the hotel sector suffered a nearly 82% decline in revenue per available room in April 2020. The industry temporarily recouped this drawdown in July 2021, and then again in March 2022. It wasn’t until January 2023 that hotels were consistently above pre-pandemic levels. While not illustrated in the chart, higher room rates have been the driving force behind the revenue growth in the sense that occupancy as of August 2024 was about 150-basis points lower — at 64.5% — than year-end 2019 figures.

Overall, revenue per available room increased at a compound average growth rate of 3.4% from December 2019 to August 2024. Among the 69 metropolitan areas in which Moody’s Analytics tracks hotel data, the top 10 saw average increases of 42.8% during that period, which translates into an annual growth rate of 7.8%. The bottom 10 metros, however, saw a cumulative rate of -9.6%, on average, representing a compound annual growth rate of -2.3%. Las Vegas was the top performing market, with an annual growth rate of 14.8%, while San Francisco fared the worst with an annual growth rate of -7.9%. With a more favorable macroeconomic backdrop, expect consumer spending patterns to support modest growth in the hospitality sector over the near term. As is always the case in real estate, location matters and performance is nuanced.