While the industrial sector often gets the most recognition for being a pandemic-era darling, the self-storage industry has also enjoyed the benefits from changes in socioeconomic conditions that have bolstered demand for flexible storage solutions. As the pandemic took effect in early 2020, lockdowns and social distancing measures constrained consumers’ ability to spend money on service-oriented activities. Instead, after paying for the basics, such as one’s housing, utilities and food, government stimulus checks along with any personal savings were increasingly spent on goods – such as home appliances, new furniture and the latest technology equipment for upgrading a home office.

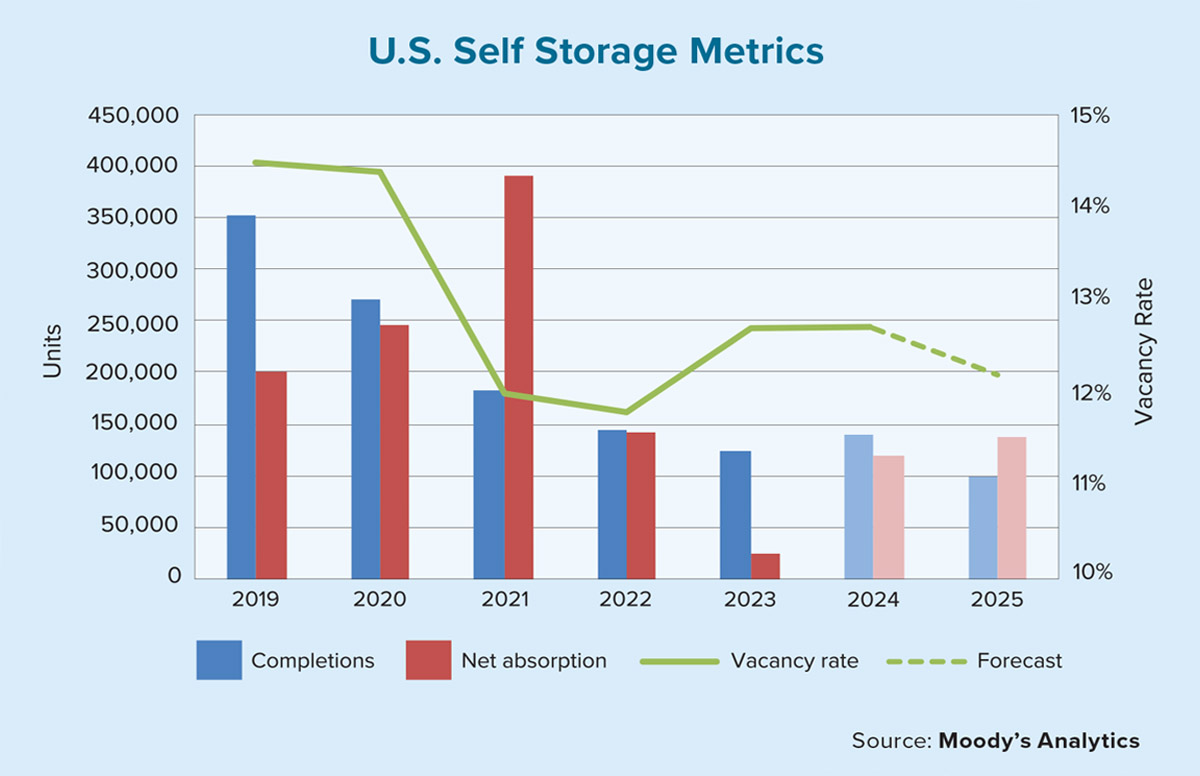

As households accumulated more goods, the self-storage industry boomed. In 2021, for example, net absorption was near a record high for the past decade at just under 400,000 self-storage units. Since then, the sector’s absorption has dramatically slowed and supply growth has greatly moderated over the past several years from approximately 350,000 units in 2019 to 125,000 units in 2023.

Consequently, from year-end 2019 to the first quarter of 2024, the sector’s vacancy rate declined by 150 basis points (bps) to 13%. Still, the vacancy rate was 260-bps above its pandemic low of 10.4% from the second quarter of 2022, mostly due to a low level of absorption in 2023.

Across the nation, the Southwestern, Southern Atlantic and Midwestern regions reported the largest vacancy rate declines over this roughly four-year period at 330-bps, 210-bps, and 210-bps, respectively. Conversely, the Northeastern and Western regions reported minimal declines at 60-bps and 40-bps. These trends coincide with general migration patterns from more expensive metros such as New York and Los Angeles to areas in the South with a lower cost of living, more favorable business and tax policies, and of course, warmer weather.

Moreover, since 2019, asking rents for 10×10 storage units increased by a compound annual growth rate (CAGR) of 2.5% for non-climate-controlled units (NCC) and 2.4% for climate-controlled (CC) units. In 2021, for example, asking rent growth was a resounding 12.3% annually for NCC units and 14.5% for CC units. Contrasting back to the industrial sector, asking rents for warehouse and distribution properties increased by a compound annual growth rate of 8% over this same period.

So it is understandable why the industrial sector’s strength is more frequently touted. It is also worth noting that completions of storage units significantly outpaced net absorption in 2023. The result being that asking rents for NCC units decreased by 2.5% annually, and CC units fell by 3.4% annually. Thus, despite the down year in 2023, rent stability has remained relatively strong, given the circumstances.

During the first quarter of this year, the self-storage industry was off to a slow start, with a vacancy rate, as mentioned earlier, rising by 30-bps to 13%. However, the first three months and the final three months of the year typically have slower leasing activity. It is the second and third quarters (especially May, June and July) that usually are busier. This timeframe coincides with the academic calendar and the spring home buying season when more families are generally looking to move. Notwithstanding the seasonal patterns associated with the sector, Moody’s Analytics forecasts that the vacancy rate at the end 2024 will be in the mid- to high-12% range. In 2025, we expect the vacancy rate to end the year in the low-12% range. There is no doubt the pandemic-related surge in the self-storage sector is in the rear-view mirror. Over the next 12 to 18 months, we are likely to see the sector stabilize toward a new equilibrium in tandem with the gradual cooling of the labor market.