Due to e-commerce competition and changing consumer preferences, retail-property assets have faced increasing stress long before the COVID-19 pandemic arrived. But while many thought that the onset of pandemic-related restrictions would mark a true beginning of the end for brick-and-mortar retail, this simply has not been the case.

E-commerce as a share of all U.S. retail sales inevitably skyrocketed between the first and second quarters of 2020, going from 11.4% to a historic high of 15.7%. But since its peak, this metric has steadily declined and reached 12.9% in Q4 2021, census figures show. In an apparent reversion to their original growth path, e-commerce sales (while still growing) indicate a continued consumer desire to make in-person purchases.

Another sign of lukewarm promise for retail real estate is the growth path of all retail sales activities. In the decade following the Great Recession, retail sales climbed steadily before crashing at the onset of the pandemic. Nonetheless, the growth of this metric quickly rebounded and has continued to trend upward.

The steady rise of inflation over the past year and a half is likely a partial contributor to the robust sales levels of recent months. Therefore, because the same basket of goods has become noticeably more expensive in such a short period of time, demand for retail goods may not be increasing as rapidly as sales figures would suggest. Consequently, although rising retail sales are typically an indicator of demand for additional real estate space, that might not be the case in this instance.

In the five years prior to the pandemic, the University of Michigan’s measurement of consumer sentiment was consistently high, with the index oscillating between 87 and 101. In April 2020, it plunged to a reading of 71.8. After trending upward the following year, it has consistently declined and reached a low point of 62.8 in February 2022, a level not seen since October 2011. This muted sentiment is largely a result of rising consumer prices, which is bound to have downward effects on retail spending and demand for retail square footage.

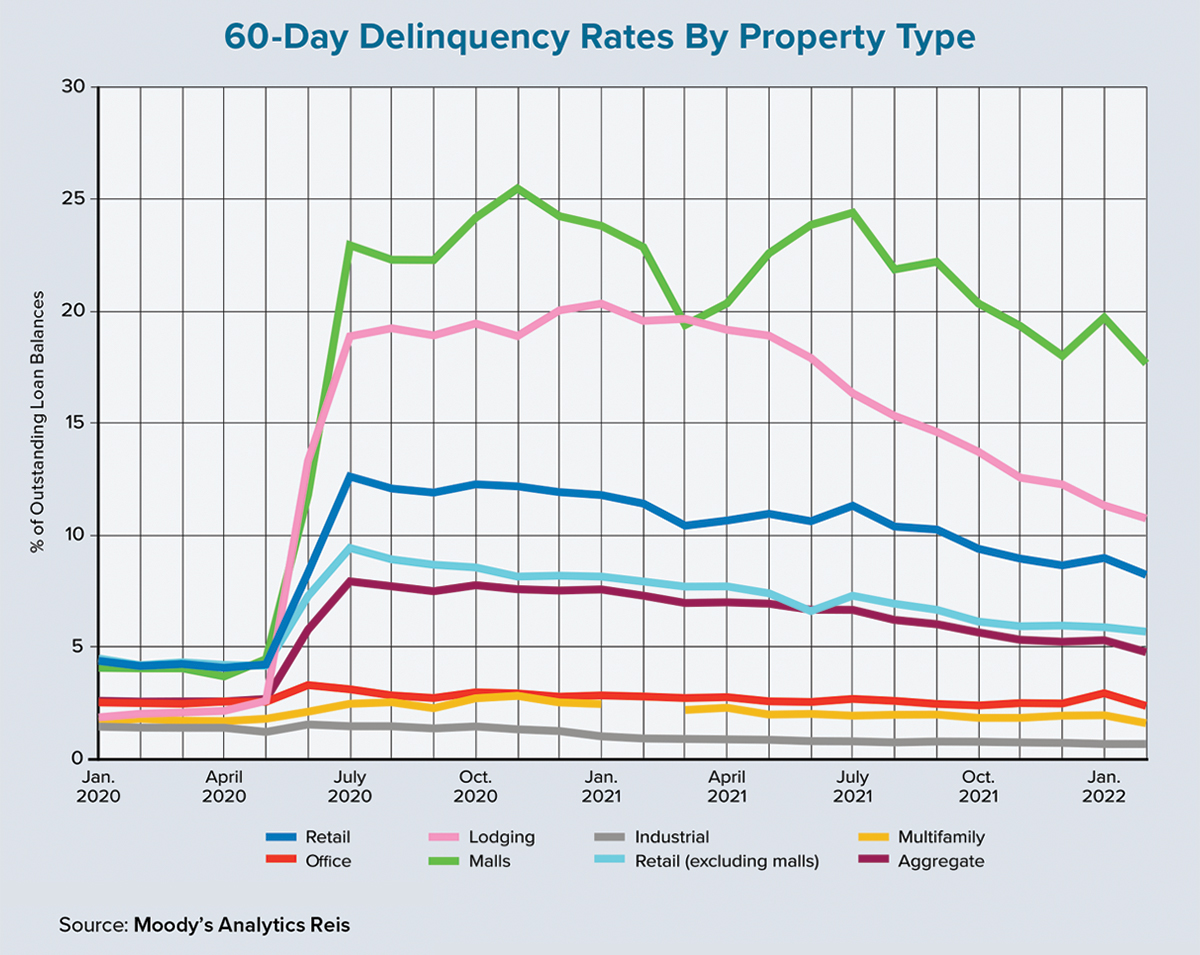

Even though the early days of the pandemic were trying for owners of retail assets, with mortgage delinquencies climbing sharply across all property subtypes, the sector has managed over time to stave off complete calamity in the capital markets. The accompanying chart shows that the share of retail-backed loans at least 60 days overdue dropped from a peak of 12.6% in July 2020 to 8.2% in February 2022. But retail and its subtypes still have some of the highest rates of past-due loans in recent years.

Unsurprisingly, regional mall properties continue to be the most at-risk retail subtype and are driving overall delinquency behavior among retail assets. The share of mall debt deemed delinquent peaked at 25.5% in November 2020, although it shrank to 17.7% as of this past February.

A similar story emerges when looking at loan defaults in 2021 as retail proved to be the largest contributor. Last year, retail debt posted an aggregate loss of $1.1 billion due to the liquidation of 131 retail loans, accounting for 48.8% of all commercial mortgage losses, according to Moody’s data. Once again, regional malls led the overall capital-market losses by retail properties ($700.5 million on only 18 loans collateralized by mall assets). These losses accounted for 62% of all retail loan losses and 30% of all commercial mortgage losses last year. Although this paints a rather dire picture of the health of malls during the COVID-19 era, many of these malls were struggling and performing poorly prior to the pandemic due to an evolving retail environment.

Performance metrics indicate improving prospects for retail, however slight. Moody’s data shows that the vacancy rate peaked in 2020 at 10.5%, with negative net absorption totaling nearly 3 million square feet. Retail began to slowly recover in 2021 with vacancies declining by 20 basis points. Renewed demand that outpaces completions is a trend that is expected to continue for the next five years.

Fundamentals will stabilize in the coming years as the sector recalibrates toward a new equilibrium, given the demand-side challenges it has faced over the past decade. Although fundamentals and capital-market performance provide a glimmer of hope that the sector may be on the mend, retail will continue to face pricing challenges during the next 12 months as a multitude of factors continue to influence demand for these spaces. ●