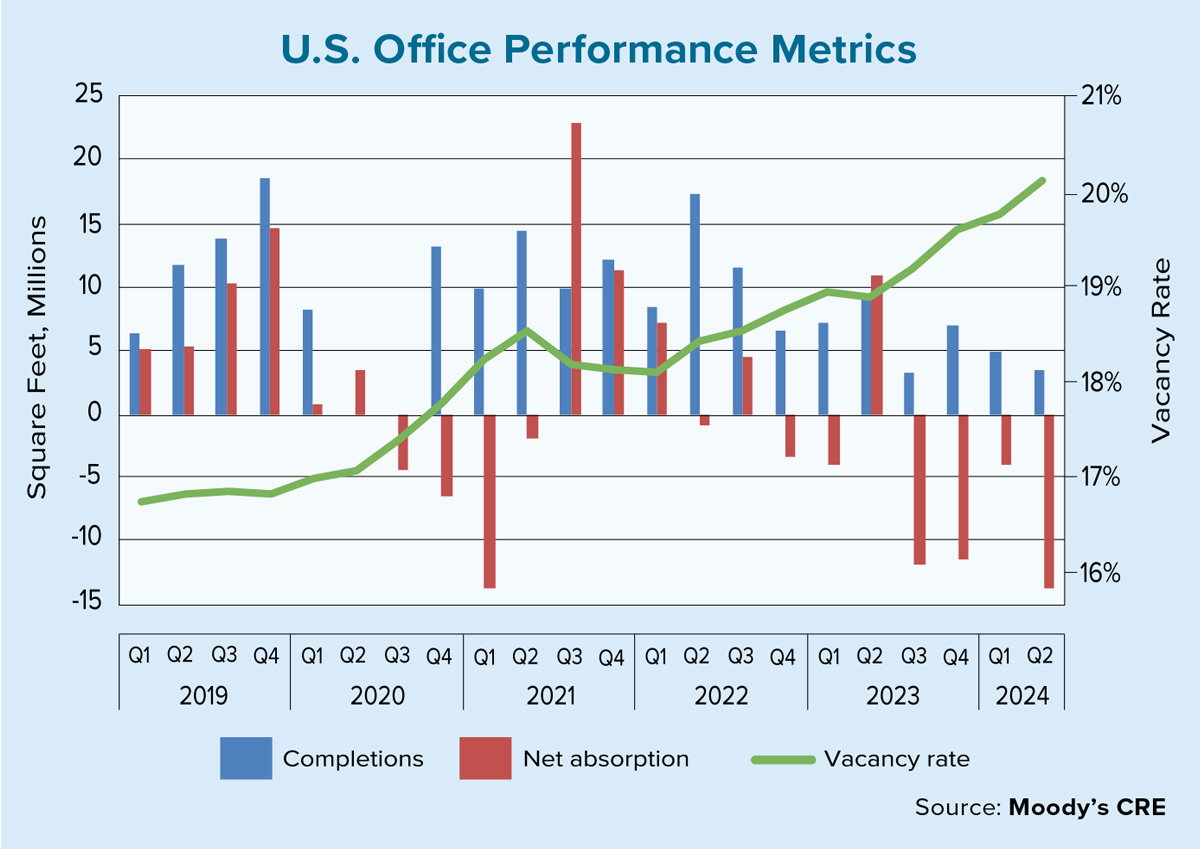

As the Federal Reserve approaches its first interest rate cut since the beginning of the COVID-19 pandemic, the change in direction cannot come soon enough for the troubled office sector. Moody’s Analytics data revealed that in the second quarter of 2024, the office sector’s vacancy rate hit an all-time high of 20.1%.

This was the first time the 20% threshold had been breached in the nearly 50 years of Moody’s data history. For context, the pre-pandemic record occurred during the savings and loan crisis when the office vacancy rate peaked at 19.3% in both 1986 and 1991. Unlike the savings and loan crisis, which was induced by a combination of excess supply and macroeconomic uncertainty, this cycle’s peak reflects the fallout from the pandemic that significantly accelerated the hybridization of the workforce.

With the long-term office vacancy rate going back to 1979 averaging 15.2%, it is clear the sector has been shocked to a new equilibrium. The question, though, is just how much higher will vacancy rates go? A recent Moody’s Analytics research paper estimated the nationwide office vacancy rate is expected to peak at approximately 24% in early 2026.

Moody’s preliminary second-quarter estimate for net absorption of almost 14 million square feet was at the lowest level in three and a half years, and was another sign that the demand for office space continues to diminish. Additionally, on the supply side, completions of a little more than 8 million square feet over the first half of the year marked the slowest pace since 2012.

Given this backdrop, one might assume rents would have sharply declined. But that hasn’t been the case. Asking rents, for example, rose by 65 basis points in the second quarter to $35.71 per square foot. This marked the 13th consecutive quarter of flat-to-positive rent growth. Granted, the quarterly change in asking rents has been below 1% over this period, it is still worth pointing out that asking rents are 4% higher than their pre-pandemic levels (using the fourth quarter of 2019 as a proxy).

One reason rents have held up is that the typical office lease is for five to 12 years (with some leases lasting beyond 20 years), which helps to provide landlords with stable cash flows during down markets. On the flipside, there’s downside risk to in-place rents when those leases mature.

Asking rents don’t paint a complete picture with regards to leasing activities. Effective rents, which include concessions, such as free rent periods, rent reductions, tenant improvement allowances and other financial incentives, provide a clearer view. In other words, while asking rents increased slightly quarter-over-quarter, effective rents declined by seven basis points to $28.17 per square foot, the fourth straight quarter of flat or falling rents. Moreover, relative to the fourth quarter of 2019, effective rents are a mere percentage point higher.

Given the slow bleed occurring in the office sector, landlords have been increasingly turning to concessions as a mechanism to attract and retain tenants and reap the financial benefits associated with higher occupancy rates. To highlight the significance that concessions are playing in today’s market, the difference between asking and effective rents is also at record levels, according to Moody’s research. Specifically, asking rents, on average, are 26.8% higher than effective rents at the national level. Said differently, concessions imply a discount of 21.1% on asking rents.

How high vacancy rates climb and, by extension, the magnitude of concessions in the market remains to be seen. Job growth continues to remain a key driver for office space demand and with increasing signals of a cooling labor market, how the Fed manages the balance of risks between inflation and economic growth will be even more critical for the sector.

The shift toward remote work and flexible working arrangements has added another layer of complexity in terms of predicting future office space needs. The office sector is continuing to work through a period of transformation, and while more turbulence lies ahead, tenants are likely to hold the upper hand at the negotiating table for the foreseeable future.