Driven by shutdown policies related to containing the spread of COVID-19, the U.S. economy is likely to go through the worst downturn since the Great Depression. Moody’s Analytics Reis forecasts that U.S. gross domestic product will decline by 6.6% year over year in 2020, a figure that is 1.7 times worse than the Great Recession of 2008-2009. Compared to that six-quarter meltdown, however, the current recession should move at light speed, with most of the distress happening in the middle two quarters of this year.

The retail-property sector, in particular, is expected to experience significant distress. Under pressure from the rise of e-commerce over the past 20 years, this sector entered the current downturn in a position of relative weakness. Mall vacancies were at 9.7% at the end of 2019, an historic high that topped the 9.4% level at which vacancies peaked in 2011 following the last downturn.

Since pandemic-related effects on the economy began escalating this past March, major retailers such as J. Crew, Neiman Marcus and J.C. Penney have announced plans to enter bankruptcy. Others, such as Macy’s and real estate investment trust Simon Property Group, preemptively closed their stores.

Not every retailer has been asked to shut down due to shelter-in-place policies. Grocery stores and pharmacies have remained open, having been deemed essential businesses. One of the handful of employment categories that posted gains in the April 2020 jobs report included warehouse clubs and supercenters, which grew by 93,000 jobs compared to the prior month.

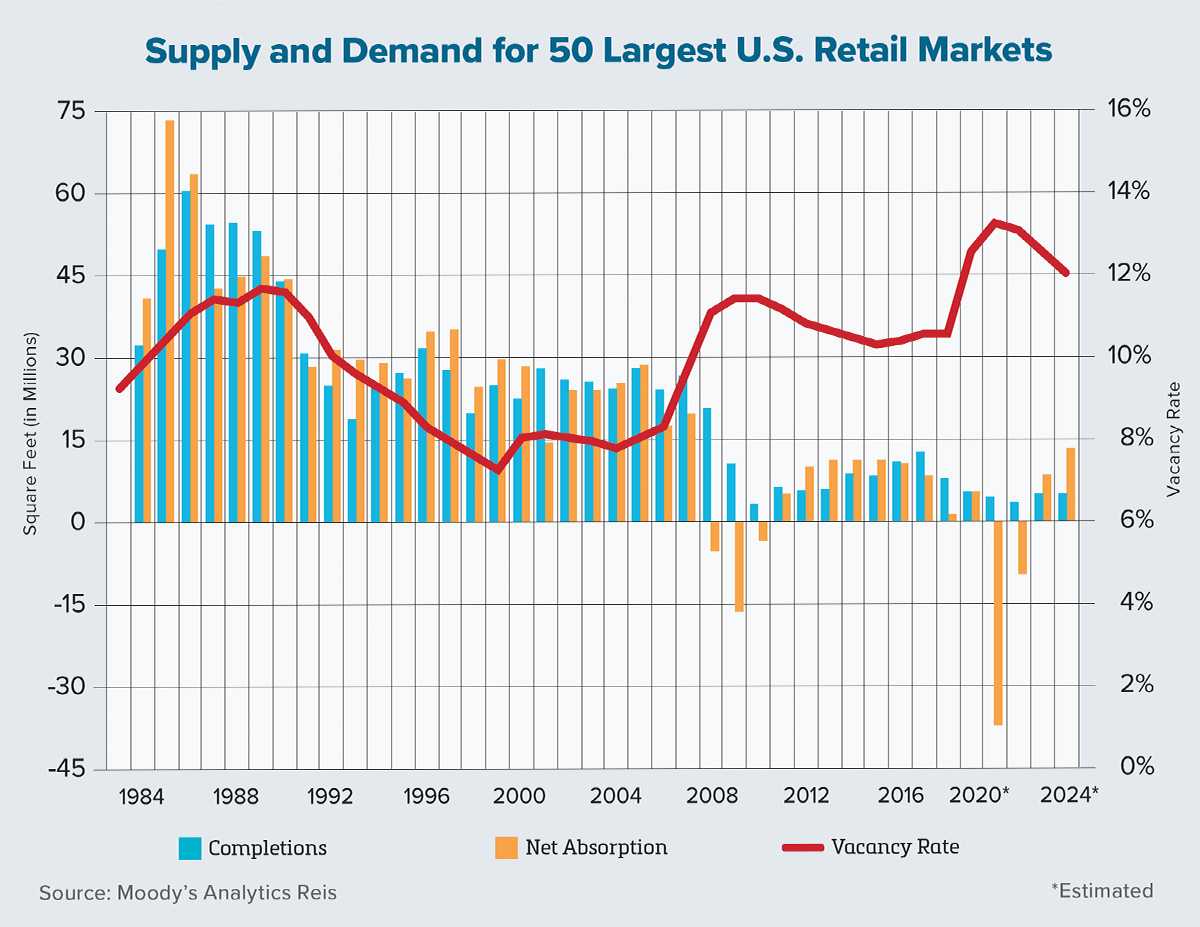

The current crisis is expected to hit the retail-property sector over the short and long term. Moody’s Analytics Reis expects that neighborhood- and community-center retail vacancies will rise from 10.2% prior to the pandemic to a record high of 13.3% in 2021 before gradually recovering.

The recovery will be exceedingly slow and we expect vacancies to remain somewhat elevated through 2024. Interestingly, smaller markets might experience better performance metrics over the next five years, given how local stores tend to have relative dominance in an area of limited trade. In the chart on this page, which aggregates data from the nation’s 50 largest retail markets, we expect vacancies to remain elevated above the cyclical high from 2008-2009.

Effective rents are expected to decline by an historic amount — 11.1% in 2020 alone, nearly double the 6.1% decline that the retail asset class experienced from the end of 2007 through the end of 2011. What is next for retail? There are three predictions that are likely to come true in the recovery.

First, if they have not done so already, retailers will acknowledge the need to move away from brick-and-mortar stores and accelerate plans to sell products and services online. Earlier this year, for example, watchmaker Patek Philippe began offering some models online via a select group of authorized dealers after previously refusing to sell any of its products online. The COVID-19 crisis forced their hand.

Next, the pressure on brick-and-mortar stores will be even more intense. Simon Property Group operates malls that perform better than the market average. They will need to think even more carefully about the malls and outlet stores in their portfolio. Macy’s has already begun pursuing a reformatting strategy, building smaller stores in non-mall properties while closing 125 mall locations. The pandemic will accelerate plans like these for other retailers.

Finally, dense urban areas may fall out of favor. If retail destinations previously favored areas with an agglomeration of households to support sales, then any post-pandemic trend that prompts households to shy away from concentrated urban areas will influence how the retail landscape evolves. •