The moderating “slowcession” economy has recently helped to cool performance within the once red-hot industrial real estate sector. Rent growth, while still a bit above the long-term quarterly average, is now well below its pandemic-era peaks across warehouses and distribution facilities as well as flex spaces for research and development (R&D).

Furthermore, net absorption for both property subtypes has plummeted since mid-2022. The question now being asked is, where do we go from here? Mortgage lenders and borrowers are looking to determine whether the sector is simply regressing toward a new equilibrium after a positive demand shock, or if there is significant stress forthcoming for this highly favored asset class.

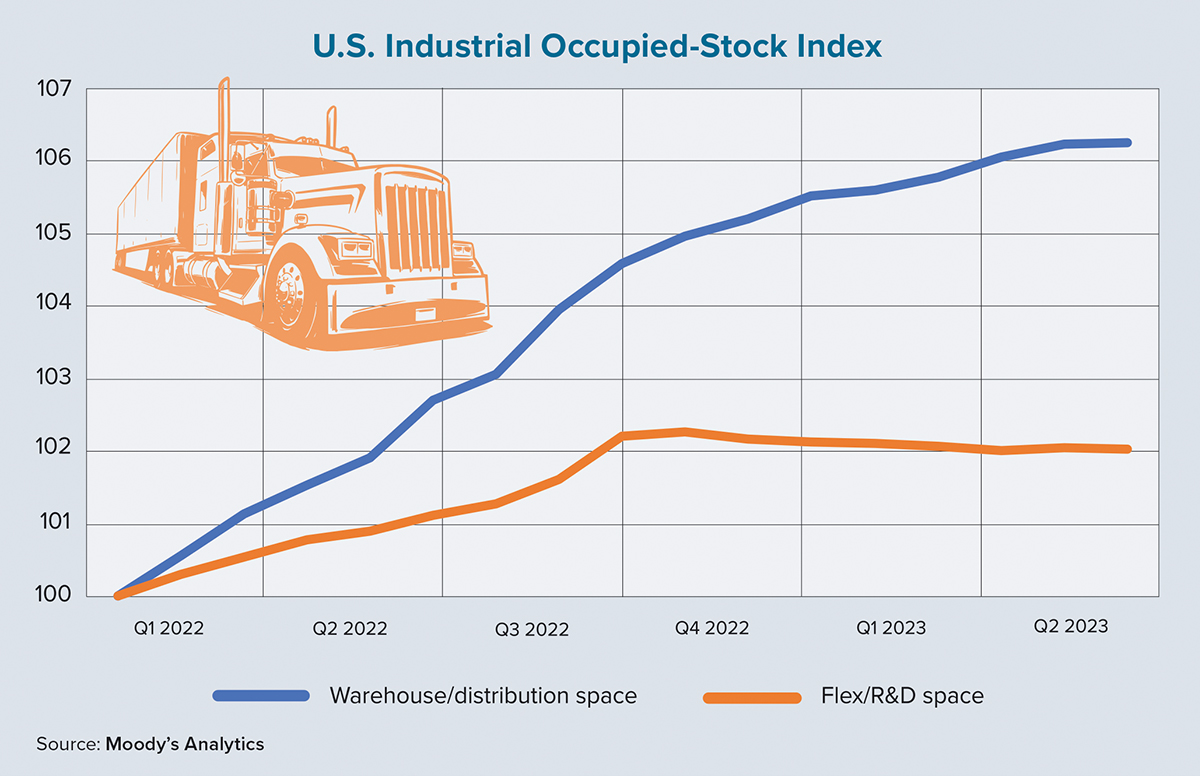

Before we dig into the Moody’s Analytics outlook for the sector as a whole, one interesting development of note is the divergent net-absorption paths within the industrial subtypes. As mentioned, declining lease activity has been observed for both warehouse and flex spaces in recent quarters, but the latter category is facing a much stiffer test of its resilience in today’s market.

Since mid-2022, the level of occupied square footage for flex and R&D spaces has actually declined for the nation as a whole. As the chart on this page shows, it’s true that occupied stock is still above the level recorded at the start of 2022, but a period of nearly a year without any net expansion of space usage is worrisome. As for warehouse and distribution space, it is clearer that there is a moderation in the pace of growth, rather than the growth hitting a wall.

The rationale for the divergence in fortunes stems from the nuances within the subtype uses and their relationships with the national and global economies. Flex and R&D space often has elements of the office sector (and even light manufacturing). With changes to the workplace related to hybrid and remote policies, owners of flex spaces are — and likely will continue — feeling at least some of the pain of their more specifically tailored office-space counterparts.

On the manufacturing front, the past year has been a tough one for this economic sector as a whole. Various measurements of manufacturing activity and sentiment have been pointing toward a less-than-favorable environment. After a period of rapid growth in 2021 and early 2022, a combination of headwinds has brought current and future space needs into question for flex and R&D spaces.

In contrast, the tailwinds for the warehouse and distribution sector are considerably stronger and much less uncertain than those of the flex segment. E-commerce continues to grow. Meanwhile, accelerated migratory patterns, as well as fixes to the logistics network weaknesses that were exposed early in the COVID-19 pandemic, promote greater confidence in this subsector for lenders, developers and investors.

As for a more specific outlook for the industrial sector, Moody’s maintains a positive view for this property type. Warehouse and distribution spaces should continue their upward trajectory, while the flex/R&D segment is expected to regain its footing. A new and higher growth path has been established as companies reshore or nearshore their manufacturing activities, which will lessen supply chain pressures over the long term and allow the growth of e-commerce to endure.

Lofty construction expenses for manufacturing facilities are serving as a leading indicator of this path. Additionally, innovative shipping methods and the push to ship many goods in less time requires a larger and more spread-out footprint of warehouse and distribution facilities. The construction pipeline indicates that many of the projects started during the height of growth in this sector will come online in 2023, meaning that new supply will likely exceed net absorption for the first time in several years.

Nonetheless, relatively constant vacancy rates in the 4% to 5% range are poised to keep effective rent growth rates in the region of 6% per year. This is still well above the historic yearly averages prior to 2020. ●