Retail sales increased at a healthy pace of 3% for 2024 before falling by 0.9% month-over-month in January, which was short of expectations. The positive momentum in the second half of 2024 was inevitably due for a pullback considering the holiday shopping season had concluded and consumers continue to remain cost-conscious in the face of economic uncertainty.

The headline weakness in January was likely overstated — and could be adjusted upward — given motor vehicle sales were responsible for nearly half of the decline. For what it’s worth, January 2024 saw a similar monthly decline, yet ended the year in the black.

On the inflation front, the Consumer Price Index in January came in hotter than expected at 0.5% month over month and was higher by 3% year over year. Despite inflation remaining above the Fed’s 2% target, wage growth has outpaced inflation since around March 2023, inherently implying rising real incomes.

“Aggregate spending measures have been robust considering people in the bottom half of income distribution only account for 29% of total consumer spending.”

Of course, not all households have weathered the inflationary storm over the past five years so gracefully, especially lower-income households which have been less likely to partake in the significant home equity or stock market gains that have occurred. Aggregate spending measures have been robust considering people in the bottom half of income distribution only account for 29% of total consumer spending.

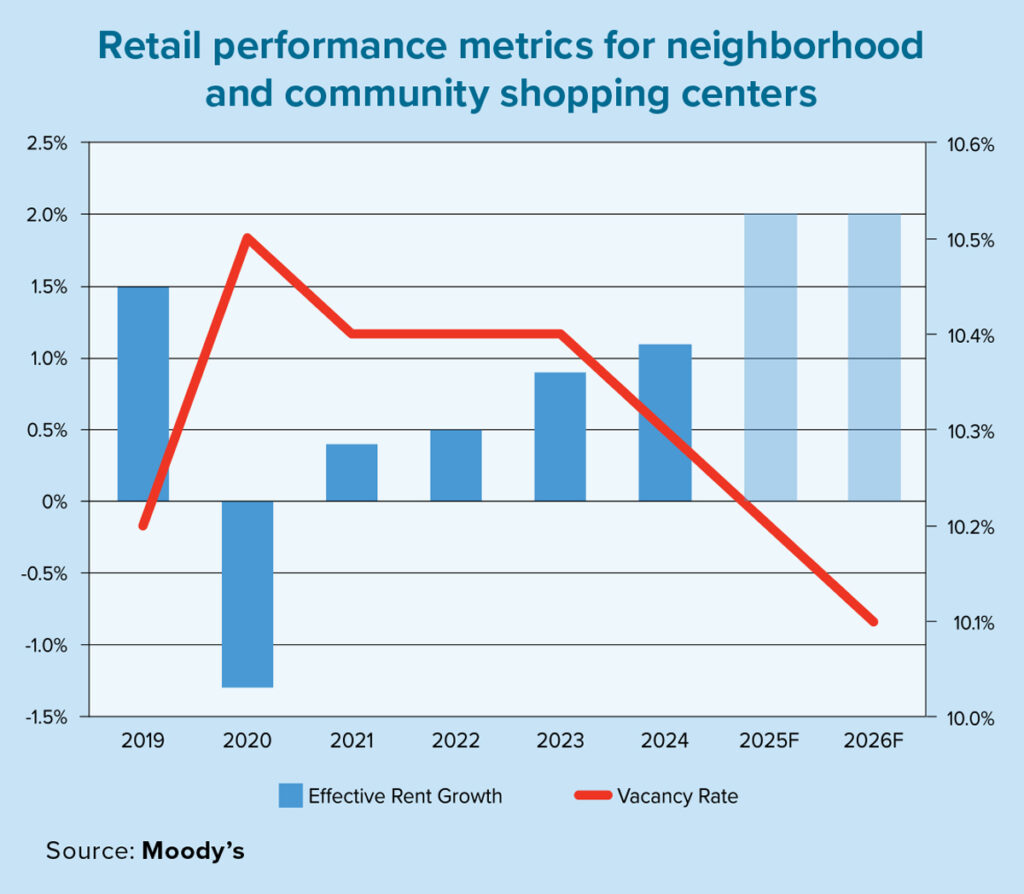

In terms of implications for the retail real estate market, Moody’s baseline forecast, which encompasses neighborhood and community shopping centers, predicts nationwide effective rent growth to increase by approximately 2% in both 2025 and 2026. Additionally, the vacancy rate will likely remain in the low-10% area over this period. Said differently, expect net absorption to outpace completions over the next two years with the gap between the two widening in earnest in 2026.

Moody’s also expects effective rent growth in the Southwestern and Southern Atlantic regions to outperform the national average over this period while the Midwestern and Northeastern regions lag slightly behind. The Western region is forecasted to perform in line with the national trend.

There are, of course, several risks to this forecast with trade policy and the knock-on effects for energy prices perhaps the most salient at the moment. Even so, directionally speaking, interest rates are poised to move lower in the second half of the year, which at the margins, should bolster spending patterns, especially for big-ticket items such as automobiles and appliances.

Moody’s as of February 2025 assumes the next interest rate cut will occur in the third quarter of 2025. It also bodes well that consumer balance sheets, when analyzed through the lens of household debt service as a percentage of disposable income, remain below their long-term average, implying additional headroom in spite of rising debt balances.

Interestingly though, despite a full percentage point reduction to the federal funds rate in 2024, the 10-year Treasury yield has remained fairly sticky near the mid-4% level. One explanation for this is related to fiscal sustainability and how an increasing federal deficit at roughly $2 trillion would require greater bond issuance from the U.S. Treasury to plug the financing gap. Regardless, while there is always uncertainty in preparing an economic forecast, 2025 is particularly hazy. Yet if the past several years are any indication, don’t bet against the American consumer.