America’s senior housing industry experienced a major shock five years ago as the COVID-19 pandemic drove a rapid rise in the senior housing vacancy rate. While every sector within commercial real estate was disrupted to some extent, the jolt to senior housing was exceptionally strong and played out in unique ways given the demographic profile of renters.

Five years since that inflection point, the national senior housing market has shown a remarkable recovery as its vacancy rate has fallen dramatically. Early pandemic concerns over operators’ abilities to fill their units have rapidly given way to questions surrounding availability and affordability.

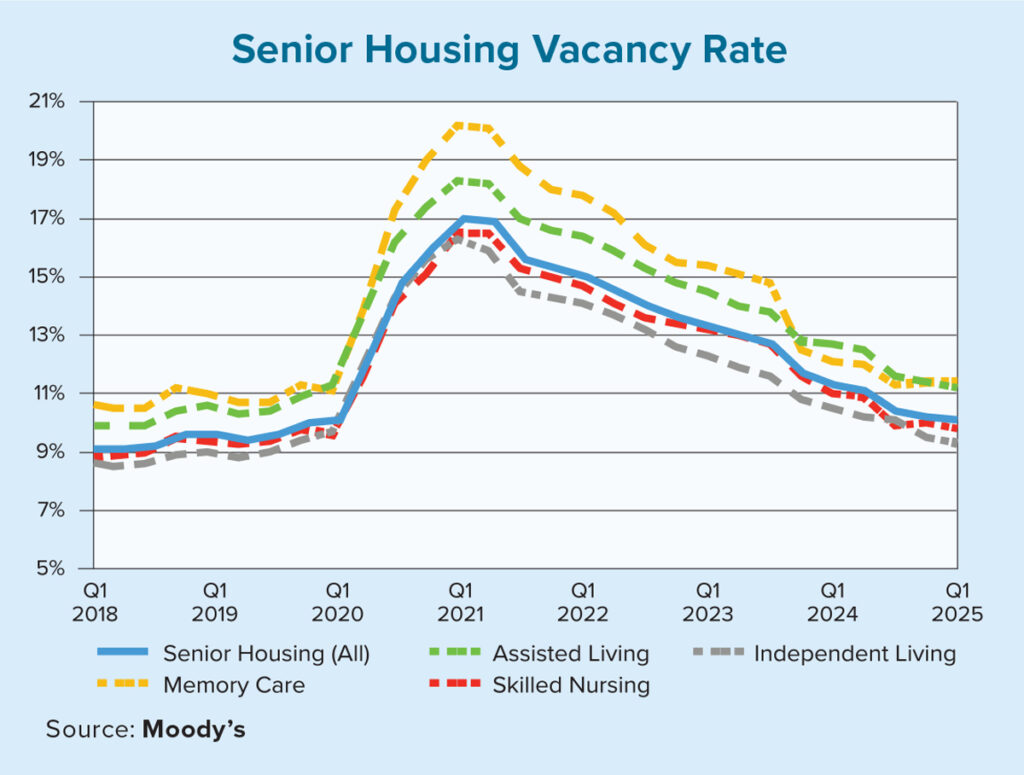

Moody’s Analytics reports that the vacancy rate in the first quarter of 2025 for senior housing was an average of 10.1%, just slightly above the pre-pandemic figure of 10% from the fourth quarter of 2019. Following the initial shock of the pandemic and the spiking vacancy rate that peaked at 17% in the first quarter of 2021, the national senior housing vacancy rate has experienced 16 consecutive quarters of declines. The chart below highlights the sharp climb in the vacancy rate in the face of the pandemic, along with a smoother recovery as seniors have re-embraced this lifestyle.

This gradual and consistent recovery stands apart from other sectors within commercial real estate affected by the pandemic. Notably, the hotel industry experienced a sharp downturn followed by a quick recovery as business and tourism travel rebounded, while the office sector has seen a prolonged decline due to lasting adjustments in demand, leading to another office vacancy rate peak in the first quarter of 2025.

Senior housing faced unique challenges during the first year of the pandemic due to the pandemic’s substantial effect on senior health and lifestyle preference shifts throughout 2020 and 2021. As health care treatments for vulnerable elderly Americans advanced and lifestyle restrictions across state, local and community levels eased each passing year, demand has rebounded.

Health care and lifestyle adjustments have merged with demographic drivers to steadily increase demand. America’s baby boomer generation has increasingly moved into retirement age in recent years. Also, while not yet at the ages of peak senior housing utilization, America’s population pyramid highlights the rising wave of both current and prospective renters entering the senior rental market in the years ahead.

Despite immediate and looming demand, financing issues arising from prolonged high interest rates have constrained new supply growth, leading to the current senior housing market featuring decreased vacancies and rising rents with a tight construction pipeline.

America’s aging population pyramid indicates demand is likely to continue rising, but the housing supply remains tight. The most precarious moment senior housing faced as a sector coincided with the ideal investment period when interest rates were lowest during the heart of the pandemic. As it became more evident that senior housing was positioned for recovery, interest rates had already begun to rise throughout 2022, complicating new construction efforts.

Consequently, both new completions and the construction pipeline have remained low in recent years, with only 5,264 new units added year over year in the first quarter of 2025. The broader multifamily market has consistently expanded its inventory by more than 2% year over year, while annual senior housing inventory expansion has fallen to well below 1%.

Across five regions Moody’s Analytics tracks in the U.S., the Northeast region maintained the lowest vacancy rate in the first quarter of 2025 at 8.7%, holding onto its pre-pandemic performance when it also maintained the nation’s lowest vacancy rate. However, a part of that performance has come from the lack of supply growth.

Inventory growth as a percentage of existing inventory was already behind the rest of the nation pre-pandemic, a trend amplified in recent years. Over the past 10 years, senior housing inventory in the Northeast has expanded by just 9.3%. The nation’s four other regions all experienced a 10-year inventory expansion of at least 16.8% as of the first quarter of 2025.

America’s senior housing market is likely to face affordability concerns as rents climb, resulting from demand outpacing new supply. Demographic trends are expected to drive this trend forward. The period of higher-for-longer interest rates has led to a tight pipeline for new units, but the senior housing sector is poised to see a stronger pipeline than in recent years should demand continue to strengthen.